A Steadily Growing Housing Market

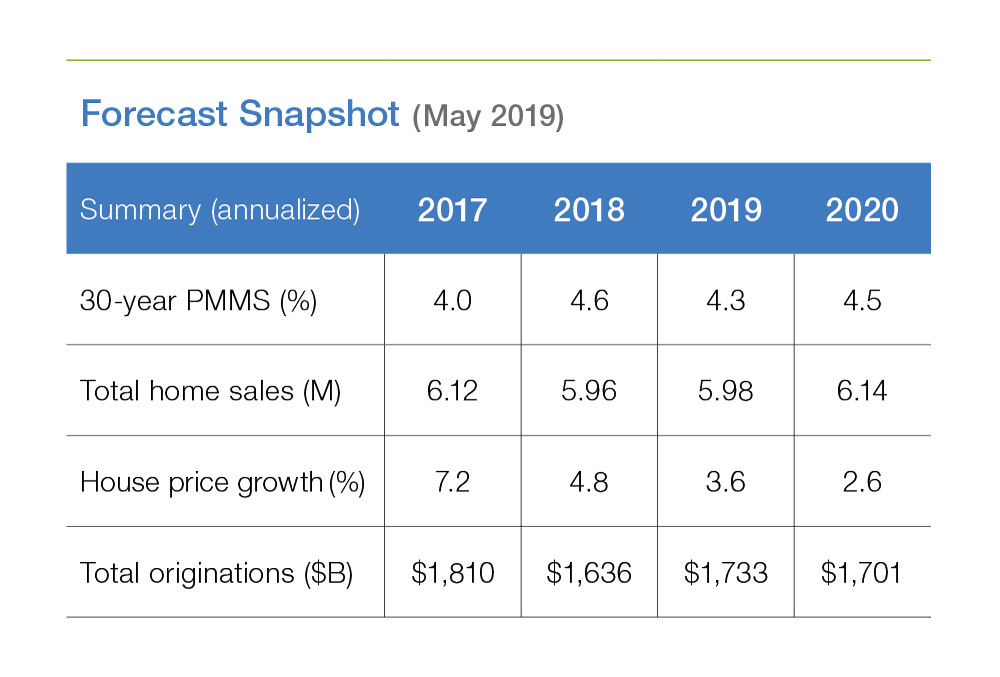

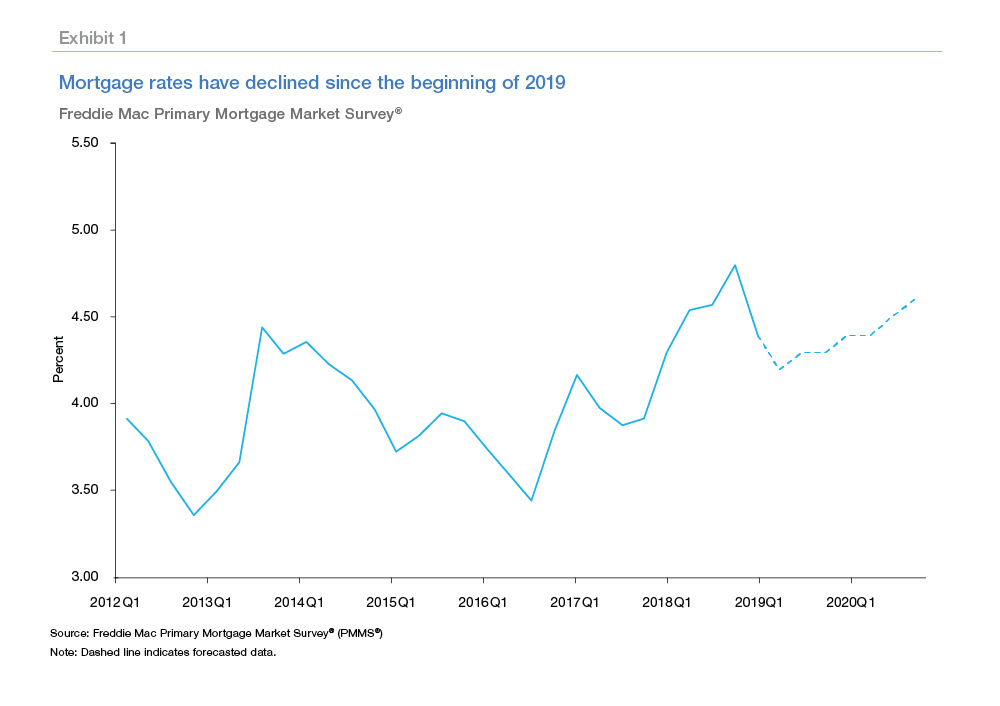

After increasing throughout April, mortgage rates declined at the start of May. The combined positive impact of low mortgage rates, a strong labor market, low unemployment, and modest wage growth supports our forecast for a steadily growing housing market in 2019.

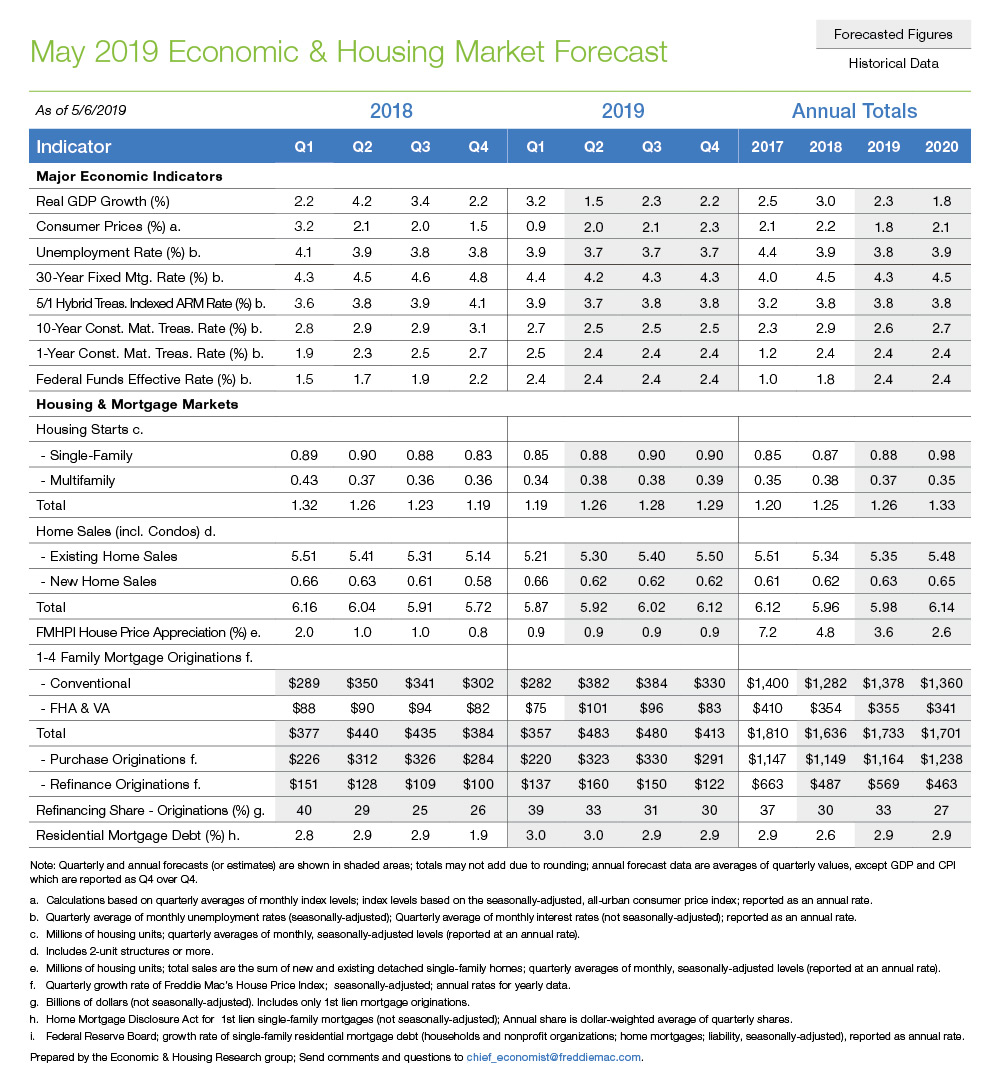

Real Gross Domestic Product grew at an annual rate of 3.2% in the first quarter, beating expectations. Transitory factors like private inventory investment were behind the first quarter surge and are unlikely to persist throughout the year. We expect GDP to grow 2.3% in 2019 before slowing to 1.8% in 2020.

The Bureau of Labor Statistics reported an unemployment rate of 3.6% in April, which marked a 50-year low. This has informed our decision to lower our unemployment rate forecast to 3.7% for the second quarter of 2019, and we expect it to remain flat for the remainder of 2019, before increasing in 2020. Overall, we expect the unemployment rate to be 3.8% and 3.9% in 2019 and 2020, respectively.

Mortgage rates continue to decline since the beginning of 2019

We still expect the 30-year fixed-rate mortgage to continue its downward trend, averaging 4.3% in 2019, before increasing to 4.5% in 2020.

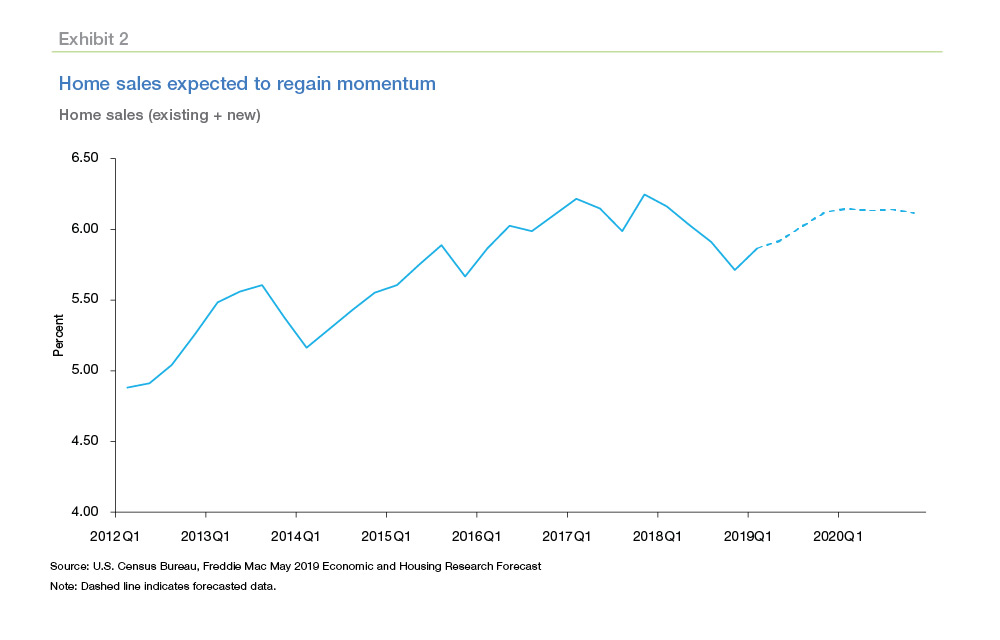

Homes sales showing signs of recovery

Existing home sales have benefited from low mortgage rates and a healthy job market. We expect stronger home sales and housing starts in the coming months. This will bring full-year housing starts and sales in 2019 back to around the same level we saw in 2018.

House price appreciation in the first quarter of 2019 was slightly higher than previously anticipated. This has led us to revise up our 2019 annual forecast for home price growth to 3.6%. On the other hand, we expect house price growth to moderate to 2.6% in 2020.

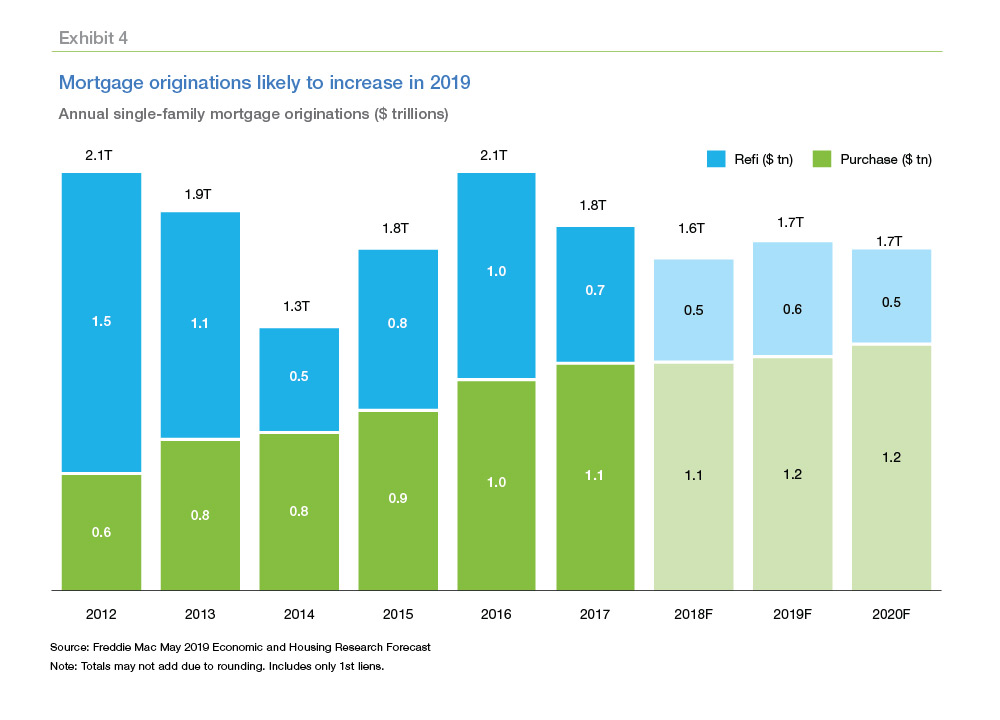

Mortgage originations expected to increase with low mortgage rates

The originations market will recover from its 2018 slump this year driven by declining mortgage rates, which continue to provide an impetus to first-time homebuyers as well as homeowners looking to refinance.

Moving forward, we will be forecasting the growth rate for single-family residential mortgage debt of households and nonprofit organizations. This replaces our forecasts for total residential mortgage debt, which included multifamily mortgages as well. The change is an effort to be consistent with our mortgage originations forecasts, which reflect only single-family mortgages. We expect the growth rate of outstanding residential mortgage debt to be 2.9% in both 2019 and 2020.

First Quarter 2019 Refinance Report:

Cash-Out Volumes Remain Low

Based on Freddie Mac’s Quarterly Refinance Statistics, “cash-out” borrowers, those that increased their loan balance by at least 5%, represented 76% of all refinance loans in the first quarter of 2019. That’s down from 82% at the end of 2018. The “cash-out” share of refinances peaked during the third quarter of 2006 when it reached 89%. While the share of cash-out refinances is near its historical high, the total cash-out volume remains much lower than the previous decade. Adjusted for inflation in 2018 dollars, an estimated $16.6 billion in net home equity was cashed out during the refinance of conventional prime-credit home mortgages in the first quarter of 2019, down from $19.1 billion a year earlier and substantially less than the peak of $104.8 billion during the second quarter of 2006.

On average, borrowers who refinanced their first lien mortgage in the first quarter of 2019, took an almost 20-basis point increase in their mortgage interest rate, compared with a decrease of about 70 basis points a year earlier, and much lower than the almost 190 basis point reduction during the second quarter of 2013.

More than 95% of refinancing borrowers chose a fixed-rate loan. Fixed-rate loans were preferred regardless of what the original loan product had been. For example, 91% of borrowers who had a hybrid ARM refinanced into a fixed-rate loan during the first quarter of 2019. In contrast, only 3% of borrowers who had a fixed-rate loan chose an ARM.

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP