Where do the Service Workers In San Francisco Live?

Recently, I was in San Francisco on family business, and I took several taxi rides. Without exception, the drivers voiced the same two complaints: competition from Uber and the high cost of living, particularly the high cost of housing. Some drivers indicated they were throwing in the towel and moving to less expensive metros.

The San Francisco Bay Area is expensive. The median house price is seven times the median family income, one of the highest ratios of house prices to incomes in the U.S. It is not unusual for firms in the Bay Area to lose promising job candidates from other areas after an initial house-hunting trip. The shock of how little house even a high San Francisco salary will buy is too much for some families.

San Francisco isn't the only expensive area in the country. Many of the most desirable metros in the U.S. are among the most expensive housing markets as well. Housing advocates worry about where less-affluent households can afford to live. Even in San Francisco, where the tech industry has driven incomes far above the national average, the metro still needs a full complement of middle-income workers—police, firefighters, schoolteachers, accountants, and the like—in order to function. San Francisco needs lower-income service workers as well—waiters, baristas, janitors, security guards, and on and on. All these people need someplace to live in one of the most expensive areas in the country. So, where do they live? And how well?

How expensive is San Francisco?

Very.

The overall cost of living in the San Francisco metro is roughly 50 percent higher than the national average. 1 Food, transportation, health care, entertainment—all are more expensive than the average in the rest of the U.S.

But housing stands out. The median sales price of a home in the U.S. in 2015 was just over $200,000.2 In San Francisco, the median sales price was just over $700,000, more than three times as much. Rents are much higher in San Francisco as well. The median asking rent in 2015 in San Francisco was almost twice the median for the U.S.

Salaries in San Francisco are higher than the U.S. average, offsetting in part the higher cost of living. The median family income in San Francisco in 2015 was $103,237, roughly 50 percent higher than the U.S. median of $68,260.3 Aside from housing, higher incomes in San Francisco appear to more than compensate for the higher cost of living. But, again, housing costs stand out. In 2015, the ratio of the median sales price of a home in San Francisco to the median family income was 6.8, that is, the median home sold for almost seven years of the median family's income. In the U.S. as a whole, the house price/family income ratio was 2.9 in 2015.

"California is a garden of Eden,

A paradise to live in or see.

But, believe it or not, you won’t find it so hot

If you ain’t got the do-re-mi"

Assessing affordability

Houses (and rents) are expensive in San Francisco, but are they unaffordable? After all, people are living in all those houses and apartments, so they must be able to afford them in some sense. And demand for houses and apartments in the San Francisco metro remains high. At the end of 2015, houses sold in San Francisco typically remained on the market less than a month,4 and the inventory of houses for sale was much lower than the National Association of Realtors’ six month rule of thumb for a balanced market. Additionally, rental vacancy rates in San Francisco have remained below four percent the last few years while the average in the U.S. has ranged from seven to nine percent.5

Affordability is a tricky concept, but a common approach focuses on the ability of middle-income families to purchase the typical home in the area. Specifically, the median family income is compared to the income required to qualify for a standard mortgage6 to purchase the median-priced home. This type of approach highlights the financial challenges faced by the middle class, but doesn’t speak directly to the level of affordability for lower- and higher-income residents.

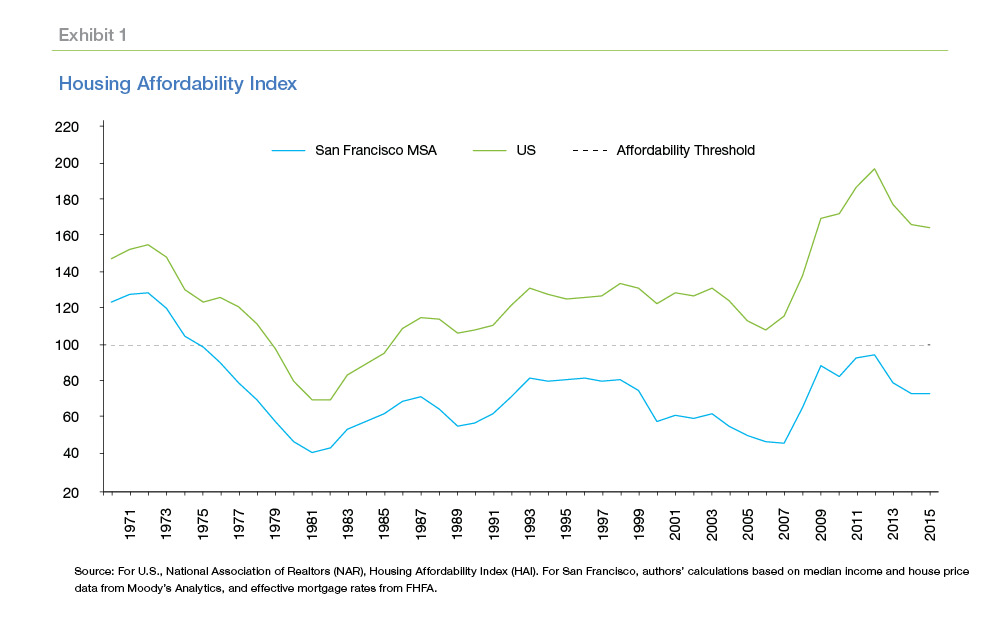

The National Association of Realtors (NAR) calculates perhaps the best-known housing affordability index (HAI) and HUD publishes the NAR index on its website.7 An HAI value of 100 indicates that a family with the median income has exactly the income required to qualify for a mortgage to buy the median-priced house. Higher values of the index are better. For instance, a value of 120 indicates that the median family income is 20 percent higher than the income required to qualify for a mortgage on the median-priced house.

Exhibit 1 compares the HAI trend in the U.S. to the trend in San Francisco. For the U.S., the HAI dropped below 70 in 1981 when 30-year mortgage rates exceeded 18 percent. As mortgage rates declined following their 1981 peak, affordability increased steadily until the housing crisis in the mid- 2000s. Following the onset of the crisis, affordability spiked driven initially by falling house prices, then later by ultra-low mortgage rates. Today, affordability is near its all-time high. The median family income is more than 60 percent higher than the income required to purchase the median-priced home.

According to this metric, housing has always been much less affordable in San Francisco. The shape of the HAI trend line in San Francisco is roughly similar to the shape of the U.S. line, but the affordability gap has grown over time. In 1981, at the low point of national affordability, the HAI in San Francisco was approximately 40, 29 points below the U.S. The HAI in San Francisco has remained below 100 since and stands today at 72, a full 92 points below the U.S. Ironically, this reading marks a relatively-golden period for middle-class affordability in San Francisco.

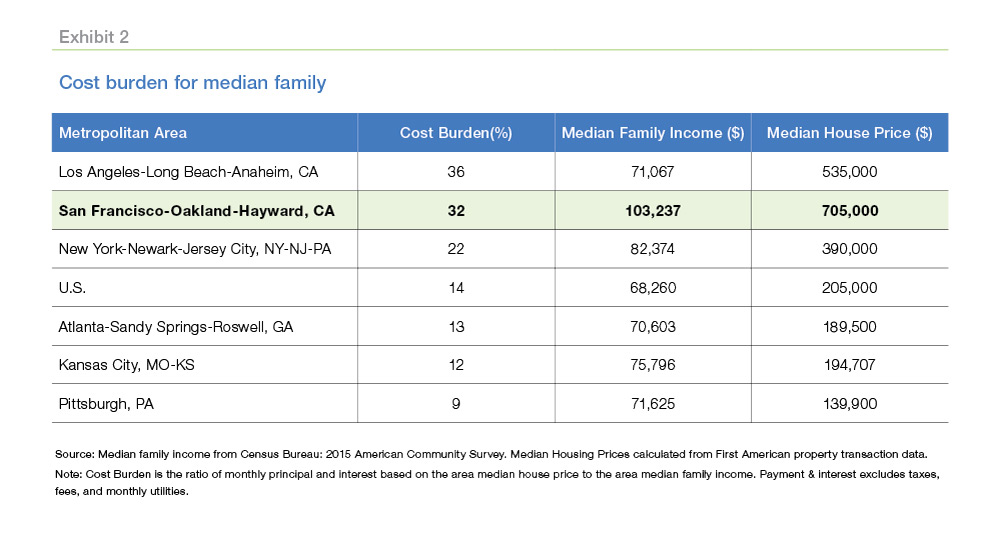

Another approach to measuring affordability tracks the cost burden; that is, the share of family income devoted to housing costs. Housing economists traditionally regard a family spending more than 30 percent of income on housing—owning or renting—as cost burdened. A family spending more than 50 percent of income is defined as severely cost burdened.

Exhibit 2 displays the cost burden of the median-income household in nine metros. San Francisco is highlighted. The median family in San Francisco spends 32 percent of its income on housing, putting it near the high end of the distribution.8

Where to live in San Francisco

The metrics discussed above provide a general guide to how affordable—or unaffordable—it is to buy a house or rent an apartment in the San Francisco metro area. However, they don’t identify where to live in the metro area. That decision involves tradeoffs between the cost burden of housing, the time consumed in commuting, and the quality of the neighborhood a family chooses.

Consider the case of a family of four where both spouses have jobs in the city of San Francisco. To minimize commute time and maximize family time, this family may choose to buy a house in the city. House prices are particularly high in the city, so the family is likely to end up with a smaller, older house than they could get in the suburbs, and there almost certainly won’t be the type of yard you’d find in a suburban home. Alternatively, the family may choose to locate in a less, expensive outlying area. Still there are tradeoffs. Areas with high-performing public schools and community amenities like parks, summer youth programs, community swimming pools, etc. are likely to be more expensive than grittier neighborhoods with fewer amenities and perhaps more crime. Choosing among these alternatives is complicated, and families must make difficult trade-offs between the cost burden of housing and the quality of life.

The problem becomes more tractable if we concentrate on just the affordability of different locations. We begin by mapping the spatial distribution of house prices.

The spatial distribution of house prices

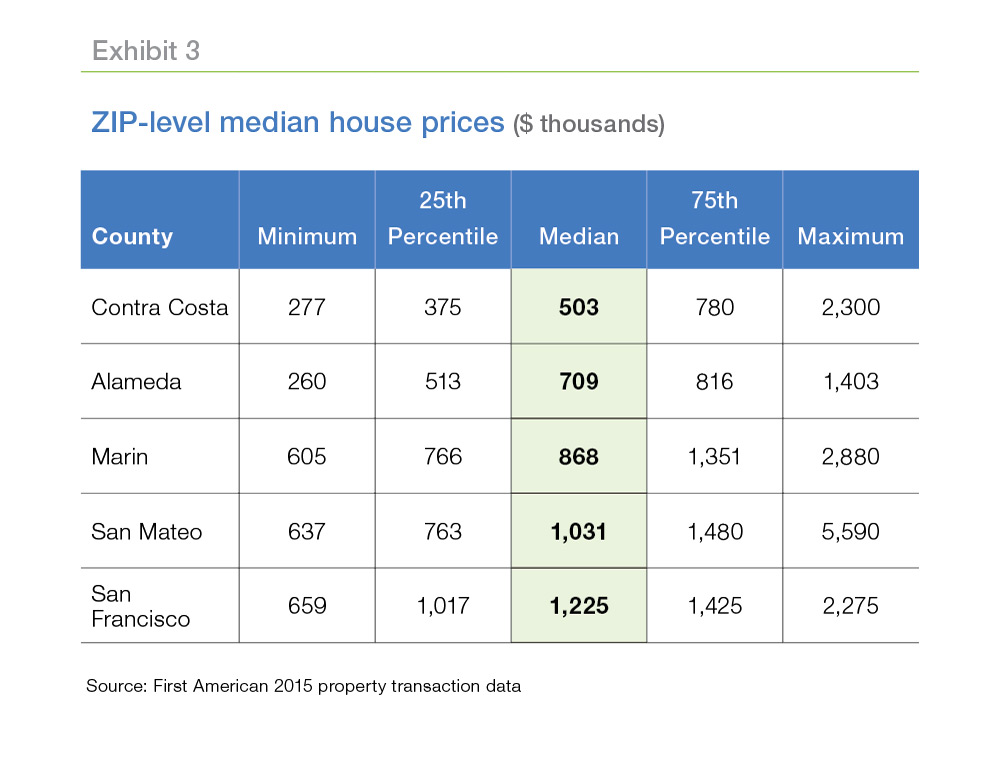

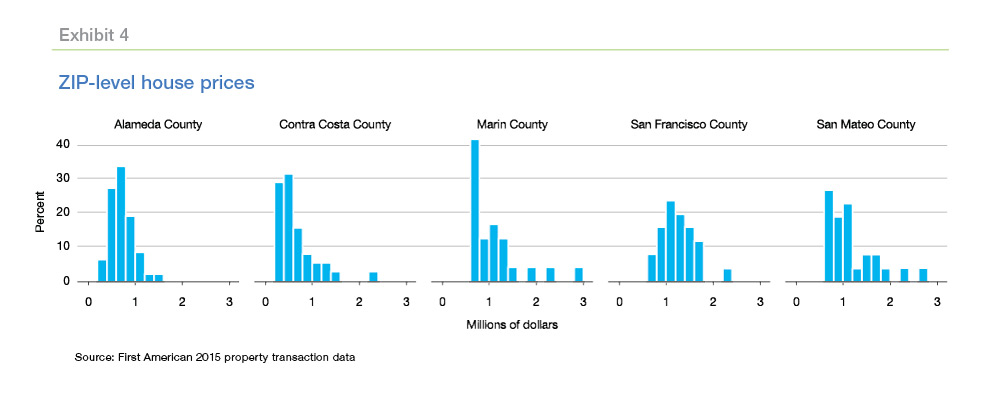

Exhibits 3 and 4 display information about the distribution of house prices at the ZIP code level in the San Francisco metro area, an area that includes, not only the city/ county of San Francisco, but four other counties as well: Alameda, Contra Costa, Marin, and San Mateo. The two East Bay counties—Contra Costa and Alameda—are significantly less expensive than the two West Bay counties—San Francisco and San Mateo. Marin County is a little harder to classify, but it is more similar to the West Bay than to the East Bay counties.

Exhibit 4 provides another view of the differences in house prices by county.9 Across the entire San Francisco metro area, median house prices are below $1 million in 104 of the 161 (65 percent) of the ZIP codes. In San Francisco proper, however, median prices are below $1 million in only six of the 25 (24 percent) ZIP codes. It’s even worse than it sounds. Of those six ZIP codes, only three are priced below $900,000. In contrast, median house prices are less than $1 million in 84 percent of the ZIP codes in Contra Costa county and 87 percent of the counties in Alameda County.

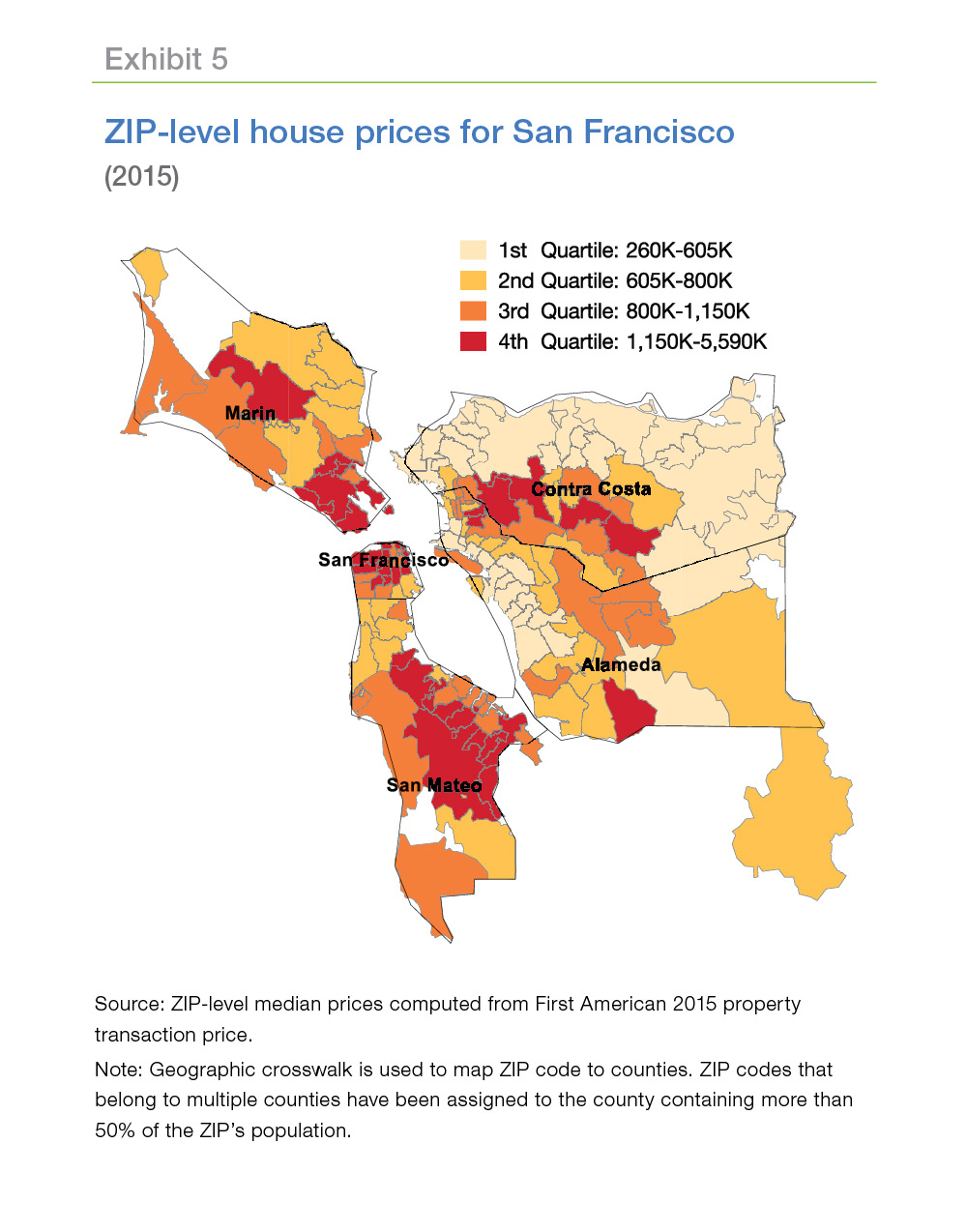

Exhibit 5 displays a map of the five counties in the San Francisco metro area. The color of each ZIP code corresponds to the median house price in that ZIP. Lower-priced ZIPs are colored light orange, while more expensive ZIPs are darker orange. Clusters of high-price “hot spots” are apparent in San Francisco, San Mateo, Marin and Contra Costa counties. A band of less-expensive “cool spots” extends up the western edge of Alameda County through Oakland. A second band of less-expensive ZIP codes runs along the northern and eastern borders of Contra Costa.

In many metros, house prices drop the farther the distance to the central business district (CBD). That distance can be measured in miles or in commute time. Intuitively, homeowners are willing to endure a longer commute in order to live in a nicer house and nicer neighborhood.

San Francisco is not entirely typical in this regard. It’s true that some of the less expensive areas can be found in the more distant reaches of Contra Costa County. And house prices in Contra Costa County drop by almost $8,000 for each mile further they are from the CBD in San Francisco, just as theory would predict. But the relationship is reversed in San Mateo County. House prices increase by almost $20,000 for each mile further from San Francisco.

It turns out there is more than one CBD in metros like San Francisco. San Mateo County lies in “tech heaven,” with San Francisco and its start-ups to the north and Santa Clara County (read “Silicon Valley”) to the south. San Mateo County is no slouch either. Google was incorporated in a garage in Menlo Park in San Mateo County. A San Mateo County ZIP code distant from the CBD in San Francisco might be only a couple of minutes from Infinite Loop, the ring road around the Apple campus in Cupertino, CA.

The spatial distribution of affordability

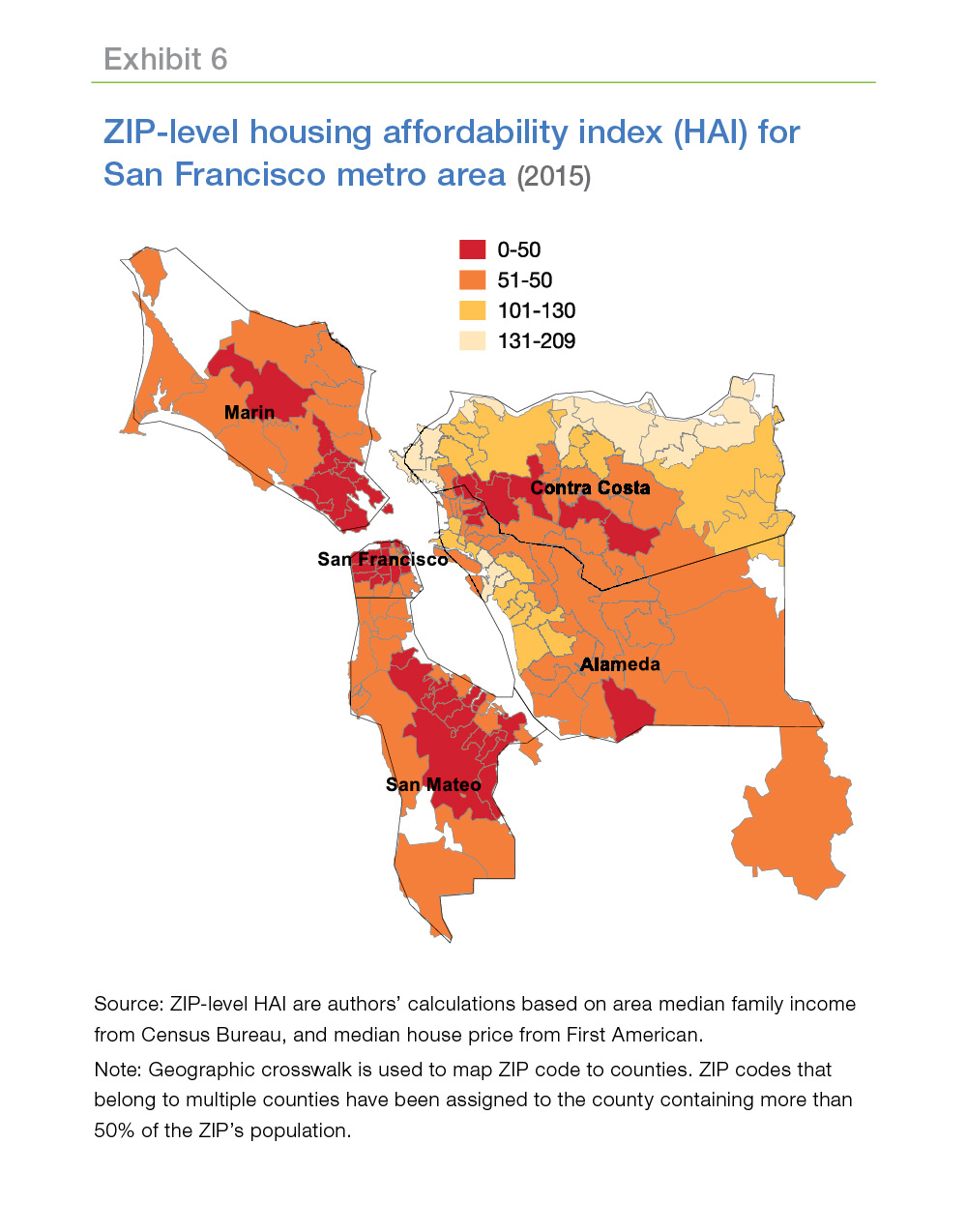

We can combine information about ZIP-level median family income with the house price data discussed above to calculate ZIP-level housing affordability indices (HAIs). Exhibit 6 maps these ZIP-level HAIs for the San Francisco metro area.

Recall that an HAI of 100 indicates that the median family income is exactly equal to the income required to qualify for a mortgage for the median-priced house. Higher (lower) index numbers indicate greater (lesser) affordability. By this measure, 23 percent of the ZIP codes in the San Francisco metro area are affordable for the median-income family living in those ZIP codes. However, in San Francisco, San Mateo, and Marin counties, there are no affordable ZIP codes; those counties appear entirely in shades of dark orange in the map. Fifteen ZIP codes (32 percent) in Alameda County and 22 ZIP codes (58 percent) in Contra Costa County are affordable—thus the many light orange areas in those two counties in the map.

If you’ve compared Exhibit 6 to Exhibit 5, you’re probably wondering why the more affluent households all live in unaffordable ZIP codes?10 It turns out that this pattern is not specific to the San Francisco metro—it’s a common relationship across the country. One reason for this phenomenon is the nature of the HAI calculation—it looks only at income and ignores wealth. Higher-income households tend also to be wealthier households. In other words, they don’t depend so much on current income to cover their housing costs.11

How does San Francisco compare to an average metro?

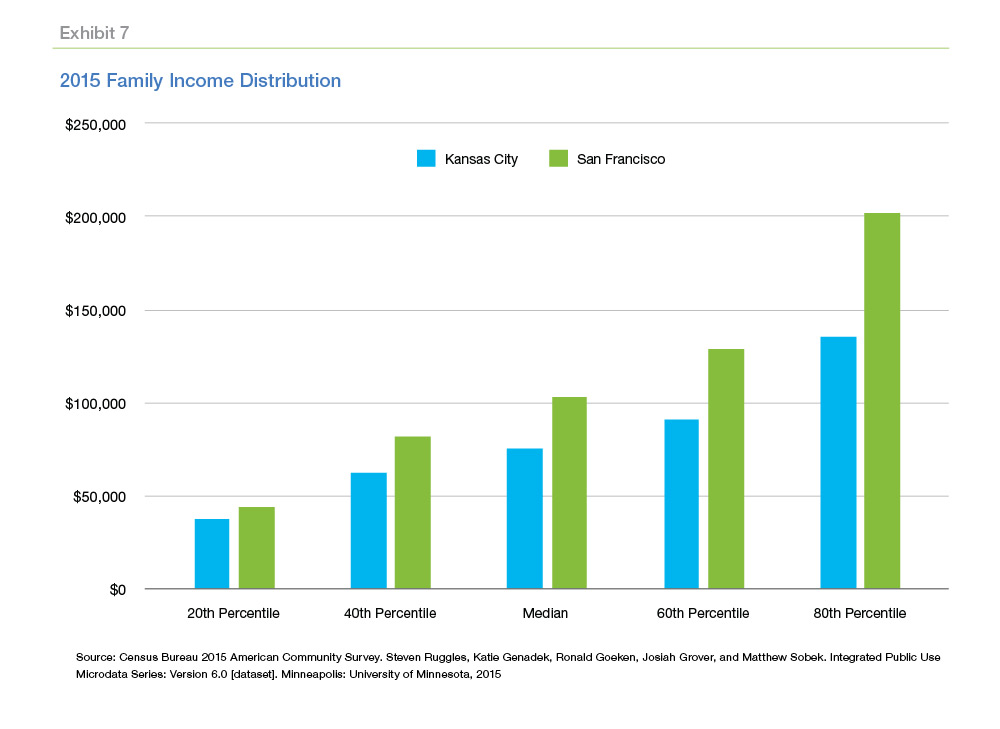

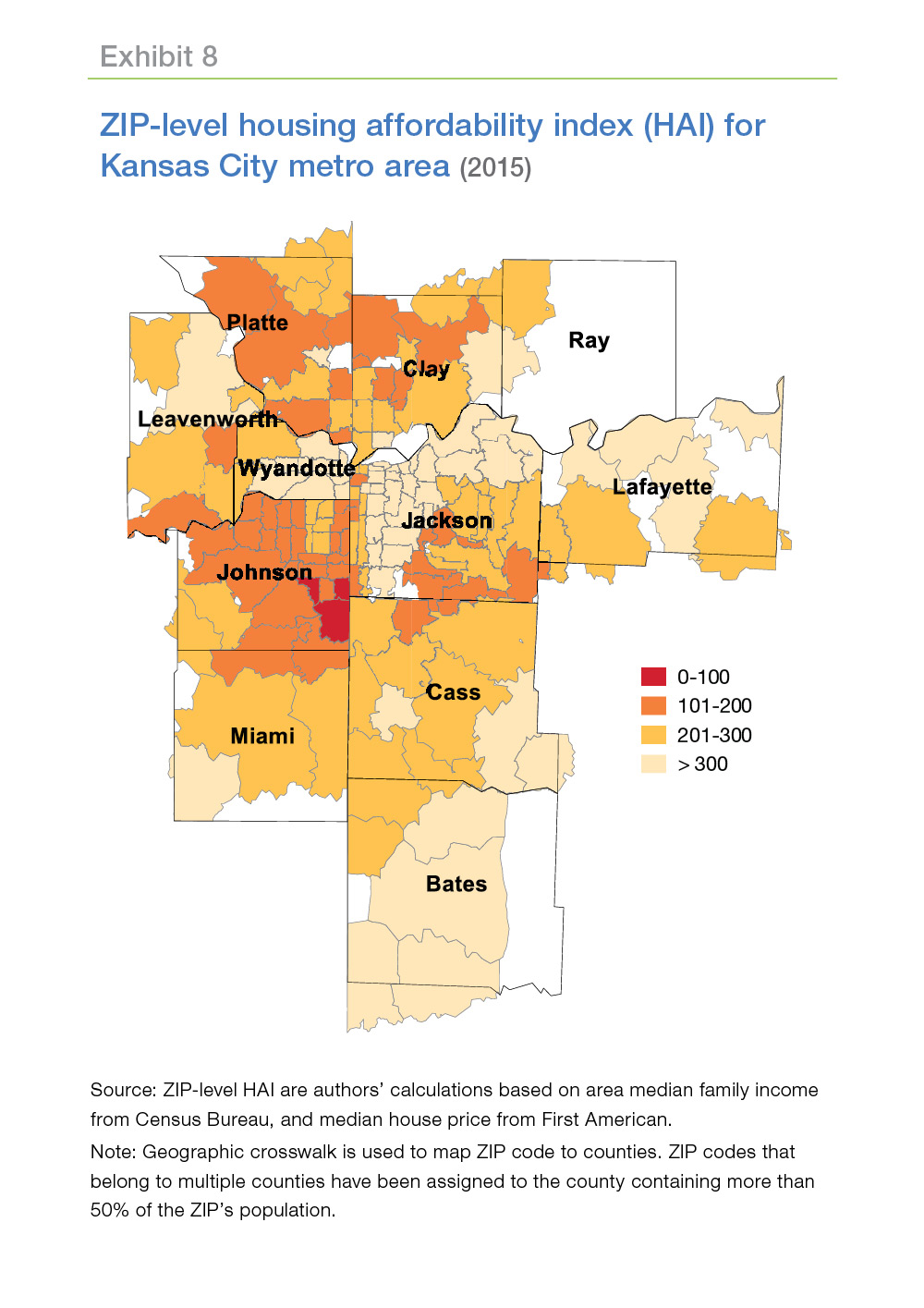

The map of ZIP-level HAIs in Exhibit 6 demonstrates that the high salaries in the San Francisco metro aren’t keeping up with the high house prices in the area. As a comparison, consider the Kansas City metro area, an area with incomes just a bit higher than the U.S. average. Exhibit 7 compares the distribution of family incomes in San Francisco to the distribution in Kansas City. Median family income in San Francisco is 32 percent higher than in Kansas City. But median house prices in San Francisco are 262 percent higher than in Kansas City.

Exhibit 8 displays the ZIP-level HAIs for the Kansas City metro area. Almost the entire map is light orange—in all but three ZIP codes, the median-income family can qualify for a mortgage to buy the median-priced home (HAI>100). Family incomes and house prices are in better balance in Kansas City than in San Francisco. Even ZIP codes close to the central business district of Kansas City are affordable by this measure.

Where do the service workers live?

So far, we’ve concentrated on the affordability of each ZIP code in the San Francisco metro area for the median-income family in each ZIP. But service workers—with lower than- average incomes—also need to find someplace to live.12

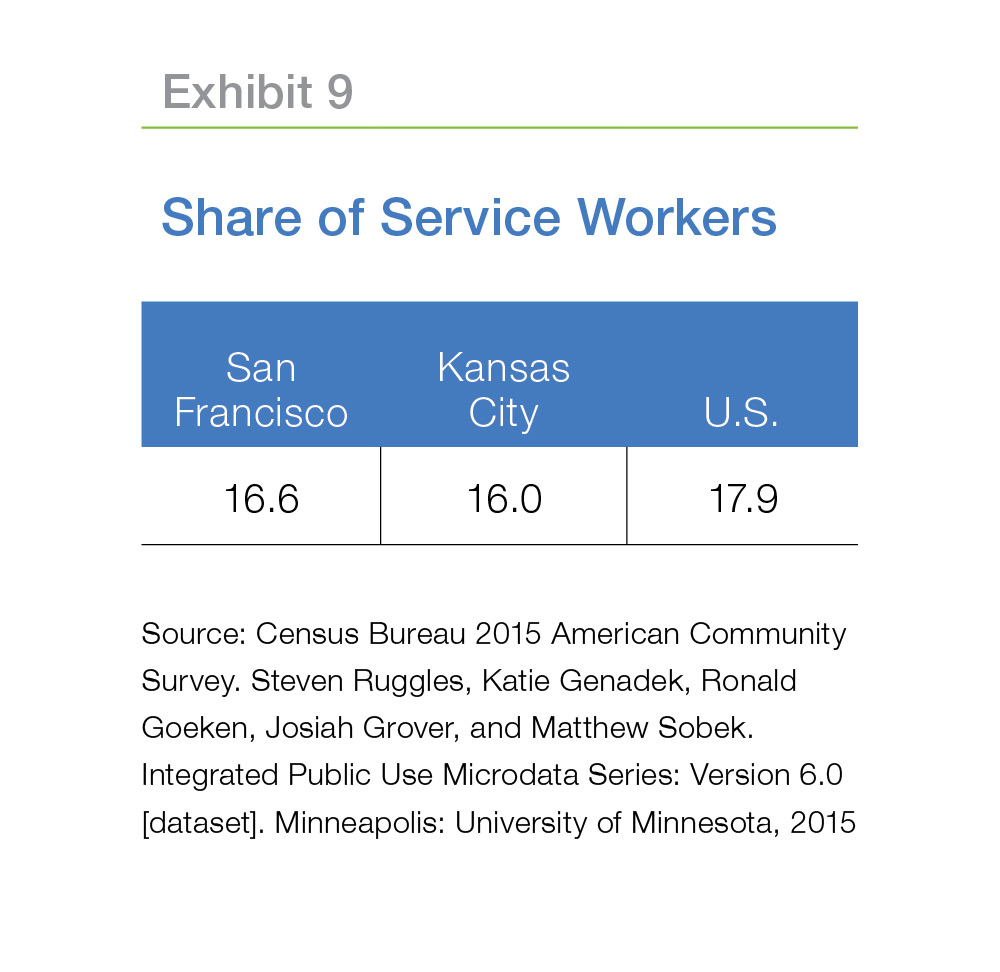

Despite the high cost of living in San Francisco, the share of service workers in the San Francisco area is similar to the share in Kansas City and in the U.S.

Family incomes of service workers are higher in San Francisco than elsewhere, as expected, but the difference is smaller for service workers than for middle-income families. Median family income in San Francisco is 52 percent higher than in the U.S. Median servicer worker family income is only 19 percent higher in San Francisco than in the U.S.13

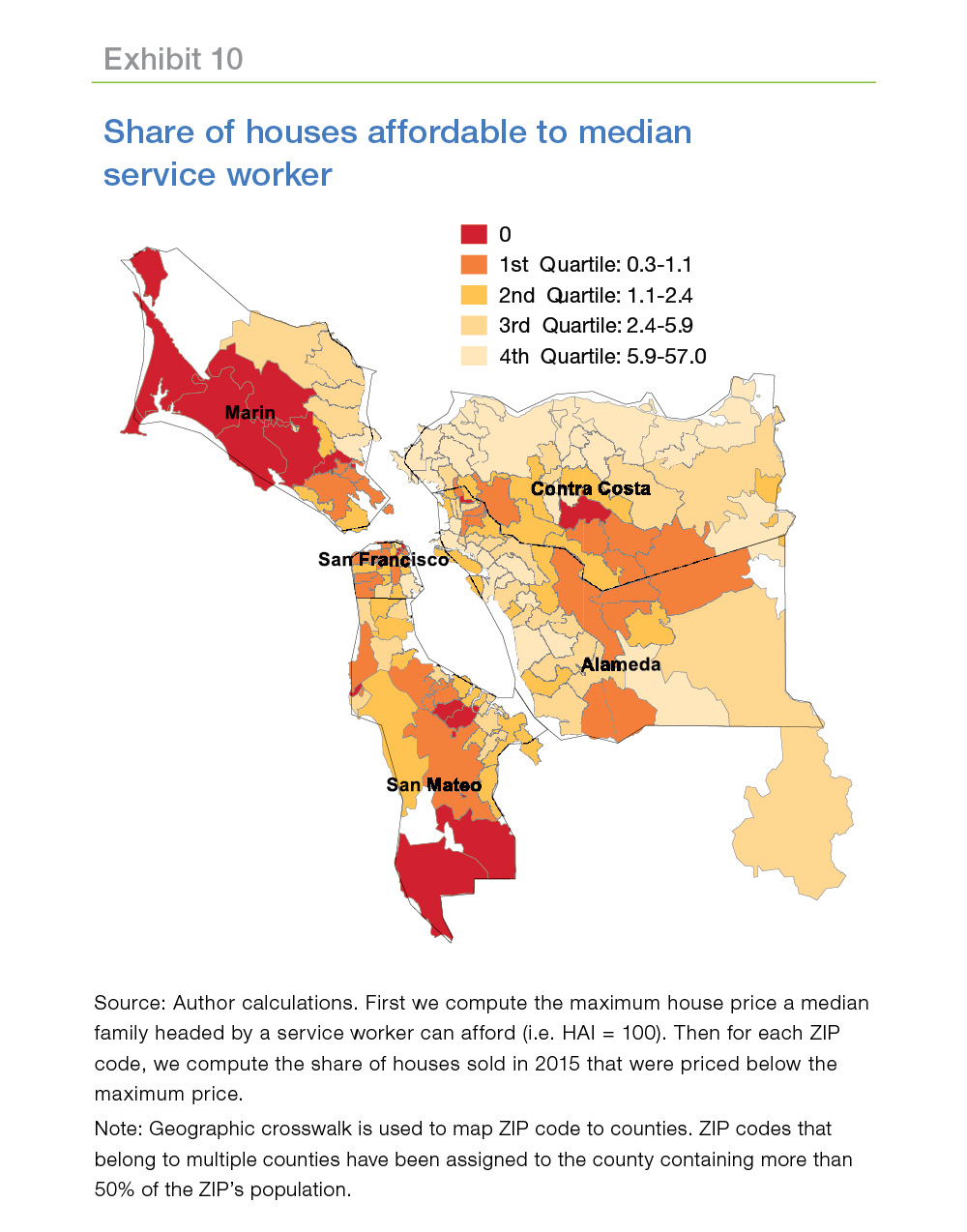

Calculating ZIP-level affordability is more challenging for families headed by service workers than for middle-income families. ZIP-level income for service workers is not readily available. Moreover, it doesn’t make sense to compare service worker family income to the median-price home. For instance, in the San Francisco metro area, there are no ZIP codes where the median-priced house is affordable to a family with the metro-level median service worker family income.14

To get a rough idea of affordability for service workers, we first calculated the house price that would produce an HAI of exactly 100 for the median income of a family headed by a service worker. In San Francisco, that income was $52,000 in 2015. With that income, a house price of $276,000 produces an HAI of exactly 100. Next we calculated the share of houses in each ZIP code that are priced at or below $276,000.15 That defines the affordable pool of houses for families headed by service workers.

Exhibit 10 maps the share of service worker- affordable houses in each ZIP code. Not surprisingly, Exhibit 10 looks similar to Exhibits 5 and 6. Areas with relatively high median house prices tend to have few houses affordable to families headed by service workers.

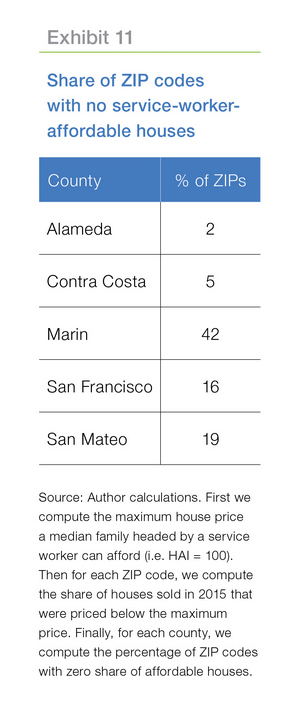

Some ZIPs have no houses that are affordable to service workers. Exhibit 11 lists the percentage of ZIPs in each county with no service-worker-affordable houses. Almost half (42 percent) of the ZIP codes in Marin County have no affordable houses for service workers. As usual, Alameda and Contra Costa counties are more affordable than the other three counties.

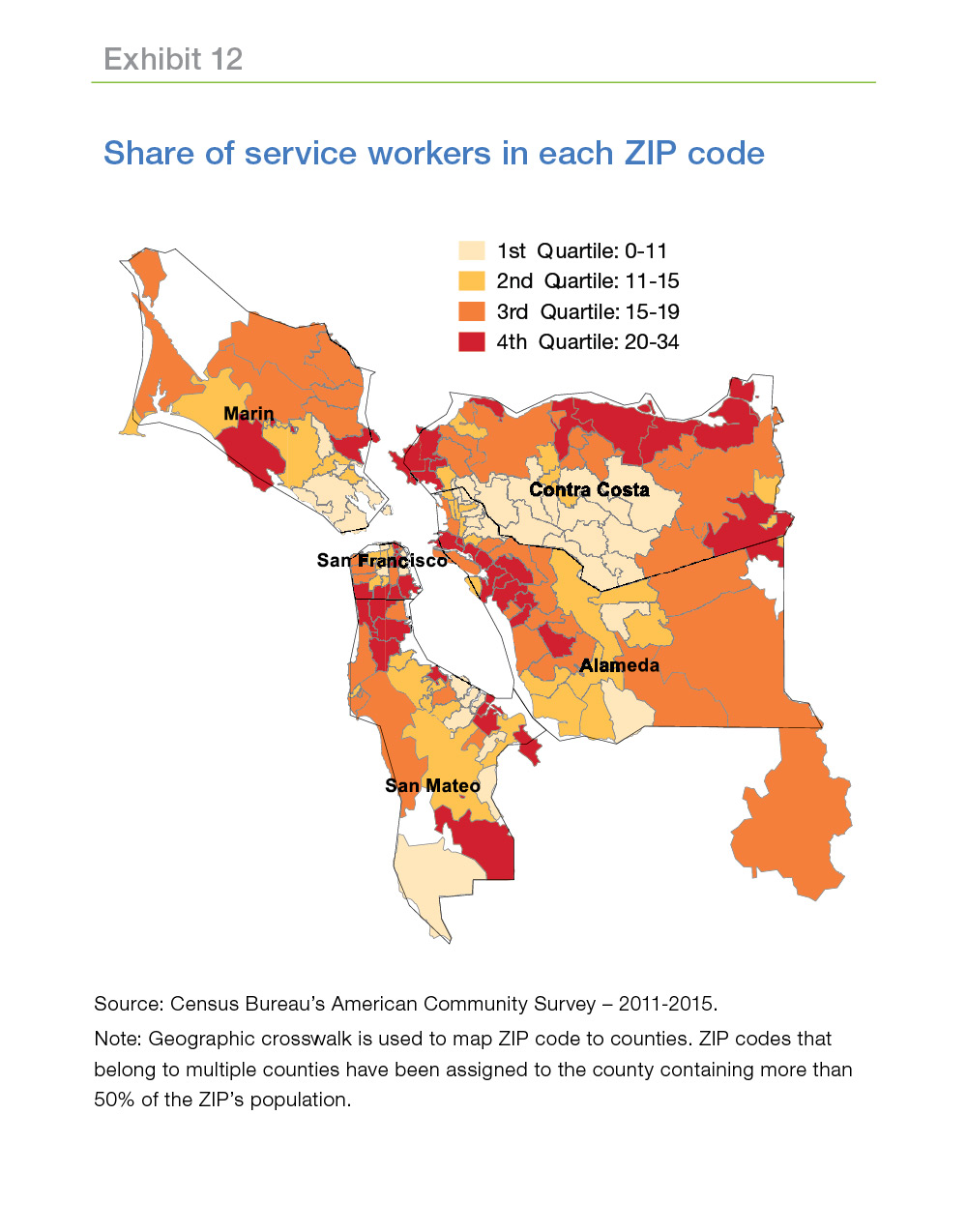

But where do the service workers actually live? Exhibit 12 displays the ZIP-level shares of service workers. For the most part, the share of service workers in a ZIP increases with the share of houses that are affordable for service workers. But some service workers also live in ZIP codes that don’t appear to have any service-worker-affordable houses. On average, service workers comprise 15 percent of the working population in the “unaffordable” ZIPs. Marin, San Francisco, and San Mateo counties have unaffordable ZIP codes where more than 20 percent of the workers are service workers.

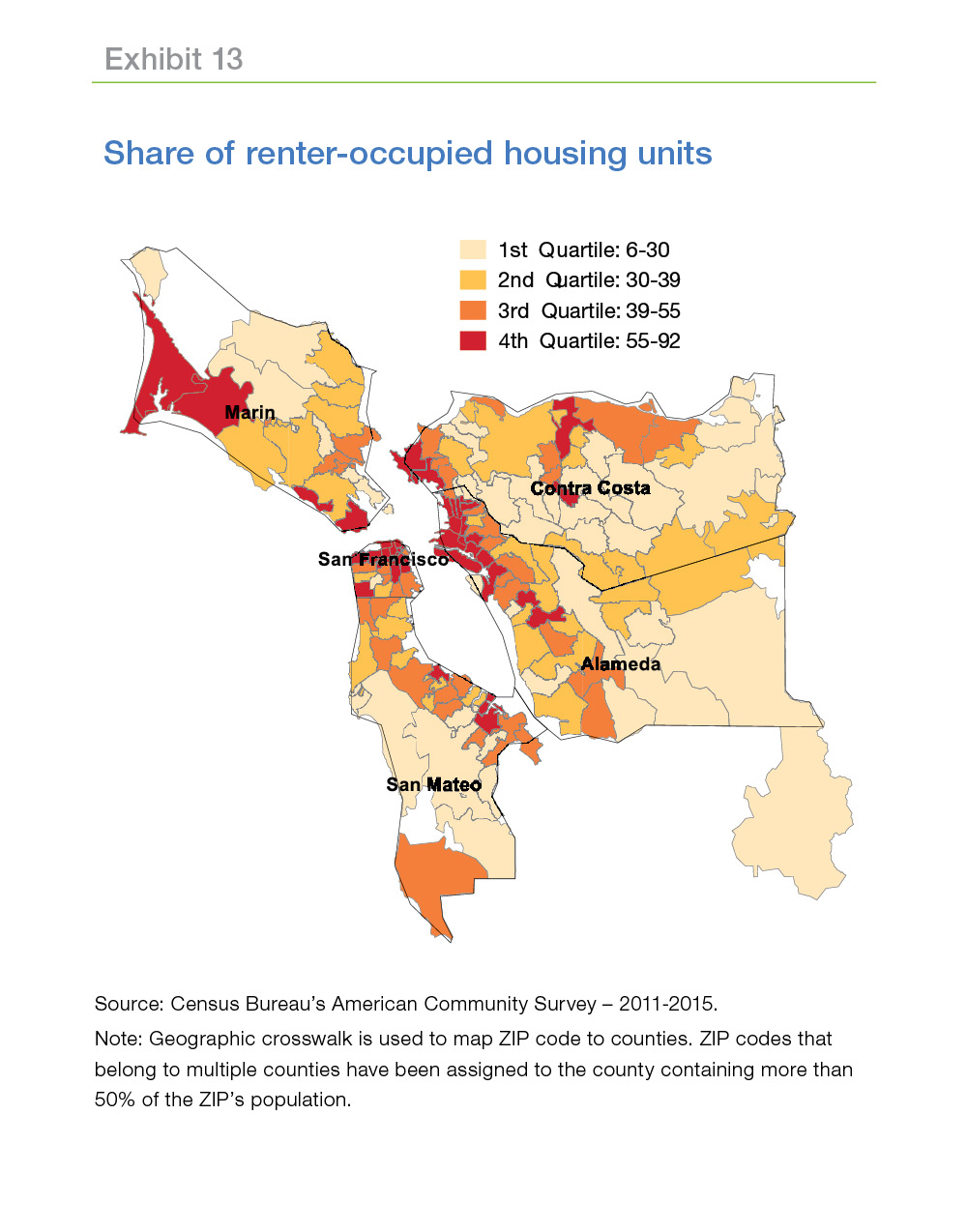

How can lower-income service workers live in some of the most expensive ZIP codes in the San Francisco metro? They rent (and they share rentals). Exhibit 13 displays the share of rental units. Some of the clusters of high rentership include the same ZIPs with a relatively-high share of service workers.

Of course, rents also are expensive in these ZIPs, and service workers are not the only renters in these areas. Many people choose renting near the city center rather than purchasing a home in an outlying area. Younger people, especially those who haven’t started families yet, are attracted by the proximity to jobs and the many amenities of the city, not the least of which is the large number of other young people. Some older people, tired of the upkeep of a house and anxious to return to the attractions of city life, also choose renting.

How well do service workers in San Francisco live?

Almost a quarter of the ZIP codes in the San Francisco metro area are affordable for a middle-income family. But what is the quality of life in those ZIP codes? Do families have to endure enormous commutes in order to find an affordable house? Alternatively, do they have to tolerate sub-par schools, low levels of community amenities and social services, and high levels of crime?

Service workers, because of their lower income, face even tougher trade-offs between affordability and quality of life, especially if they want to own a home. Alternatively, they may choose to rent rather than own, not only because houses are expensive, but also because renting may allow them to live in a more desirable neighborhood.

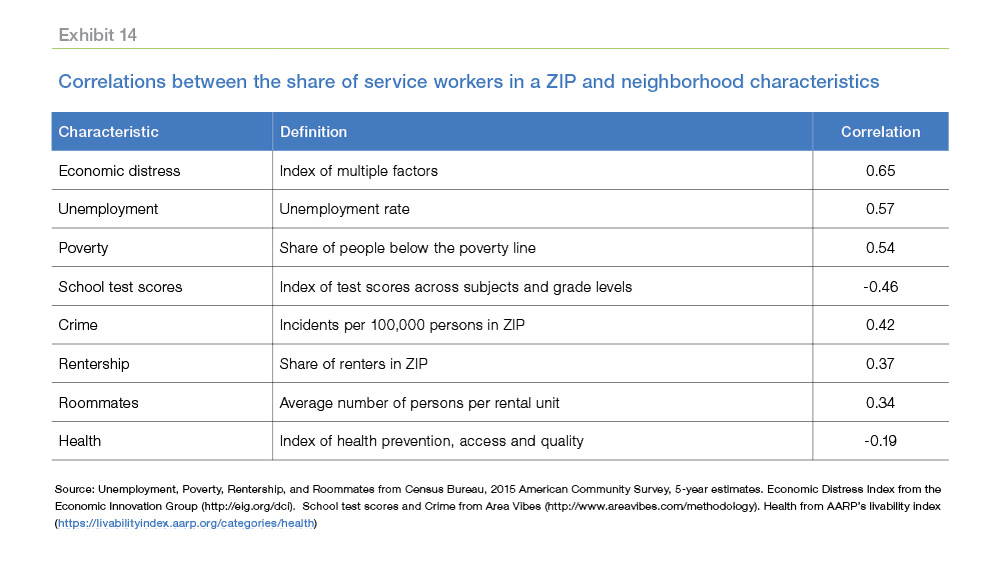

Exhibit 14 lists some significant correlations between the share of service workers in a ZIP code and characteristics that define the quality of life for residents of the ZIP. On average, the higher the share of service workers in a ZIP code, the greater the economic distress, unemployment rate, and share of families below the poverty line. School test scores are lower, and crime is higher. There is a higher share of renters, and there are more people on average in each rental unit. A somewhat weaker correlation indicates poorer access to health care.

It’s also interesting to note some characteristics that are not correlated significantly with the share of service workers in a ZIP code:

- Commute time and distance to the central business district—perhaps because of high rentership near the CBD;

- Age and size of house;

- Availability of transportation;

- Share of people taking public transportation to work;

- Environmental factors such as clean air and water;

- Share of people who walk to work.

Why are we picking on San Francisco?

Because it can take it.

San Francisco is one of the most beautiful cities in the world. The weather is fantastic.16 The area abounds with world-class universities, stellar restaurants, vibrant visual and performing arts communities, and an innovative business environment. It’s no surprise that people are willing to make significant economic sacrifices to enjoy the life the Bay Area offers.

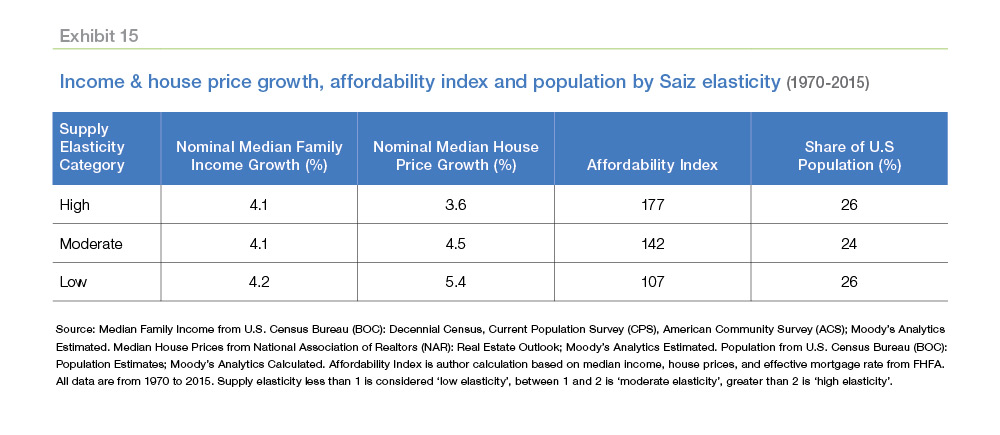

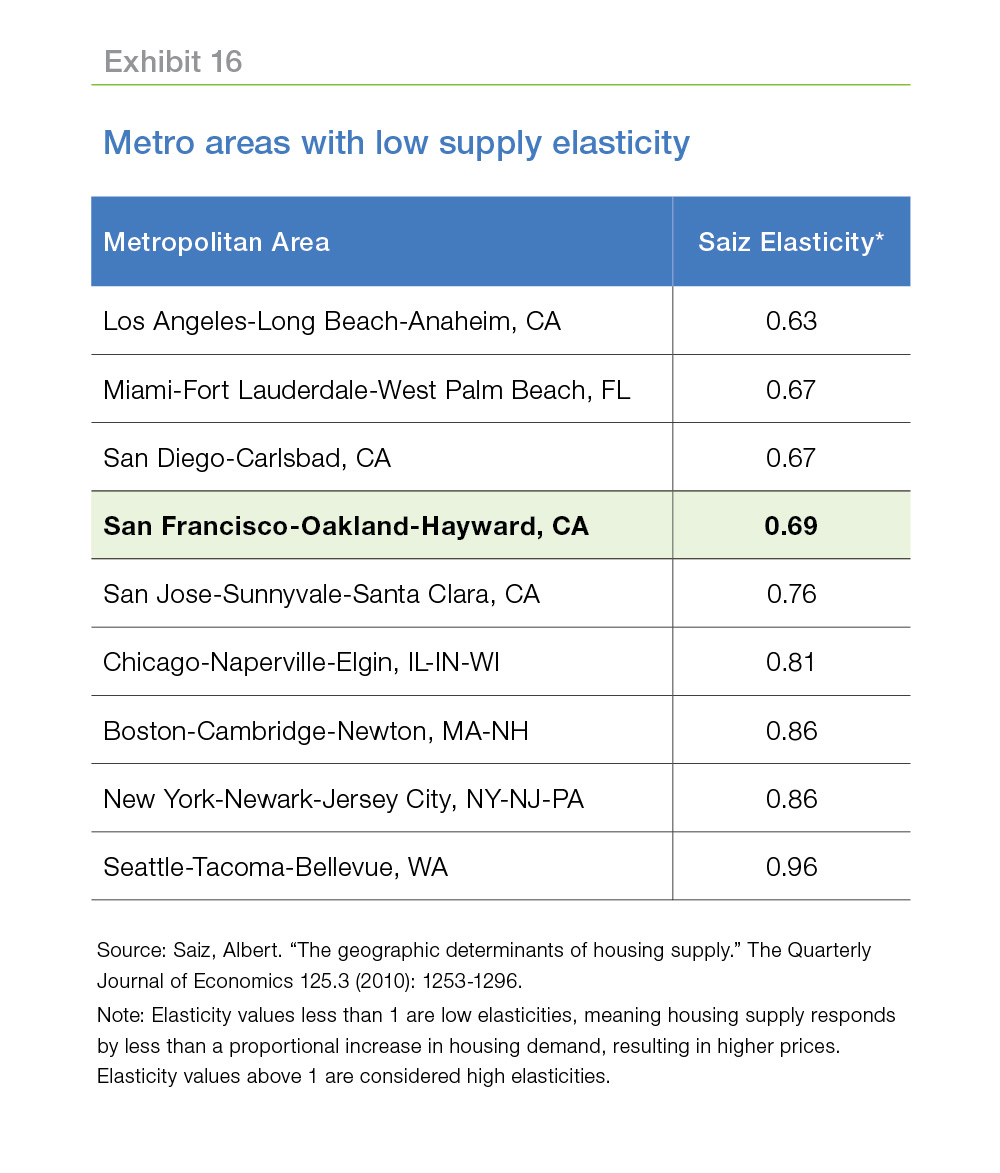

More to the point, San Francisco provides an example of the forces that are shaping the future of housing in the United States.17 Cities and metros differ in their ability to expand the supply of housing in response to increases in the demand for housing. Areas that can expand housing easily are said to have high supply elasticity. In metros with high supply elasticity, a sudden spike in demand will produce a large increase in housing units with only a modest increase in house prices. Alternatively, in metros with low supply elasticity, a spike in demand will drive prices up without much increase in the number of housing units.

Research by Albert Saiz18 identified two key determinants of supply elasticity: the availability of buildable land and the stringency of land use restrictions. Metros with little available buildable land and tight land use restrictions have low supply elasticities.

Exhibit 15 displays long-term growth rates of house prices and family income, the current housing affordability index, and share of the U.S. population for 253 metros categorized by low, moderate, and high supply elasticities.19 Income growth has been almost identical across the three groups, but house prices have risen much faster in areas with low supply elasticities.

San Francisco has a very low supply elasticity. San Francisco is surrounded on three sides by water and is noted for its many hills. Accordingly, there is relatively little buildable land in San Francisco. San Francisco also has tough zoning laws that make it challenging to increase residential density. These factors help explain the rapid growth in house prices in San Francisco and the high cost of housing, even relative to the higher-than-average incomes in the area. The category of metros with low supply elasticities contains some of the most attractive cities in the U.S. Some of the patterns we’ve noted in San Francisco— high housing costs relative to income; difficult trade-offs between housing cost, proximity to work and quality of neighborhood—are likely to be replicated in these other metros.

The simple trick to buying a house in the Bay Area

My parents live in San Mateo County in a ZIP code where the median house price in 2015 was $1.8 million. But they’re not tech millionaires and neither are some of their neighbors. My father was a firefighter, and my mother was a homemaker and later worked at the local high school to help with our college costs. Two doors down, our neighbor worked for the garbage company. My high school sweetheart (now wife) lived around the corner. Her father owned a local hardware store.

How can my middle-class parents afford to live in this high-cost area? Simple. They built their house 50 years ago when the area was largely undeveloped.

This answer is not facetious. It helps explain why the shares of middle-income and lower-income families in the San Francisco metro area are relatively similar to the shares in the U.S. However, many, if not most, of these long-time middle-income and lower-income residents could not—or would not—relocate to the Bay Area today. Some younger families are able to remain in the area without undue hardship only because they inherited their parents’ homes. However, the financial barriers to entry for new firefighters, waste disposal workers, and small business owners remain very high, and these barriers will shape the mix of skills and incomes in the Bay Area in the decades to come.20

If you don’t have a time machine handy, there’s another trick to living in my parents’ ZIP code. A few years ago, Hall of Fame quarterback Joe Montana purchased a house nearby. So all you have to do is win four Super Bowls, and you can move right in.

Conclusion

At the outset, we asked where the service workers in San Francisco live, and how well they live. This has been a long essay with lots of maps and tables, so you may find it useful if we summarize the answers.

Where do the service workers live?

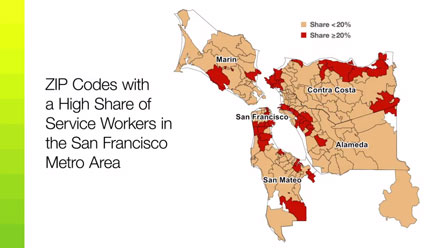

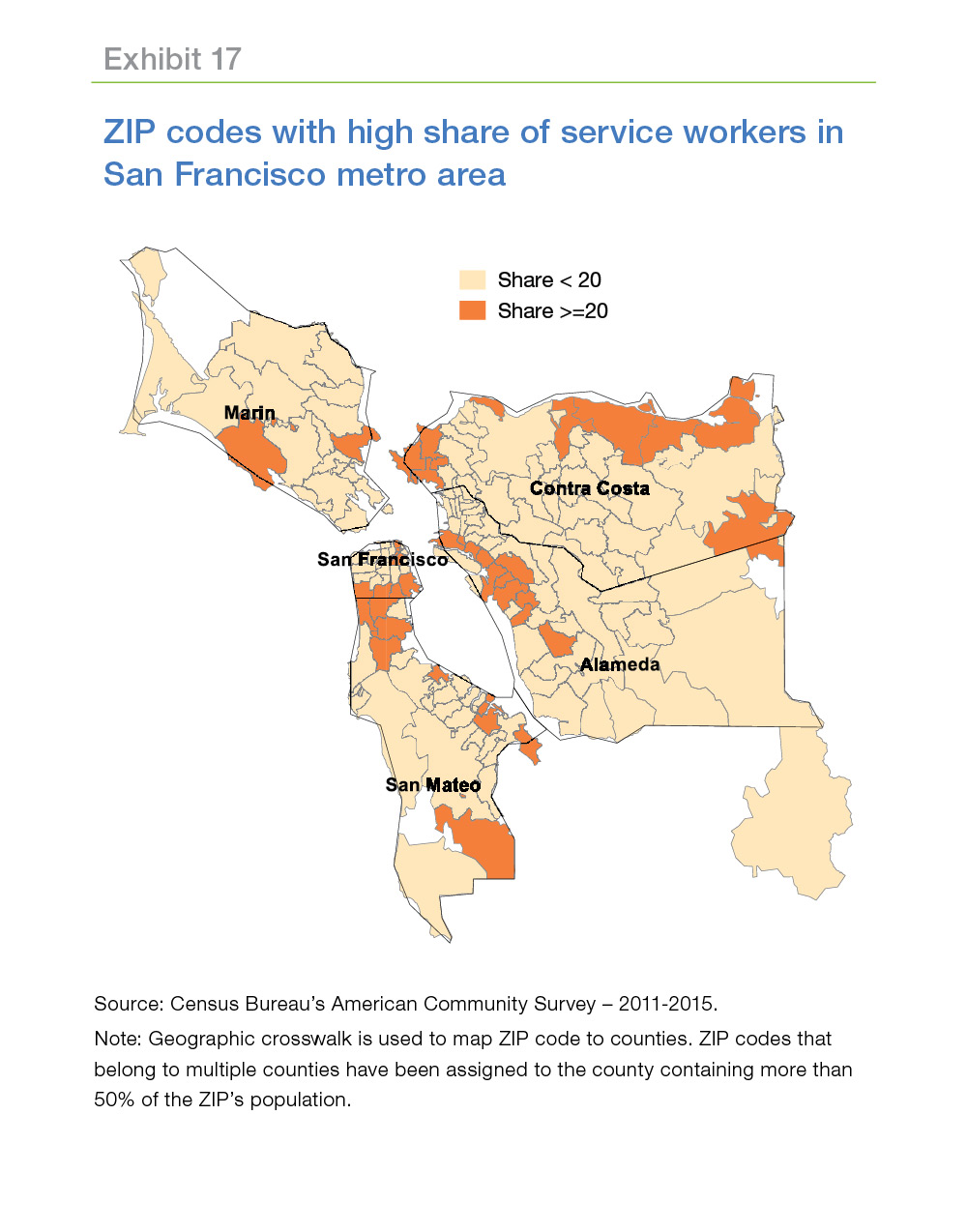

Exhibit 17 highlights ZIP codes where a high share of service workers live.21 We can safely ignore Marin County. Only three ZIP codes in the county have a high share of service workers, and only one of those ZIP codes is a reasonable commute from San Francisco. In addition, the Bay Area Rapid Transit (BART) system doesn’t serve Marin County.

Two areas in the West Bay stand out—the central business district of San Francisco and a cluster of ZIPs on the border between San Francisco and San Mateo counties. Residents in these ZIP codes are most likely to regard San Francisco as the magnet for employment. Two areas in the East Bay also stand out—a band of ZIP codes along the western border of Alameda County and a crescent of ZIP codes along the northern and eastern borders of Contra Costa County. Several BART lines run through the Alameda County band of ZIPs with high servicer work shares, making it possible to commute to San Francisco without driving and parking a car. BART service is more limited in Contra Costa County, and service workers in the Contra Costa crescent who are distant from a BART station may concentrate their job search closer to home.

How well do they live?

It varies.

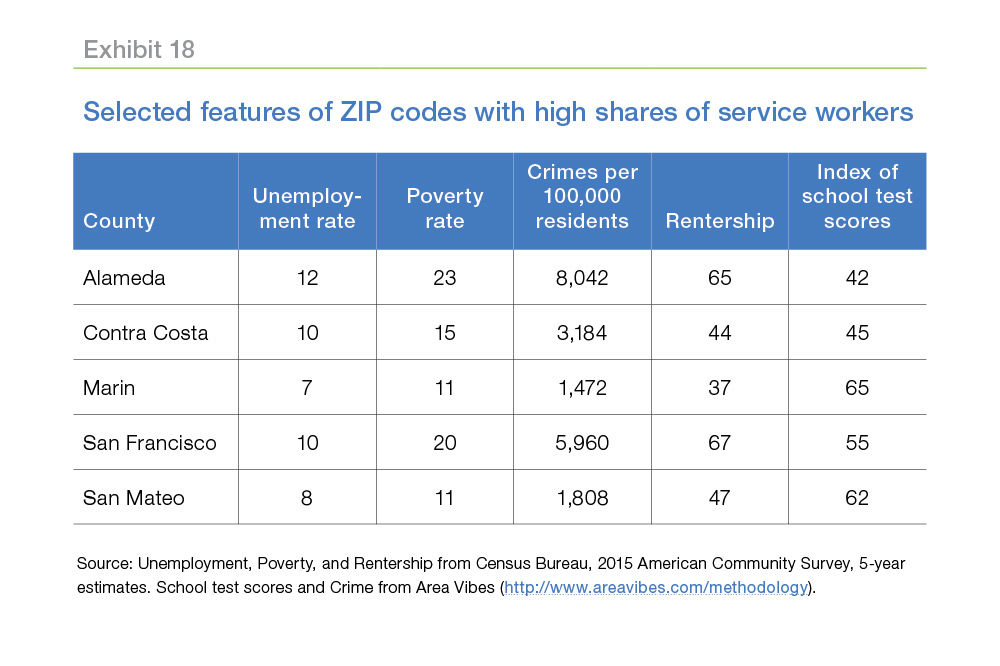

Exhibit 18 compares selected neighborhood features across the highlighted ZIP codes in each county. Residents in high-servicer-share ZIP codes in Alameda and San Francisco counties face particularly challenging conditions. The unemployment and poverty rates are much higher than the average for the entire San Francisco metro area. Crime also is high, even compared to the highlighted ZIP codes in neighboring counties. Contra Costa county has elevated unemployment and poverty rates, but its crime rate is not significantly higher than the metro area average. Both Alameda and Contra Costa counties have low school test scores, but San Francisco is close the metro area average.

The pattern of rentership in Exhibit 18 suggests that servicer workers’ location decisions are tied closely to their choice of renting or owning. In San Francisco County, ZIP codes with high shares of service workers have high rentership rates. In Alameda County, which offers rapid transit options to San Francisco, rentership also is high. In Contra Costa County, which has less access to rapid transit, high-servicer-share ZIP codes have the same rate of rentership as the metro area average.

At the risk of oversimplification, we hypothesize that service workers in San Francisco County are predominantly single, unmarried or married without children, and interested in the amenities offered by a major city like San Francisco. Service workers in Contra Costa County appear to place a high value on home ownership and are willing to locate in an area that is distant from San Francisco and that has more-limited access to rapid transit. This group is likely to have a larger share of families with children. Alameda County is the in-between case. Ready access to San Francisco appears to be the only counterbalance to the high unemployment, poverty, and crime rates and the low school quality.

Will net migration slowly drain the stock of service workers and middle-income families?

While it is difficult to quantify, it is likely that many lower- and middle-income residents in the San Francisco metro area are “legacies”. They can afford to live in the area either because they settled in the area before it became so expensive, they inherited a house, or family ties have incented them (and family financial assistance has enabled them) to remain in the area.

How will San Francisco react to the likely net loss of lower- and middle-income families over the next few decades? Will city and county governments in the metro area implement programs to subsidize or otherwise sustain housing affordability for lower- and middle-income families? Will wages for lower- and middle-skill jobs be bid up as the pool of these workers shrinks? Will companies leverage technology to economize on the need for these skill sets? Or will the cost of living moderate? Will the adjustments in San Francisco be echoed by similar trends in other high-cost metros? The nature of the Bay Area’s urban ecosystem will be shaped in large part by these adjustments, whatever they turn out to be.

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP

Sean Becketti, Chief Economist

Kadiri Karamon, Quantitative Analyst

Opinions, estimates, forecasts and other views contained in this document are those of Freddie Mac’s Economic & Housing Research group, do not necessarily represent the views of Freddie Mac or its management, should not be construed as indicating Freddie Mac’s business prospects or expected results, and are subject to change without notice. Although the Economic & Housing Research group attempts to provide reliable, useful information, it does not guarantee that the information is accurate, current or suitable for any particular purpose. The information is therefore provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution. Alteration of this document is strictly prohibited.

1 http://cost-of-living.careertrends.com/l/60/San-Francisco-CA-Metro-Area#Cost%20of%20Living%20Calculators&s=44CZLp

2 Authors’ calculations based on First American property transaction data.

3 Census Bureau, 2015 American Community Survey, 1-year estimates.

4 https://www.redfin.com/blog/2016/09/has-san-francisco-real-estate-finally-reached-its-max.html

5 For San Francisco, U.S. Census Bureau: Current Population Survey - Housing Vacancy Survey; Moody’s Analytics Estimated. For U.S., U.S. Census Bureau: Housing Vacancies & Homeownership Rates.

6 The "standard" mortgage is a 30-year fixed-rate mortgage with a 20 percent down payment and a debt-to-income ratio of 25 percent. In practice, there is no such thing as a standard mortgage, but these assumptions make possible consistent comparisons across areas.

7 https://www.huduser.gov/portal/ushmc/hd_hsg_aff.html

8 The cost burden estimate is available only for the median-income household in each metro. There are no metros where the median-income household is severely cost burdened, however many actual households are severely cost burdened.

9 To improve the readability of Exhibit 4—and many of the other exhibits below—we’ve dropped ZIP code 94027 (Atherton), the second-most-expensive ZIP code in the country, with a median house price of $5.6 million. If you happen to be driving through 94027, you can stop and say howdy to some of the heads of Google, Facebook, Hewlett Packard, ...

10 Remember that the ZIP-level HAI relies on the median family income in that ZIP code, so the higher incomes of the more-affluent should already be accounted for.

11 Then there is the much trickier question of the income elasticity of demand for housing. In other words, as individuals become wealthier, do they choose to consume a smaller or a greater share of their budget on housing? Research on this question is unsettled. See De Leeuw, Frank. 1971. “The Demand for Housing: A Review of Cross-section Evidence.” The Review of Economics and Statistics 53 (1): 1-10, Mayo, Stephen K. 1981. “Theory and Estimation in the Economics of Housing Demand.” Journal of Urban Economics 10: 95-116., and Harmon, Oskar R. 1988. “The Income Elasticity of Demand for Single-Family Owner-Occupied Housing: An Empirical Reconciliation.” Journal of Urban Economics 24: 173-185 for summaries of what we know so far.

12 Service occupations in this article have been defined using Census Bureau’s 2010 occupation codes and include the following categories of workers: Healthcare Support Occupations, Protective Service Occupations, Food Preparation and Serving Related Occupations, Building and Grounds Cleaning and Maintenance Occupations, Personal Care and Service Occupations.

13 Median servicer worker family income is $52,400 in San Francisco and $44,100 in U.S (19 percent = 100*(52400/44100 -1). Source: Census Bureau 2015 American Community Survey. Steven Ruggles, Katie Genadek, Ronald Goeken, Josiah Grover, and Matthew Sobek. Integrated Public Use Microdata Series: Version 6.0 [dataset]. Minneapolis: University of Minnesota, 2015

14 In Kansas City, the median income of a family headed by a service worker would qualify to buy the median-priced home in two-thirds of the ZIP codes.

15 The house price information comes from First American Mortgage Solutions and reflects recent transactions. The distribution of transaction prices may not be representative of the values of all the houses in a ZIP.

16 The official motto of Redwood City, in San Mateo County, is “Climate Best By Government Test”. They even have a sign to prove it.

17 http://www.freddiemac.com/research/insight/20161116_trends_shaping_housing.html

18 Saiz, Albert. “The geographic determinants of housing supply.” The Quarterly Journal of Economics 125.3 (2010): 1253- 1296.

19 The population shares add up to less than 100 percent because supply elasticities are not available for all metros and because a significant share of the population lives outside of metro areas.

20 For U.S. trends see: David Autor, “The Polarization of Job Opportunities in the US Labor Market, “The Hamilton Project, April (2010). For International trends see for example: Maarten Goos, and Alan Manning, “Lousy and Lovely Jobs: The Rising Polarization of Work in Britain.” Review of Economics and Statistics 89, no. 1 (2007): 118-133.

21 Exhibit 17 highlights ZIP codes where more than 20 percent of the residents are service workers.