Will the Hispanic Homeownership Gap Persist?

This is the American story.

A wave of immigrants arrives in the U.S. Perhaps they're escaping religious or political persecution. Perhaps a drought or famine has driven them from their homes. Perhaps they simply want to try their luck in the land of opportunity.

They face new challenges in America. Often they arrive with few resources. And everything about them sets them apart—their religions, their languages, their cultures, their foods, their appearances. They are not always welcomed. They frequently face discrimination in housing, jobs, education, and more. But over time, they plant their roots in American soil. They become part of the tapestry that is America. And they thrive.

This is the story of the Germans and Italians and many other ethnic groups that poured into the U.S. a century ago.

Today's immigrants come, for the most part, from Latin America and Asia instead of Europe. Hispanics comprise by far the largest share of the current wave. Over the last 50 years, more than 30 million Hispanics migrated to the U.S. And these Hispanics face many of the same challenges as earlier European immigrants.

Homeownership provides a key measure of transition from a newly-arrived immigrant to an established resident. Many immigrants arrive without the financial resources needed to purchase a home. In addition, the unfamiliarity and complexity of the U.S. housing and mortgage finance systems pose obstacles to homeownership. As a result, homeownership rates start low for new immigrants but rise over time.

The homeownership rate among Hispanics in the U.S.—a population that includes new immigrants, long-standing citizens-, and everything in between— stands around 45 percent, more than 20 percentage points lower than the rate among non-Hispanic whites. Much of this homeownership gap can be traced to differences in age, income, education and other factors associated with homeownership.

Will the Hispanic homeownership gap close over time, as it did for the European immigrants of a century ago? Or will a significant gap stubbornly persist, as it has for African-Americans?

Who are the Hispanics?

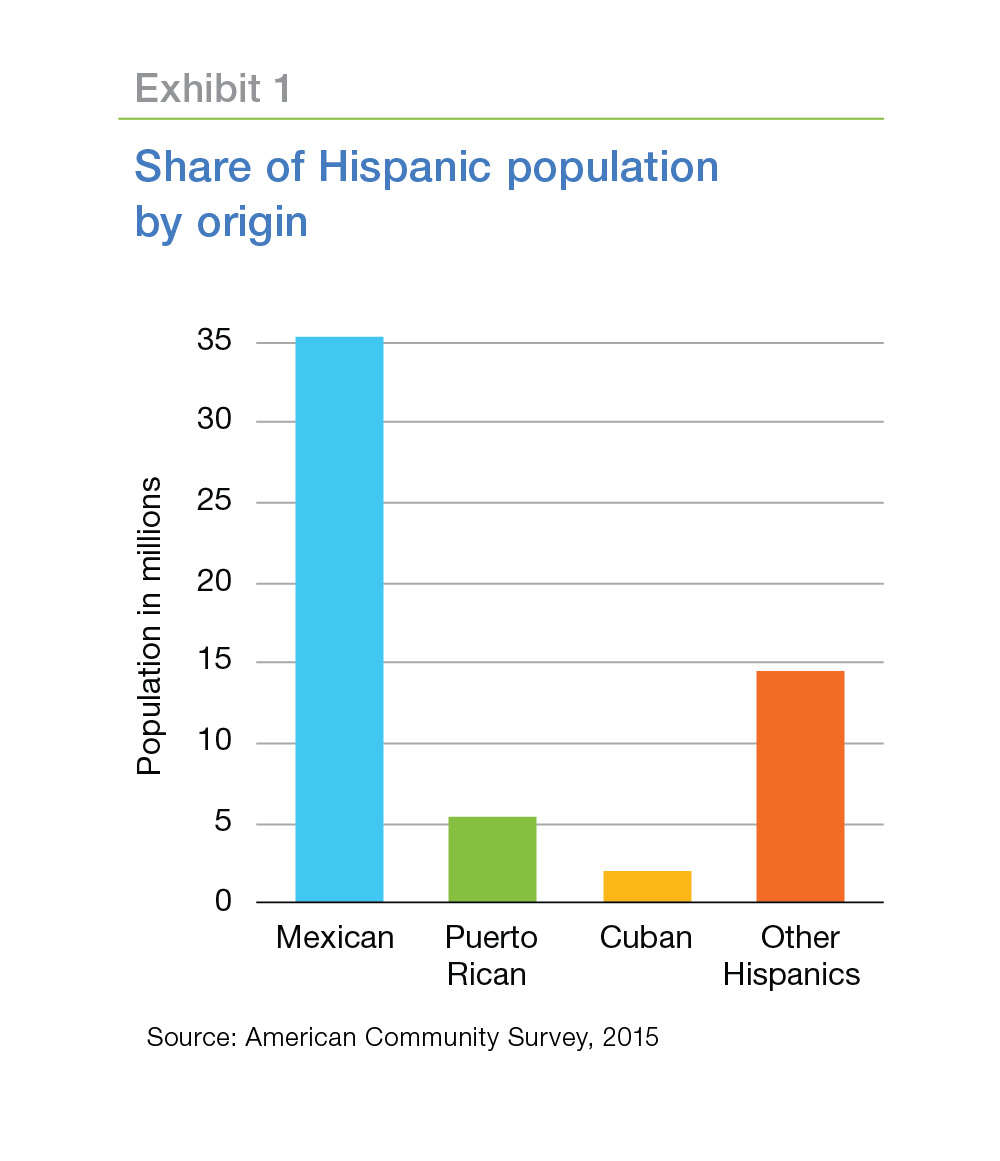

Hispanics comprise a diverse group of people who identify themselves as being of Spanish-speaking background and trace their origin or descent to Mexico, Puerto Rico, Cuba, Central and South America and other Spanish-speaking countries. Among Hispanics in the U.S., nearly two-thirds are of Mexican origin (Exhibit 1). Puerto Ricans make up nine percent of Hispanics in the U.S. followed by Hispanics of Cuban origin at just under four percent.

Hispanics of Mexican origin represent not only the largest subgroup of Hispanics in the U.S. they are also the largest immigrant group in all but 19 of the 50 states (Exhibit 2). Various non- Mexican Hispanics form the largest immigrant groups in nine of the remaining states plus the District of Columbia.1

Sixty-six percent of Hispanics are U.S. citizens, some of whom are second, third, or even later- generation residents. Another 11 percent are permanent residents, that is, green card holders. Ten percent are here in a variety of temporary categories, some of which may lead to permanent residency. And an estimated 13 percent are undocumented immigrants.

Puerto Ricans and Hispanics of Cuban origin enjoy a privileged status compared to other immigrants. Puerto Ricans are U.S. citizens, so, like all U.S. citizens, they can come and go within the United States without restriction. Virtually all Cuban immigrants have been admitted under a special parole power of the U.S. Attorney General.2

Hispanics are 10 years younger than non-Hispanic whites (Whites) on average. The share of Hispanics with a Bachelor's degree is slightly less than half the White share. The median household income of Hispanics is just short of three-quarters of White median household income.

How big is the Hispanic homeownership gap?

Homeownership increased for all racial and ethnic groups from the mid-1990s and reached a peak just prior to the housing crisis in the mid-2000s. Exhibit 4 displays the homeownership trends for Hispanics and Whites. Homeownership rates have declined since that peak and currently stand slightly higher than the 1995 level for both Hispanics and non-Hispanic whites (Whites).

The White/Hispanic homeownership gap narrowed over this 20-year period, from just under 29 percentage points in 1995 to 26 percentage points in 2015 (Exhibit 5).

What accounts for the Hispanic homeownership gap?

The homeownership rate among Hispanic households is influenced by the same factors that influence the homeownership rate of Whites. For instance, age, as a proxy for stage of life, is a powerful predictor of the probability of homeownership. As people grow older, they are more likely to get married and have children—factors that increase the likelihood of homeownership. Similarly, more educated and more affluent individuals are likelier to be homeowners. Much of the Hispanic homeownership gap can be explained by Hispanic/non-Hispanic differences in these factors.

Exhibit 6 ranks the impact of the most influential of these factors on the homeownership gap between Whites and Hispanics.3 To simplify the discussion, we focus on the results for Hispanics of Mexican origin the largest Hispanic sub-group.4 But similar results hold for the other Hispanic sub-groups.5

Supporting the Hispanic Community

Some of the steps that we have taken to better serve Hispanic borrowers and help them overcome potential cultural and language barriers, as well as other considerations that traditional underwriting methods don’t take into account, include the following:

CreditSmart Español®

CreditSmart Español helps potential borrowers build and maintain better credit, make sound financial decisions, and understand the steps to sustainable homeownership.

Spanish Translations of Mortgage Documents

Freddie Mac and Fannie Mae offer Spanish translations of Freddie Mac/Fannie Mae Uniform Instruments to help lenders and others in the residential mortgage industry better serve Spanish-language-dominant consumers in becoming homeowners.

Test and Learn

As part of an ongoing test and learn launched in 2016, we are working with two lenders with demonstrated expertise in the Hispanic market to fine-tune the requirements for our low-down payment Home Possible® mortgages to specifically address the needs of Hispanic borrowers.

Borrower Help Centers

Counselors at our Borrower Help Centers offer bilingual services and are trained to help in a variety of situations related to buying and owning a home, including offering pre-purchase counseling or assistance when homeowners are struggling financially.

We also work with organizations such as the National Association of Hispanic Real Estate Professionals (NAHREP), and National Council of La Raza (NCLR) to better understand and support the needs of the Hispanic community.

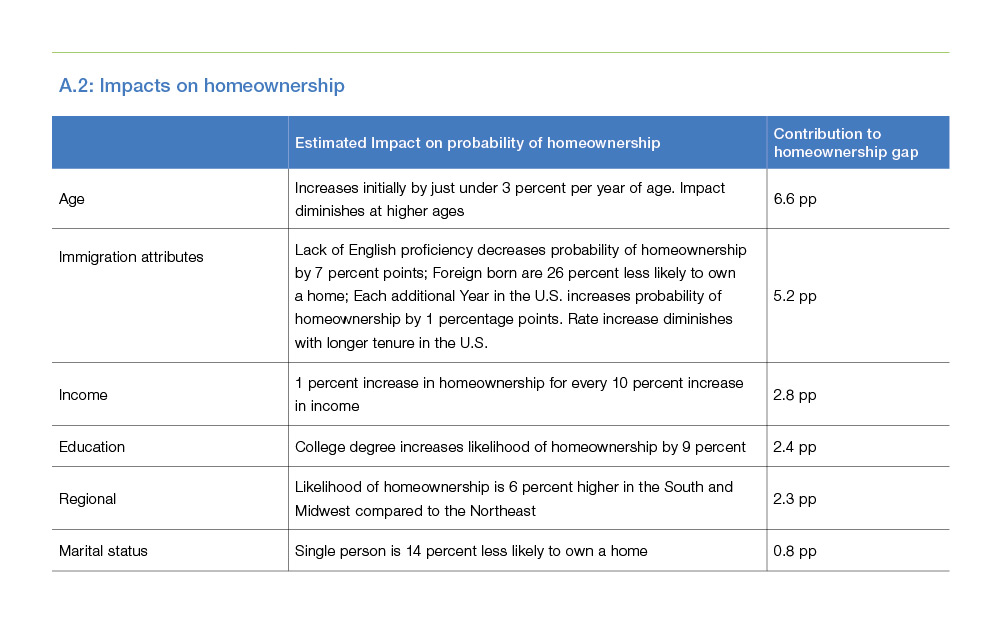

Age is the most important factor influencing the homeownership gap.6 Other things being equal, a 35-year-old is 15 percentage points likelier to be a homeowner than a 25-year-old. Accordingly, the 11-year difference in the average age of Whites and Hispanics of Mexican origin explains almost seven percentage points of the 23-percentage point difference in 2015 (30 percent of the White/Mexican-origin Hispanic homeownership gap).

A combination of immigration-specific attributes are the next-most-impactful factors, accounting for six percentage points of the White/Mexican-origin Hispanic homeownership gap. These attributes include whether a Hispanic of Mexican-origin is foreign-born (first-generation immigrant), the number of years they have resided in the U.S., and their level of English language skills. Differences in income, education, and the region of residence each explain between 1 and 3 percentage points of the homeownership gap. The shares of married Whites and Hispanics of Mexican origin are almost identical, so marital status accounts for very little of the homeownership gap.

About three percentage points (13 percent) of the homeownership gap between Whites and Hispanics of Mexican origin cannot be explained by differences in age, education, and other observable factors.7

Will the homeownership gap narrow?

The analysis of the previous section suggests that almost 90 percent of the White/Mexican-origin Hispanic homeownership gap can be attributed to age, immigration attributes, income, and the like. If White/Mexican-origin Hispanic differences in those characteristics narrow over time—if, for example, the difference in the average age of Whites and Hispanics of Mexican origin disappears—the gap in homeownership also is likely to narrow. So, the question becomes, will those differences between Whites and Hispanics of Mexican origin disappear? And, if so, how quickly?

To answer these questions thoroughly, we need to forecast the future Whites and Hispanics of Mexican origin's trends in age, income, education, and the other characteristics included in our analysis—a task that is beyond the scope of this article. However, thanks to the work of the Census Bureau, we can hazard a guess about the impact of changes in the age distribution of the White and Mexican-origin Hispanic populations.

As we noted above, differences in age account for 30 percent of the White/Mexican-origin Hispanic homeownership gap. The Census Bureau publishes projections of the age distribution of the White and Hispanic populations in the U.S.8 Exhibit 7 displays the Census's baseline projections of the average age of Whites and Hispanics from 2015 through 2060. These projections incorporate Census estimates of fertility and mortality in each group and of the net migration and age of Hispanic immigrants.9

The Census expects the average age of Whites to increase by six years over the next 45 years, from 43 in 2015 to 49 in 2060. The average age of the Hispanic population is expected to increase by almost 10 years over the same period. The gap in average age is projected to drop from 11 years today to eight years in 2060.

Net immigration is expected to restrain the increase in the average age of Hispanics. Immigrants are, on average, five years younger than Americans of Hispanic descent. In addition, the average age of Hispanic immigrants is projected to increase by just over three years by 2060 for resident Hispanics.

The modest narrowing of the age gap is expected to reduce the homeownership gap by an equally-modest amount: three percentage points by 2025 and 5.1 percentage points by 2035 (Exhibit 8). This estimate is best understood as a lower bound of future growth in Hispanic homeownership. Changes in other factors such as income and education will influence homeownership as well, and these changes are likely to reduce the Hispanic homeownership gap further.

More importantly, this estimate incorporates Census projections of net migration, which masks the progress of resident Hispanics. New immigrants are younger and less-educated on average than resident Hispanics. Moreover, immigrants are likelier to have limited English proficiency when they arrive in the U.S. These factors reduce the homeownership rate of new immigrants relative to long-time residents.

Restricting attention to resident Hispanics provides a different perspective on future Hispanic homeownership. Exhibit 9 compares two projections of the share of foreign-born Hispanics10 and of the age of Hispanics. The baseline projection includes the Census projection of all Hispanics in the U.S., both current residents and future immigrants. The current residents' projection includes only those Hispanics residing in the U.S. as of 2015. Note that as of 2015, 55 percent of resident Hispanics were foreign-born. That share drops by four percentage points by 2025 relative to the baseline projection and by eight percentage points by 2035. In addition, the average age increase for current residents is five years by 2035.

Exhibit 10 compares these two projections of the Hispanic homeownership rate. In the baseline projection, the Hispanic homeownership rate increases from 46 percent in 2015 to 50 percent in 2025 and 52 percent in 2035. However, the homeownership rate rises much faster for current residents, to 55 percent in 2025 and 62 percent in 2035. This more-rapid increase in the homeownership rate also narrows the homeownership gap more rapidly (Exhibit 11). In the baseline projection, the 26-percentage point gap in 2015 drops to 22 percentage points in 2025 and 20 percentage points in 2035. For current residents, the gap narrows to 16 percentage points in 2025 and 9 percentage points in 2035.

Other influences on the homeownership gap

White/Mexican-origin Hispanic differences in income and education account for approximately 20 percent (two percentage points) of the homeownership gap. It's difficult to predict the likelihood of closing the gaps in these factors over the next 10-20 years. In the 20th century, income and education

attainment tended to increase with each generation. A common progression might have a generation with no formal schooling followed by a generation with, perhaps, an eighth grade education. The next generation might complete high school, while their children attended college. And each generational advance in educational attainment is accompanied by an increase in family income.

Mexican-origin Hispanic residents might follow a similar pattern, with each generation chipping away at the income and education gaps between Hispanics of Mexican-origin and Whites. However, other U.S. trends may present obstacles to Mexican origin Hispanic's socioeconomic progress. In a previous article, “Three Trends That are Shaping the Future of Housing”, we highlighted the so-called polarization of jobs; that is, the loss of middle-skill jobs and the simultaneous growth in both low-skill and high-skill jobs. This well-documented polarization tends to eliminate a traditional stepping stone in generational progress by reducing opportunities for people with moderate amounts of education. At the same time, and partially for the same reasons, the distribution of income in the U.S. has become more unequal over time. It remains to be seen if this is a temporary phenomenon, traced perhaps to the economic upheavals of the mid-2000s, or a long-term trend that may thwart generational progress to higher socioeconomic levels.

Differences for non-Mexican Hispanics

While Hispanics of Mexican origin are the largest Hispanic sub-group in the U.S., 36 percent of resident Hispanics are not of Mexican origin. Moreover, the non-Mexican Hispanics differ from Hispanics of Mexican origin in ways that affect their current and future likelihood of homeownership.

Puerto Ricans and Hispanics of Cuban origin are the other two largest Hispanic sub-groups in the U.S. Hispanics of Cuban origin have higher homeownership rates than both Hispanics of Mexican-origin and Puerto Ricans. They are older and have higher incomes contributing to higher homeownership rates. Puerto Ricans on the other hand have the lowest homeownership rates. Puerto Ricans are younger and have higher levels of single householders, two factors that have been associated with low homeownership rates.

Conclusion

For decades, the homeownership rate of Hispanics has remained over 20 percentage points below the rate for Whites. This homeownership gap has narrowed in recent years, but very slowly.

Most of the White/Hispanic gap can be traced to population differences in the characteristics that influence homeownership in the U.S.: age, English proficiency, income, education, etc. If these differences are reduced in the future, some of the homeownership gap can be eliminated. For instance, if the age difference between Whites and Hispanics of Mexican origin is eliminated, as much of 30 percent of the White/Mexican-origin Hispanic homeownership gap may close.

Census projections of future age distributions suggest that the age differences of Whites and Hispanics will be reduced by six percent (0.7 years) by 2025 and 12 percent (1.2 years) by 2035. If these projections are realized, the White/Hispanic homeownership gap is likely to narrow by 20 percent (five percentage points) by 2035. The Census projections include both current residents and future immigrants, and averaging the characteristics of these two groups of Hispanics tends to mask the relatively-rapid growth in homeownership among the current residents.

It is important to remember that about 13 percent of the White/Hispanic homeownership gap cannot be traced to population characteristics such as age and income. The explanation for this residual gap is unclear, although some of it may be due to wealth gaps and discrimination.

Appendix: Estimating the factors influencing homeownership

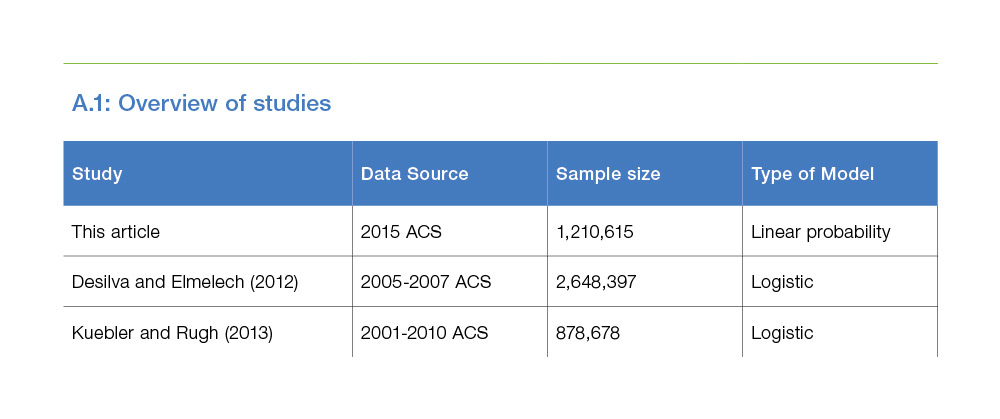

The discussion above of the Hispanic homeownership gap and its likely future trajectory is based on a regression analysis11 of household-level data from the 2015 American Community Survey (ACS) published by the Census Bureau.12 This approach to modeling homeownership rates is well-established in the academic literature,13 and our results are generally consistent with previous research14.

Our analysis assumes that the characteristics influencing homeownership—characteristics like age, marital status, income, and education—have the same marginal impact on the likelihood of homeownership for all people. However, the model allows for an additional impact of race/ ethnicity. As an example, a non-Hispanic White and a Hispanic of Mexican origin with identical background characteristics nonetheless have a different probability of homeownership. To capture these differences, the model includes separate constants for three non-Hispanic groups (White, African-American, and Asian) and four Hispanic groups (Hispanics of Mexican, Puerto Rican, Cuban, and other origins). In addition, there are separate variables to capture immigration-specific effects, such as limited English proficiency.

Comparison to previous studies

Table A.1 compares our study with two previous studies that focus on Hispanic homeownership and A.2 presents the results of our regression.15

Unexplained component of homeownership gaps

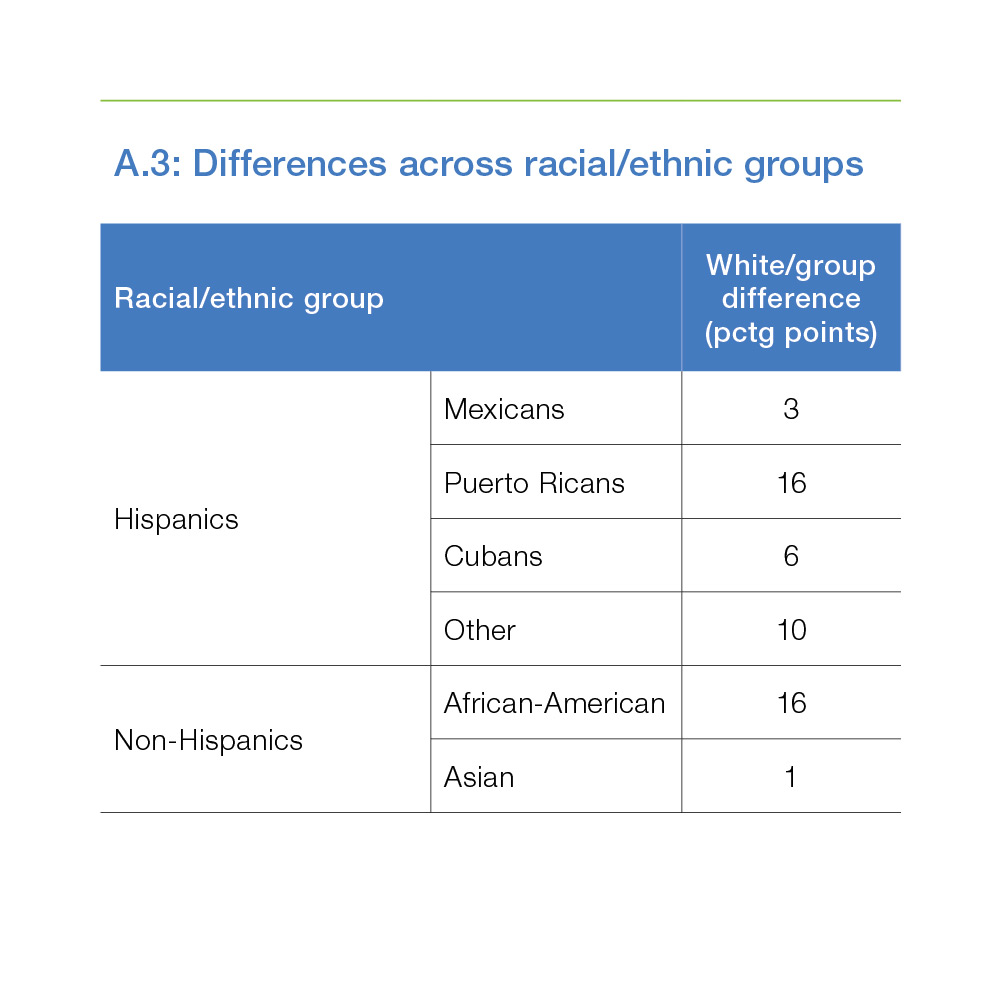

In our model, the constant terms for each racial/ethnic group quantify the portions of the differences in homeownership rates that cannot be explained by fundamental characteristics, such as age and income, as of 2015. Table A.3 displays these unexplained components measured as differences from the baseline group, Whites.

The White/Mexican-origin Hispanic homeownership gap is 23 percentage points. As Table A.3 shows, 3 percentage points (13 percent) of this gap is unexplained by fundamental characteristics. The ethnic-specific homeownership gap for Hispanics of Cuban origin is 6 percentage points (16 percent). Puerto Ricans have a 16-percentage-point ethnic-specific homeownership gap, equal to the White/African-American gap.

Projecting future homeownership rates

To project homeownership rates we hold demographic-specific homeownership and headship rates constant and used the Census-projected population growth by age to reweight the population. This approach links homeownership rates with the share of foreign-born population and is an extension of the methodology we used last year in Why are the Experts Pessimistic About the Future of Homeownership?.

The share of the foreign-born in the population is an important factor explaining homeownership. Census population projections include projections of the share of foreign-born and native-born by age and race/ethnicity. We apply the share of foreign-born projections from Census to our 2015 ACS estimates of the U.S. population to obtain projected homeownership rates.

For the resident Hispanics scenario, we subtracted the Census projections of net immigration for Hispanics from the foreign-born Hispanic population in the baseline. Adjusting the age and share of foreign-born by year (but keeping other factors like education, income and geographic location fixed) provides a measure of the impact of net migration in maintaining the White/Mexican-origin Hispanic age gap and in replenishing the immigration-specific factors that tend to reduce the homeownership rate.16

Holding income, education, and other factors that contribute to homeownership constant is an important limitation of our analysis and most likely reduces our projections of Hispanic homeownership. If the current gap in education and income narrow, the Hispanic homeownership rate is likely to be higher than our projections.

Trends in homeownership

Because our regression model uses data from a single year (2015), it cannot capture historical trends in the racial/ethnic-specific component of the homeownership rate. It's possible that these components will decrease over time. The Census projects an increase in the share of Hispanics in the U.S. population, from 18 percent today to 20 percent in 2025 and 23 percent in 2035. This projected increase may motivate some participants in the housing industry to increase their focus on selling homes and providing mortgages to Hispanics, thus narrowing the White/Hispanic homeownership gap faster than our age-based projections suggest.

References

Borjas, G. J. 2002. Homeownership in the Immigrant Population. Research Institute for Housing America, Institute Report 02-01

Cortes, A., Herbert, C. E., Wilson, E., & Clay, E. (2007). Factors affecting Hispanic homeownership: A review of the literature. Cityscape, 53-91.

DeSilva, S., & Elmelech, Y. (2012). Housing inequality in the United States: Explaining the white- minority disparities in homeownership. Housing Studies, 27(1), 1-26.

Gabriel, S. A., & Rosenthal, S. S. (2005). Homeownership in the 1980s and 1990s: aggregate trends and racial gaps. Journal of Urban Economics, 57(1), 101-127.

Haurin, D. R. & Rosenthal S. S. (2006). Language, Agglomeration, and Hispanic Homeownership. Washington, DC: U.S. Department of Housing and Urban Development, Office of Policy Development and Research

Krivo, L. J., & Kaufman, R. L. (2004). Housing and wealth inequality: Racial-ethnic differences in home equity in the United States. Demography, 41(3), 585-605.

Kuebler, M., & Rugh, J. S. (2013). New evidence on racial and ethnic disparities in homeownership in the United States from 2001 to 2010. SocialScience Research, 42(5), 1357-1374

Painter, G., Gabriel, S., & Myers, D. (2001). Race, immigrant status, and housing tenure choice. Journal of Urban Economics, 49(1), 150-167.

Ruggles S., Genadek, K., Goeken, R., Grover, J., & Sobek M. (2015). Integrated Public Use Microdata Series: Version 6.0 [dataset]. Minneapolis: University of Minnesota.

1 In the D.C. area, the largest immigrant population is from El Salvador.

2 This power immediately grants these Cuban immigrants full legal status and puts them on a path to U.S. citizenship.

3 To quantify these impacts, we estimated a regression relating the probability of homeownership to factors shown in previous research to influence homeownership rates. We then applied Oaxaca-Blinder decomposition technique to determine the impacts. Details of the regression analysis and a comparison to prior research by others appear in the appendix to this article.

4 The homeownership gap between Whites and Hispanics of Mexican origin is 23-percentage points.

5 The appendix details the differences across sub-groups.

6 See "Why are the Experts Pessimistic about the Future of Homeownership?" for an explanation of the relationship between age and homeownership.

7 This unexplained portion of the gap may be due to a combination of factors: limitations of our regression model, unmeasured characteristics such as unfamiliarity with the U.S. mortgage finance system, limited credit records, disparity in financial wealth across groups, and discrimination in housing markets.

8 Census does not publish projections by Hispanic subgroups therefore in rest of our analysis we use the overall Hispanic population. Even in case of overall Hispanic population, age is the most important factor contributing to Hispanic/White homeownership gap followed by immigration attributes so switching to Hispanics does not have any impact on the ensuing analysis.

9 The Census projections begin with an estimated base population for each group. The components of population change—fertility, mortality, and net migration—are projected separately for each birth cohort (that is, persons born in each year) based on past trends.

10 Foreign-born is one of the immigration-specific characteristics that is correlated with a lower homeownership rate.

11 For this article, we employ a linear probability model rather than the more-commonly-used logistic model. Both estimators are consistent, but the use of a linear probability model simplifies the attribution of impacts to regressors and makes the projection of future homeownership rates more tractable.

12 We obtained ACS data from the Integrated Public Use Micro Data Series (IPUMS) which are compiled from the American Community Survey (Ruggles et al. 2015).

13 See, for example, Painter et al. 2001; Borjas 2002; Krivo and Kaufman 2004; Gabriel and Rosenthal 2005; Haurin and Rosenthal 2006; Cortes et al. 2007. Desilva and Elmelech 2012 and Kuebler and Rugh 2013 focus specifically on the homeownership gaps of Hispanic groups.

14 Like most previous studies we are constrained by unavailability of the measure of wealth that can influence homeownership. However, we use income and education in our analysis and that should partially capture the effect of wealth.

15 These estimated marginal impacts are largely consistent with the direction and magnitudes found in earlier studies.

16 Ideally, we also would adjust the other factors as well to represent their prevalence in the resident population. These adjustments would likely increase the Mexican -origin Hispanics homeownership rate further.

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP

Sean Becketti, Chief Economist

Ajita Atreya, Quantitative Analyst Sr.