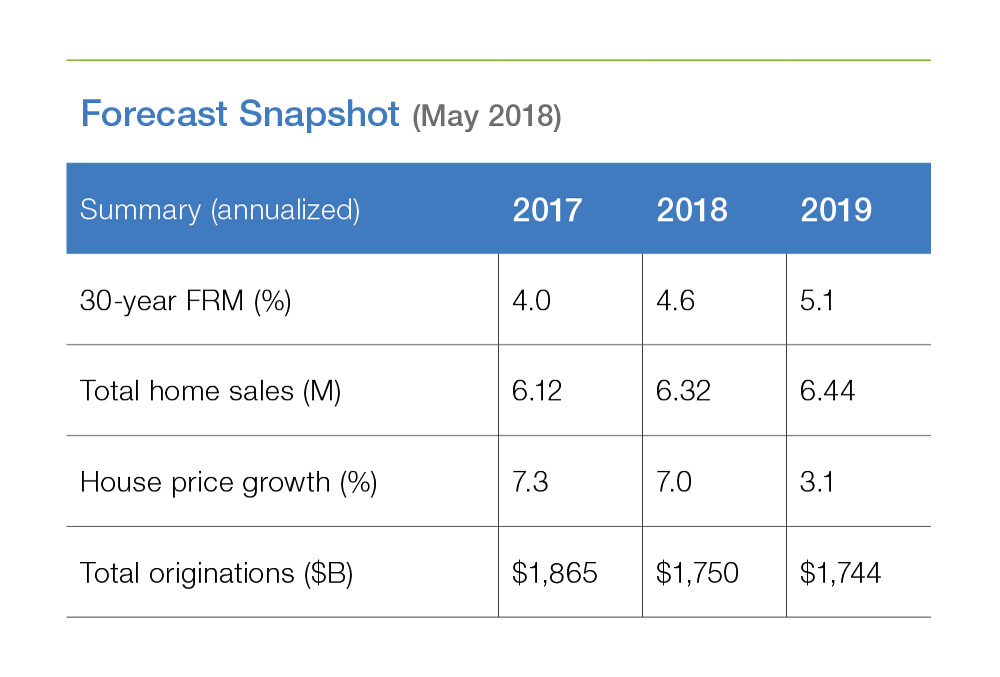

Housing Demand Holding Steady Amidst Rising Mortgage and Home Prices

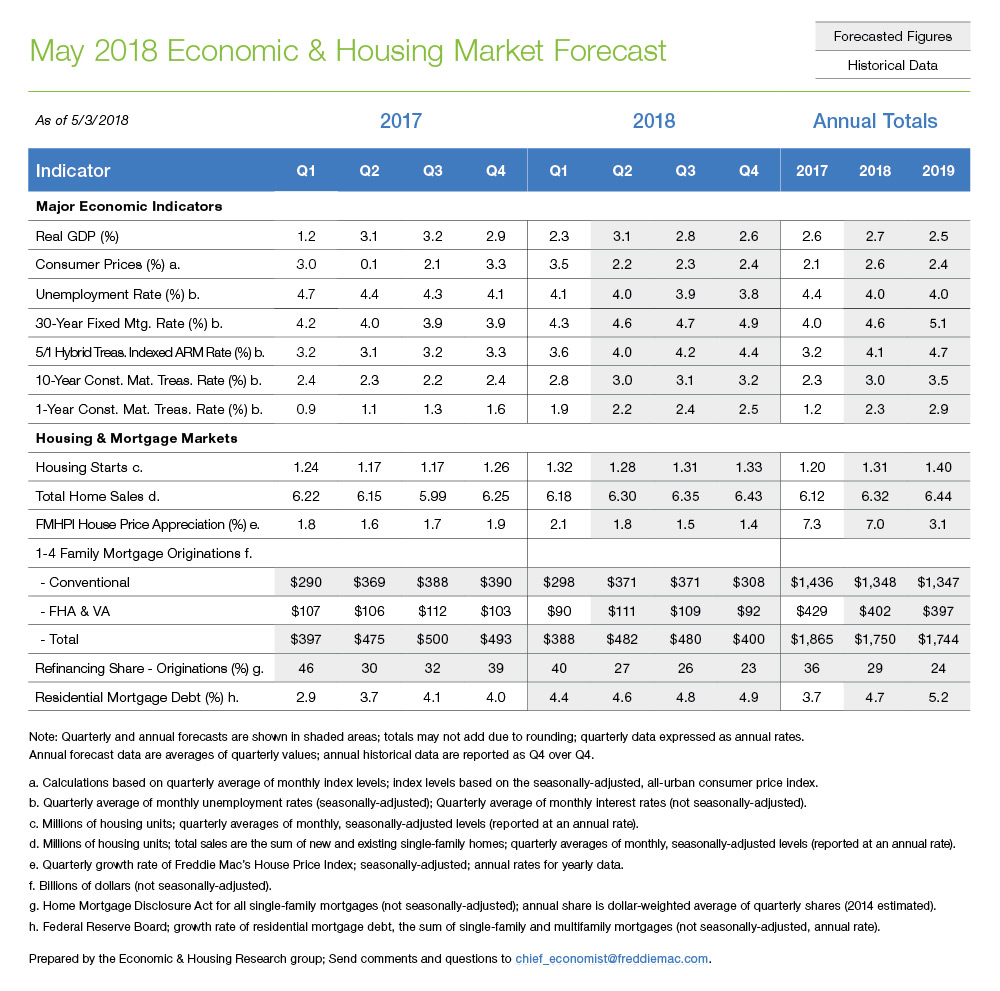

Real Gross Domestic Product (GDP) grew at an annualized rate of 2.3 percent in the first quarter of 2018, down from 2.9 percent in the fourth quarter of 2017. First quarter expansion tailed off as consumer spending growth was the lowest in nearly 5 years. We still expect spending to pick up in coming quarters as the fiscal stimulus from tax cuts further kicks in. We forecast real GDP growth of 3.1 percent in the second quarter of 2018 and 2.7 percent for the full year.

The U.S. labor market keeps chugging along, generating many new jobs. The economy has added jobs for 91 consecutive months through April 2018, helping to push the unemployment rate to 3.9 percent last month, the lowest level since 2000. However, wage gains remain elusive. Average hourly earnings increased 2.6 percent year-over- year last month. Hourly earnings growth is only a hair above the rate of inflation (2.5 percent year-over-year increase, according to the April Consumer Price Index). We forecast consumer price inflation of 2.7 percent in 2018 and 2.5 percent in 2019.

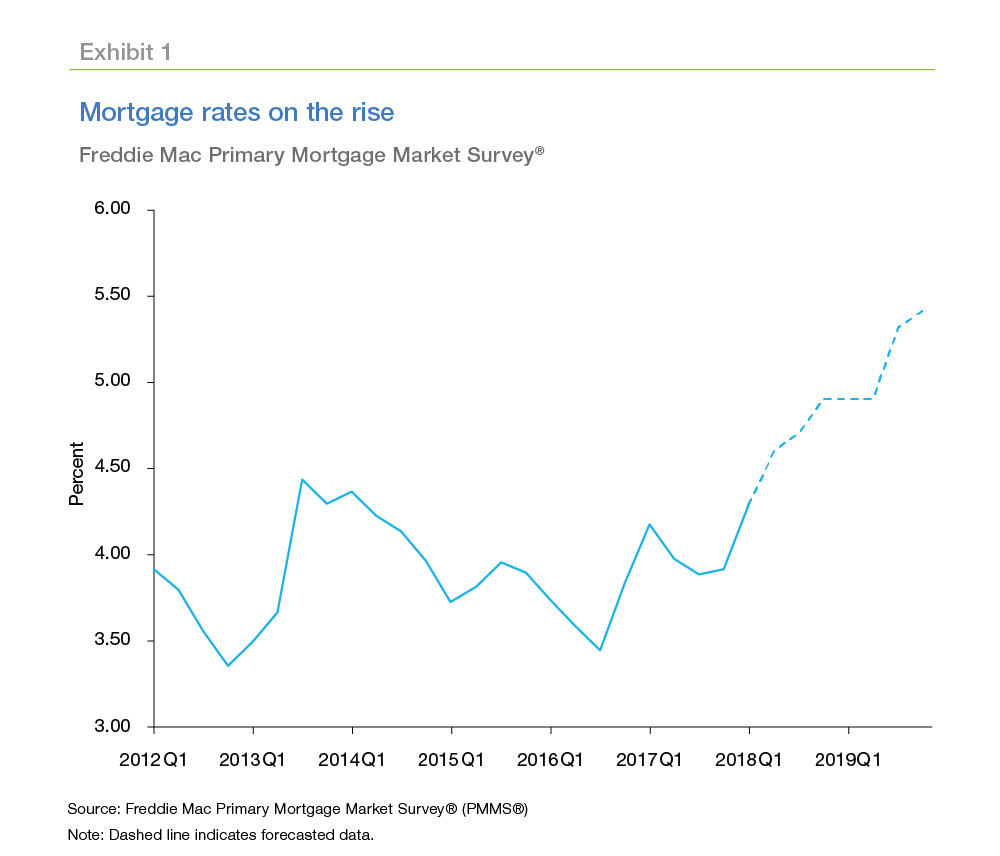

Mortgage rates on the rise

Firming inflation will put upward pressure on interest rates, including mortgage rates. The 30-year fixed-rate mortgage kept climbing in May, up to 4.66 percent by the middle of the month. We expect the uptick in rates to continue. Our forecast has mortgage rates averaging 4.9 and 5.4 percent in the fourth quarter of 2018 and 2019, respectively.

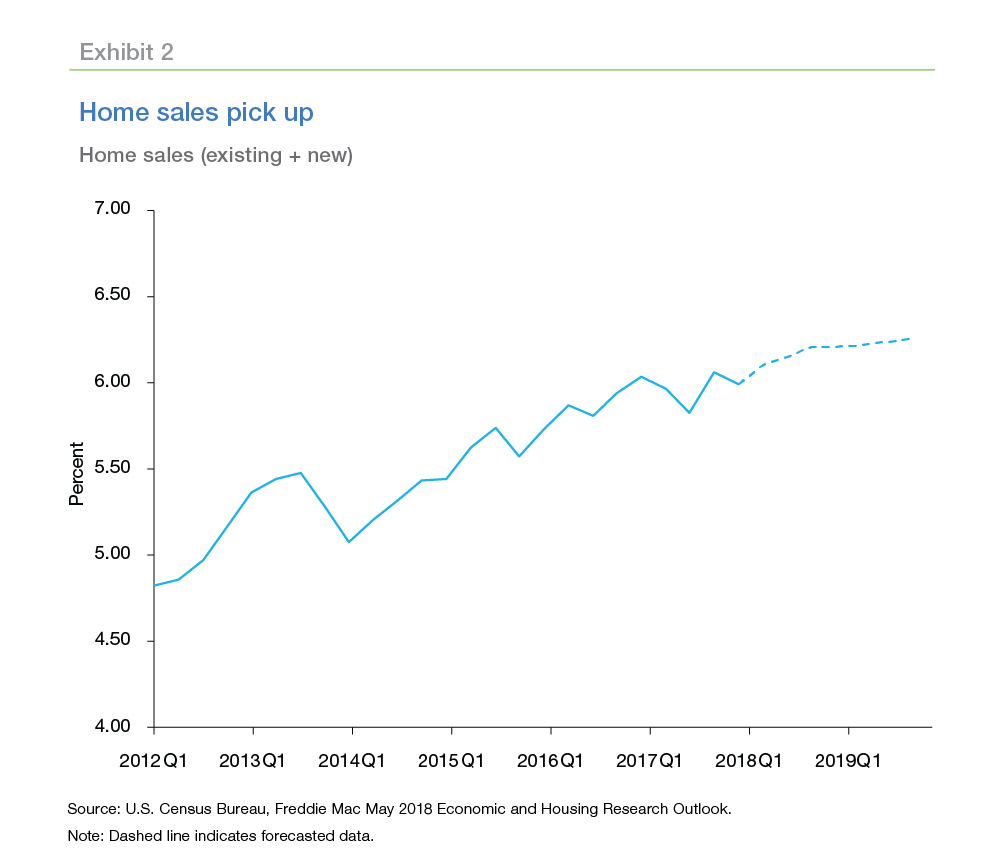

Housing demand holds up

Higher mortgage rates have not yet slowed home purchase demand. Buyer resiliency in the face of higher rates reflects the healthy economy and strong consumer confidence. We forecast modest growth in home sales over the next two years. Total home sales (new and existing) are forecasted to increase to 6.32 million (+3 percent year-over-year) this year and to 6.44 million (+2 percent year-over-year) in 2019.

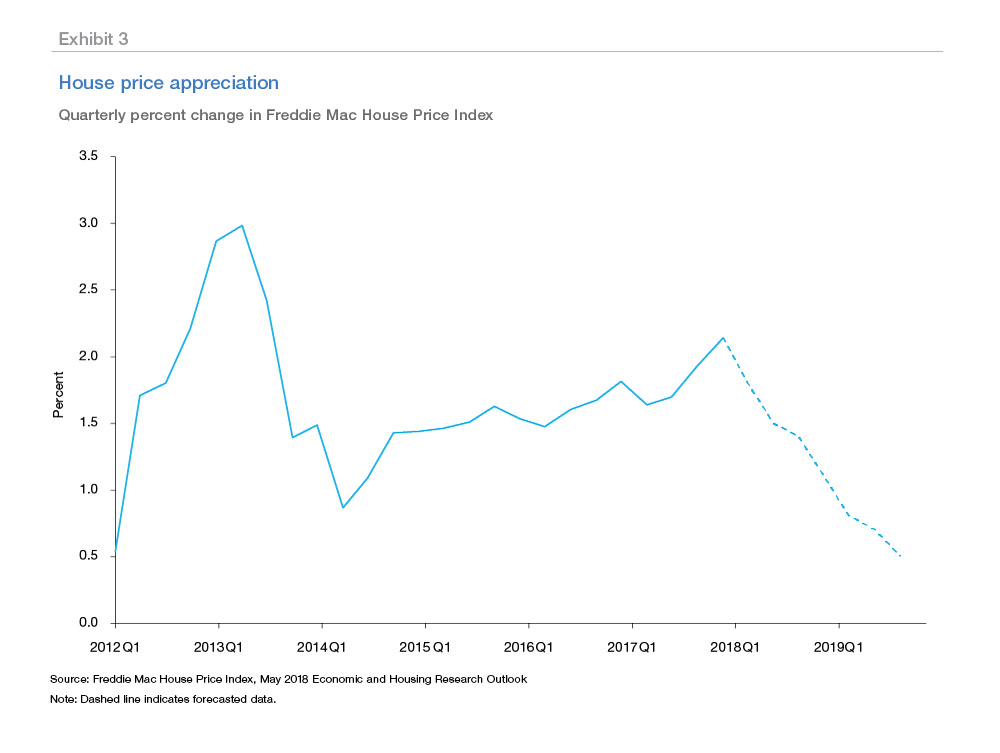

Robust housing demand and limited supply continue to put upward pressure on house prices. Nationally, home prices are increasing at around a seven percent annual rate. With higher mortgage rates tempering demand, and new supply gradually coming online, home price growth should moderate. We forecast home prices to increase 7.0 percent in 2018, with the annual growth moderating to 3.1 percent in 2019.

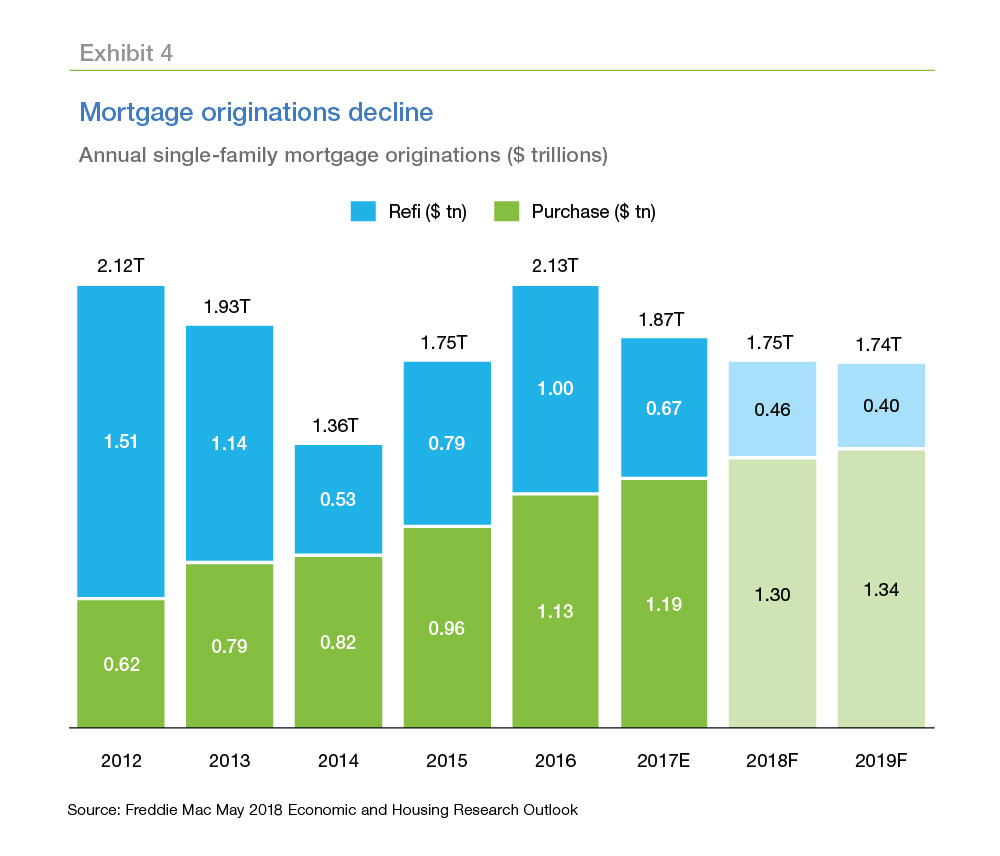

Mortgage originations decline

Higher borrowing costs reduce homebuyer affordability and the incentive to refinance. However, the strong labor market and years of pent-up buyer interest are providing a lift to purchase demand. In 2018, the negative impact of higher mortgage rates on refinance activity will outweigh the positive factors lifting originations.

Refinance activity, which already declined $300 billion (32 percent) from 2016 to 2017, is forecasted to decline another $175 billion (26 percent) in 2018. Higher home sales and house price appreciation will drive purchase origination volume up $60 billion (up 5 percent), but not enough to offset the decline in refinances. Full year originations are forecasted to fall about 6 percent in 2018 to $1.75 trillion and stabilize at $1.74 trillion in 2019.

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP