Freddie Mac's Mortgage Rate Survey Explained

Freddie Mac’s Primary Mortgage Market Survey (PMMS) is the longest running weekly survey of mortgage interest rates in the United States. Since Freddie Mac launched its survey in 1971, others have begun collecting and reporting mortgage rate information.

For example, Bankrate and Zillow report weekly average 30-year fixed-rate mortgage rates, and the Federal Housing Finance Agency provides a Monthly Interest Rate Survey (MIRS), which includes annual mortgage interest rate data back to 1963. The various survey measures usually show the same general trend in mortgage rates, but there are differences from week to week, and in some cases, persistent differences in the level of rates reported by various sources.

Because the PMMS is widely covered across the industry and in the media, various stakeholders, as well as consumers, are often interested in understanding why the PMMS rates sometimes differ from other surveys, other reports, or the rates their lender is quoting on the day Freddie Mac releases its survey. Freddie Mac is also interested in understanding why various measures of mortgage rates can differ and ensuring that it maintains the accuracy and reliability of the PMMS.

This Research Note considers differences in the PMMS and the Mortgage Bankers Association’s Weekly Applications Survey (WAS), another widely tracked survey for the mortgage market.

Background on mortgage rates

Before getting into the details of the PMMS and WAS, it’s helpful to take a step back and see what makes up the mortgage rates that borrowers pay, especially for the conventional conforming 30-year fixed-rate mortgage, the most popular product in the market today. Most, but not all, conventional conforming 30-year fixed-rate mortgages in the United States end up in a mortgage- backed security. The lenders who originate the mortgage loans and sell them into the secondary market need to cover the costs of origination, servicing, securitization, and funding of the loans, and those costs are passed on to borrowers through the mortgage rate they pay.

Origination and servicing costs contribute about 0.5 percentage points to the cost of a loan. Another 0.5 percentage points come from the cost of securitizing a loan, which includes a guarantee fee and a 0.10 percentage point payroll tax surcharge. The remainder and largest proportion of the mortgage rate comes from funding costs.

Funding costs are determined by market forces in the liquid Mortgage-Backed Securities (MBS) market. Approximately $200 billion in MBS are traded in the market every day. MBS pricing is anchored by Treasury yields, which indicate the cost of borrowing for the least-risky borrower in the market—the U.S. Treasury. Mortgage rates tend to move up or down with Treasury yields.

Enlarge Image

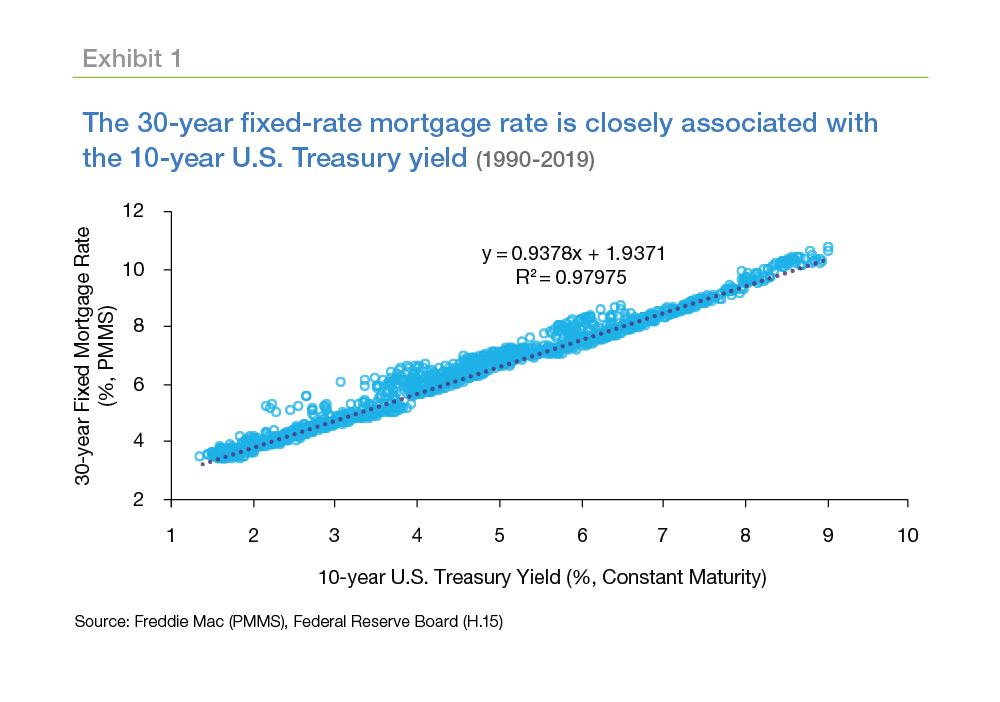

Although there is a positive relationship between the 10-year Treasury yield and the 30-year fixed-rate mortgage rate, these rates do not move in lockstep every week. As a result, the mortgage-Treasury spread, that is, the arithmetic difference in these rates, is not constant. These rates can vary based on shifts in investor opinions on the riskiness of mortgages, imbalances in the supply of Treasuries and mortgages, and fluctuations in our survey results, among other things.1During episodes of market turbulence, such as the 2008 financial crisis, the mortgage-Treasury spread can increase significantly. But, once the turbulence subsides, the spread tends to narrow, and the close correlation between the Treasury yield and mortgage rates returns. As shown in Exhibit 1, 98% of the weekly variation in average 30-year fixed-rate mortgage rates since 1990 can be explained by weekly variations in 10-year Treasury yields.

Background on Freddie Mac’s Primary Mortgage Market Survey

The Freddie Mac PMMS is a primary market survey, which means it does not use data on loans purchased or funded by Freddie Mac. Instead, Freddie Mac surveys originators across the country and across different types of lending institutions and estimates what a typical consumer might see if they shopped around for mortgage rates. The PMMS sample includes a mix of lender types which is roughly proportional to the level of mortgage business that each type commands nationwide.

The PMMS currently provides only a national average. Freddie Mac previously reported regional averages because historically there were often substantial differences in the rates borrowers paid based on the region where they lived. Over time, regional averages converged as the liquid MBS market allowed borrowers all over the country to access the benefits of the global capital markets when shopping for a mortgage. Because of the convergence in regional average mortgage rates, Freddie Mac stopped reporting the regional averages in 2015.

The PMMS is focused on conventional, conforming fully-amortizing home purchase loans for borrowers who put 20% down and have excellent credit. From week to week, the composition of borrowers in the market changes, but the PMMS keeps the loan product, loan purpose, and borrower profile constant. By keeping the loan profile constant, the PMMS captures weekly movements in rates excluding composition effects, which allows for easier comparison over time. For example, in periods when mortgage rates decline, the share of refinance loans typically rises. If on average, refinance loans have higher mortgage rates than otherwise similar purchase loans, then the decline in the national average rate would be somewhat offset by a shift toward more refinance loans.

The PMMS also calculates “points” by adding discount points and origination points. A point equals one percent of the loan amount. Discount points are used by consumers to buy down their mortgage interest rate. Therefore, an inverse relationship exists between the number of points paid and the given mortgage rate. Origination points are paid by consumers but are used to cover the costs of originating the mortgage, such as compensation for the loan officer, application processing costs, etc. The points quoted in the PMMS represent the average points charged for mortgages offered at the PMMS rate during the survey week, and they have historically averaged around one point.

The survey is collected from Monday through Wednesday, and the results are released on Thursday at 10 a.m. Eastern Time (ET).

Background on the Mortgage Bankers Association’s Weekly Applications Survey

The MBA WAS measures single-family loan application activity. It surveys lending institutions to gauge changes in application activity from week to week. Per the MBA, as of September 2011, the WAS covers more than 75% of the U.S. retail residential market. As noted above, the survey measures application activity, not origination activity. Not all applications will necessarily be approved, and not all approved applications will result in an origination.

The rates captured in the WAS are the averages of lender reported rates and are not currently weighted to reflect application volumes. Like the PMMS, the WAS reports on points and fees, which include discount points paid by the borrower and origination fees charged by the lender.

The MBA reports survey results every Wednesday morning at 7 a.m. ET. Results reported Wednesday morning are for the period beginning the previous Saturday at midnight through 11:59 p.m. that Friday.

Differences between the PMMS and WAS

Enlarge Image

Enlarge Image

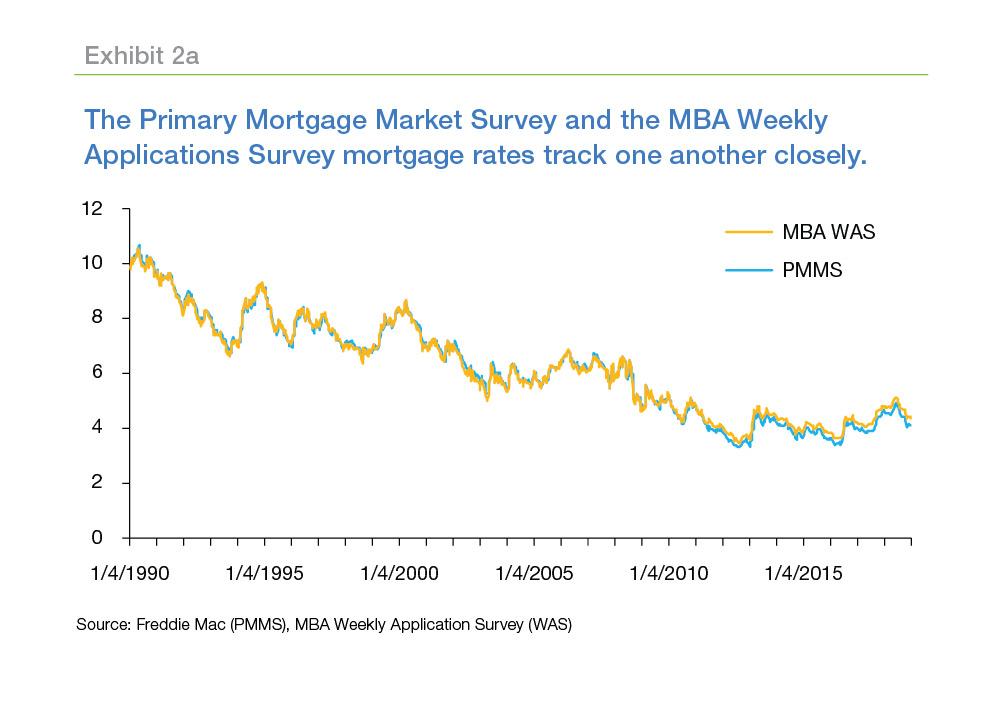

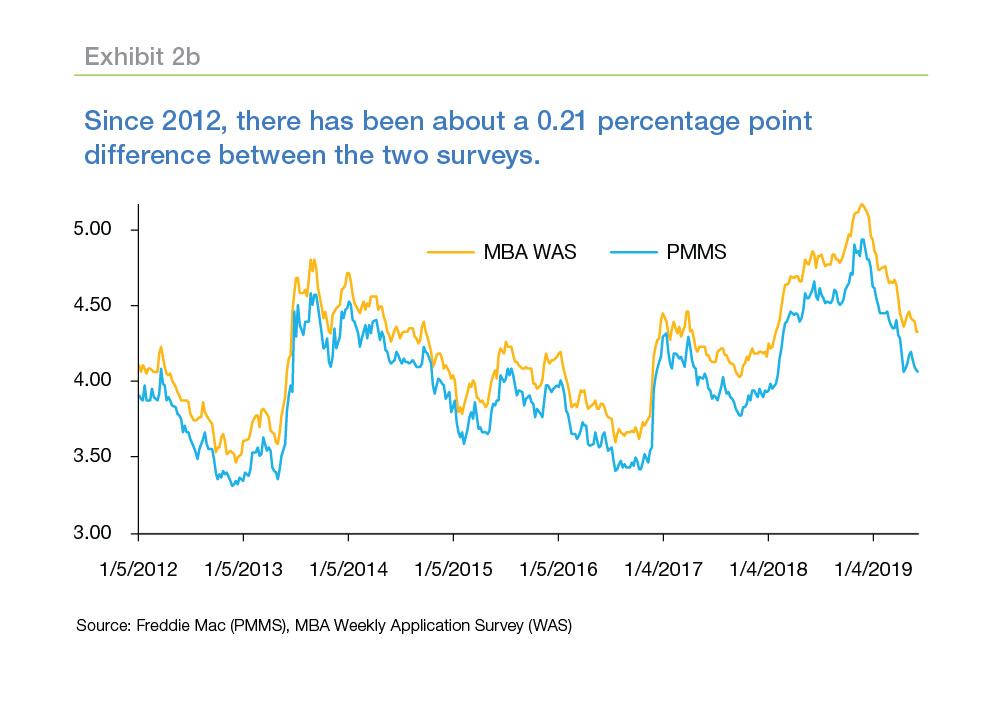

In general, the PMMS and WAS mortgage rates track each other closely. As shown in Exhibit 2, the national mortgage rates reported in the two surveys since 1990 have had a correlation of 0.997. Despite the high correlation, the average rates reported in the two surveys have differed, and the level of divergence has increased in recent years. For example, since 1990, the average difference in rates reported in the two surveys is 0.035 percentage points, and the average difference since 2012 is 0.21 percentage points.

What can explain this divergence?

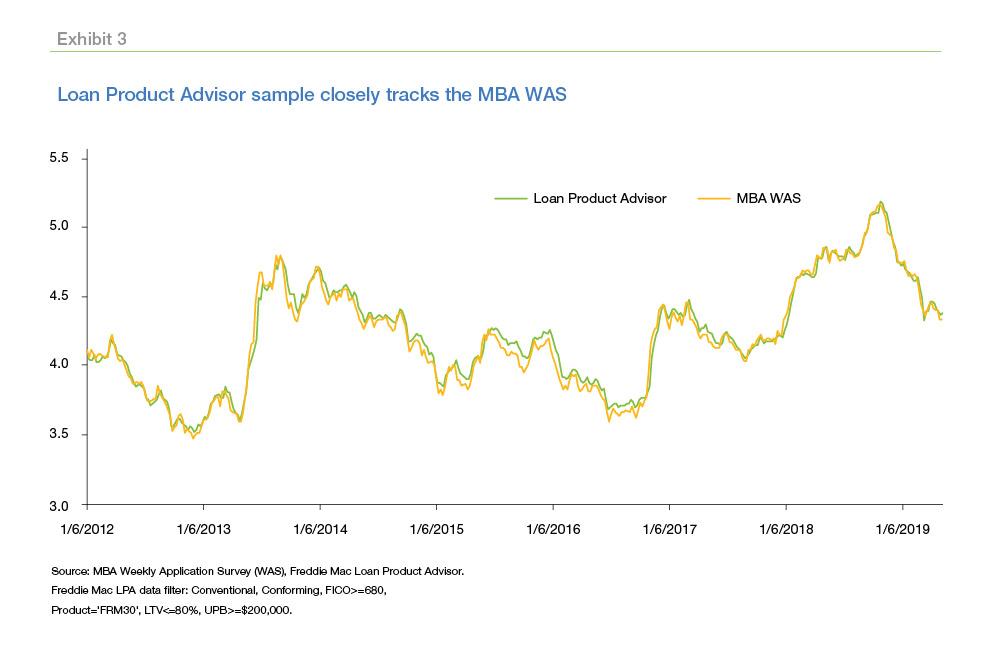

To analyze the difference between the PMMS and WAS rates, Freddie Mac ran a variety of scenarios using data collected through its Loan Product Advisor underwriting system to replicate a sample of loans similar to the applications tracked in the WAS and constructed a close approximation of the MBA’s average rate. As shown in Exhibit 3, when the sample of applications received through Loan Product Advisor was restricted to 30-year fixed-rate conventional applications, with a loan-to-value (LTV) of less than or equal to 80% and an unpaid principal balance (UPB) greater than or equal to $200,000 in the conforming space, the Loan Product Advisor and WAS rates were almost identical.

Enlarge Image

Therefore, understanding the difference between the Loan Product Advisor sample and the PMMS data helps explain why the PMMS and WAS have diverged.

The Loan Product Advisor sample summarized in Exhibit 3, which more closely tracks the WAS in terms of average rates, is less restricted than the loans we survey in the PMMS. When we added restrictions with respect to loan purpose and credit score, the Loan Product Advisor sample more closely matched the PMMS sample. Specifically, the Loan Product Advisor sample was restricted to applications with the following features:

- Home purchase loans

- FICO scores of 790 or above

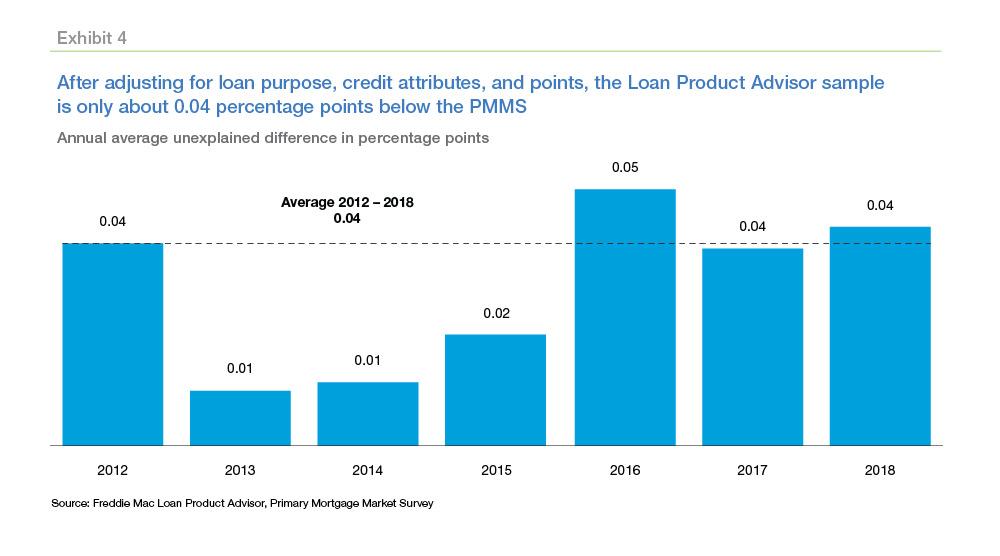

The Loan Product Advisor sample also does not include discount points paid by borrowers, unlike the PMMS data. As a result, the Loan Product Advisor sample was adjusted to add a measure of discount points to better match the points in the PMMS data. Given the trend in average rates shown in Exhibit 3, it's assumed that the weekly average points for applications received through Loan Product Advisor is equal to those reported in WAS. The contract rate for the Loan Product Advisor sample was then adjusted based on the differential in reported points between the PMMS and WAS data. After adjusting for loan purpose, credit score, and points, the differential in weekly average rates between the Loan Product Advisor sample and the PMMS data is reduced to about 0.04 percentage points on average for the 2012-2018 period, or about 20% of the original gap observed.

Exhibit 4 displays the differences in the PMMS data and our adjusted Loan Product Advisor sample.

Enlarge Image

The remaining difference between the PMMS and WAS data remains unexplained but is likely due to sampling variability, differences in coverage including timing, and differential weights on lenders.

For example, with respect to sampling variability, Freddie Mac’s internal analysis suggests that the weekly PMMS has a margin of error of about 0.05% for the 30-year fixed-rate mortgage. With respect to coverage and timing, the PMMS is constructed to reflect originations, while the WAS measures applications, only about 75% of which are covered by the survey and not all of which will become originations (during the same survey period or at all). With respect to weighting, the PMMS is constructed to reflect a composition of mortgage originations weighted in terms of the size and type of lending institution as well as geographic coverage while the WAS is not weighted to reflect application volumes.

These differences in approach between the PMMS and WAS help explain some of the remaining differences in the survey data.

References

1. For a detailed technical analysis, see Boyarchenko, N., Fuster, A., & Lucca, D. O. (2018), Understanding mortgage spreads, FRB of New York Staff Report, (674), available at https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr674.pdf.