Mortgage Forbearance Rates during the COVID-19 Crisis

Bob and Jane purchased their home three years ago. Now, in the midst of the pandemic, Jane is furloughed from her job as a purchasing manager, and Bob is working fewer hours as a mechanic. They are wondering how long their savings will last. Postponing mortgage payments would make their reserves hold out a lot longer.

During the COVID-19 crisis, mortgage forbearance plans have played an important role in helping households manage their finances by providing short-term liquidity to mortgage borrowers. Mortgage forbearance temporarily removes the obligation for borrowers to make their monthly mortgage payment.1 This Insight contrasts the characteristics of those mortgages in forbearance across the current COVID-19 crisis and two earlier periods: the 2017 Storms period (in declared disaster areas in the aftermath of hurricanes and tropical storms in 2017, including Hurricanes Harvey, Irma, and Maria); and the Baseline period (January 2019 to February 2020) just before the current crisis. We find that forbearance rates during the COVID-19 period are similar to those during the 2017 Storms but are much higher than rates during the Baseline period.

Forbearance plans are typically used by borrowers who experienced a temporary hardship such as a sudden loss of employment, a reduction in income, or a natural disaster. Homeowners typically have more savings than an average household helping them to overcome short-term declines in income or unexpected expenses. However, about 30% of homeowners have less than $14,000 in financial assets with which to cover a sudden loss of income.2 By reducing a household’s immediate mortgage expenses during a crisis, forbearance helps preserve homeownership.3

The COVID-19 pandemic has led to unprecedented levels of mortgage forbearance. On March 18, 2020, Freddie Mac extended broad mortgage relief to borrowers unable to make their mortgage payments because of COVID-19, regardless of whether or not they have contracted the virus. Included among these relief options were forbearance plans that could provide borrowers with payment relief for up to 12 months, while suspending borrower late charges and penalties. This was followed by the CARES Act, signed into law on March 27, 2020, which provided borrowers with federally backed mortgages an option to request mortgage forbearance for up to 180 days.4 Mortgage forbearance reached a peak in May 2020, with more than 4 million U.S. mortgages in forbearance, which represents about 8% of outstanding mortgages and $1 trillion in mortgage debt.5 Overall, through forbearance, homeowners have delayed about $4 billion in mortgage payments each month.

Understanding the incidence of mortgage forbearance is important for many mortgage market participants, including policy makers, originators, servicers, and investors. In the current crisis, policy makers are interested in the impact of forbearance programs on preserving homeownership, the distribution of benefits from mortgage forbearance, and the total level of implicit stimulus to the economy. Mortgage originators are affected by those borrowers that enter forbearance soon after the loan has been originated but before the loans are sold or delivered into securities. These loans may incur additional delivery fees or may not be accepted for purchase or securitization. Mortgage servicers are affected by forbearance through their obligation to advance payments to bondholders and by the costs associated with negotiating repayment plans, loan modifications, or short sales.

Investors in mortgage securities may find that security cash flows are affected by forbearances. While Freddie Mac loans in forbearance will remain in their mortgage securities, once the forbearance period ends, the nature of these post-forbearance outcomes will influence the timing of principal repayments. Forbearance outcomes can also affect investors in Freddie Mac’s credit risk transfers (CRT) transactions though the exact impacts differ across CRT issuances.6

Analysis and data

We examine the drivers of mortgage forbearance in Freddie Mac loans over three distinct episodes: the beginning of the COVID-19 crisis period (March to August 2020); another period of high rates of forbearance in areas struck by natural disasters in 2017 (a Storms period including Hurricanes Harvey, Irma, and Maria, and tropical storms, covering August to December 2017); and a Baseline period capturing the 14 months before the COVID-19 crisis (January 2019 to February 2020).

Our primary data source is internal loan-level servicing information for Freddie Mac mortgages. We restrict our analysis to 30-year fixed-rate mortgages that were current and not in forbearance the month before the start of the observation period. For the 2017 Storms period, we consider the forbearance rate only among those loans eligible for disaster-related forbearance programs. In each of these samples, we track whether a loan enters a new forbearance plan during the observation period.7

We compare the rates at which loans enter forbearance in the different periods by borrower and loan characteristics. The characteristics are current or marked-to-market loan-to-value ratio (LTV); credit score (FICO); the debt-to-income ratio (DTI); and the monthly payment. The characteristics used in the analysis are as of the time the loan was originated, except for the LTV ratio, which is as of the month before the start of the observation period. The current LTV ratio is defined as the ratio of the current unpaid mortgage balance divided by the current home value. The current home value is calculated using Freddie Mac’s House Price Index (FMHPI) at the ZIP-Code level and the home price at origination.

Results

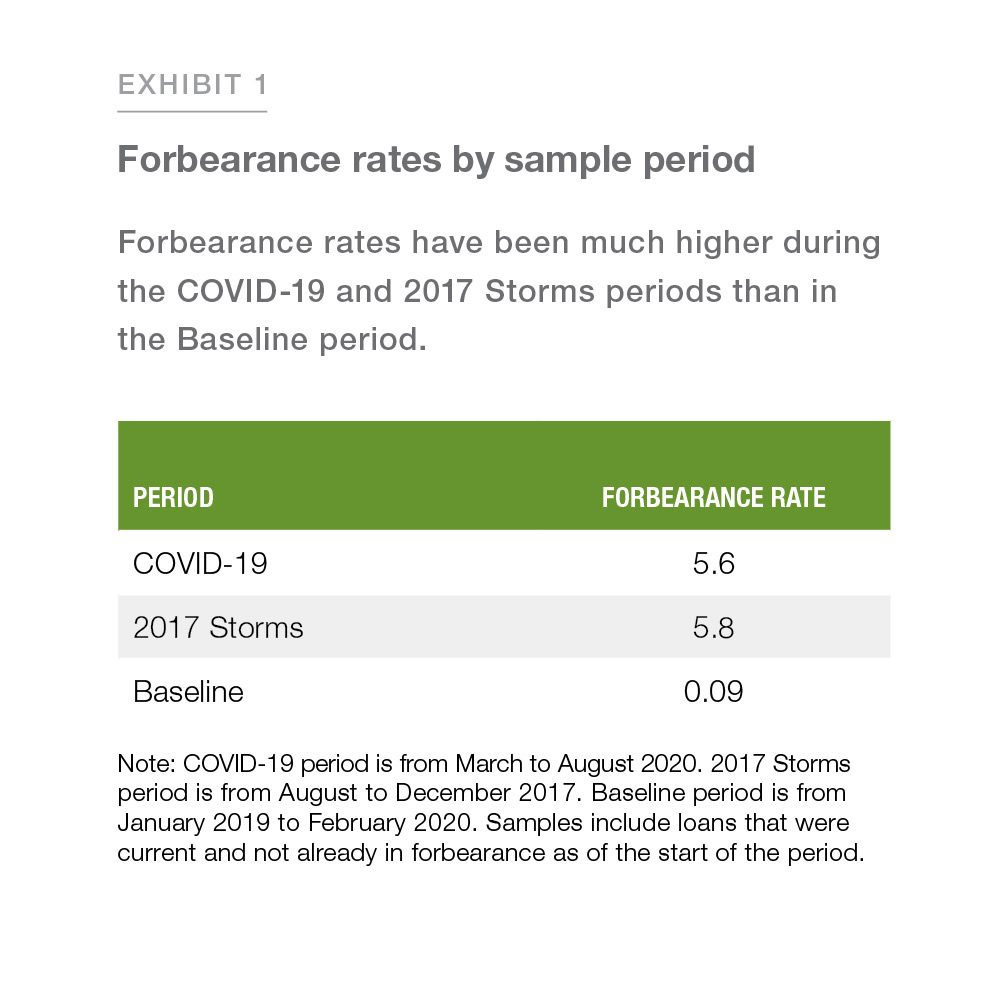

We observe three basic facts about forbearance rates across these periods. First, forbearance rates in the COVID-19 crisis period are similar to those seen in the 2017 Storms period, but much higher than in the Baseline period.8 Second, several characteristics associated with higher default rates are also associated with higher forbearance rates, such as high LTV ratios, low credit scores, and high DTI ratios. Third, forbearance rates are lowest for loans with low monthly payments, for which forbearance offers limited liquidity relief. With respect to the level of forbearance rates across the three sample periods, Exhibit 1 shows that the rates were 5.6% in the COVID-19 period, nearly the same as in the 2017 Storms (5.8%), but almost 60 times higher than in the Baseline period (0.09%), even though the Baseline spans a longer time horizon.9

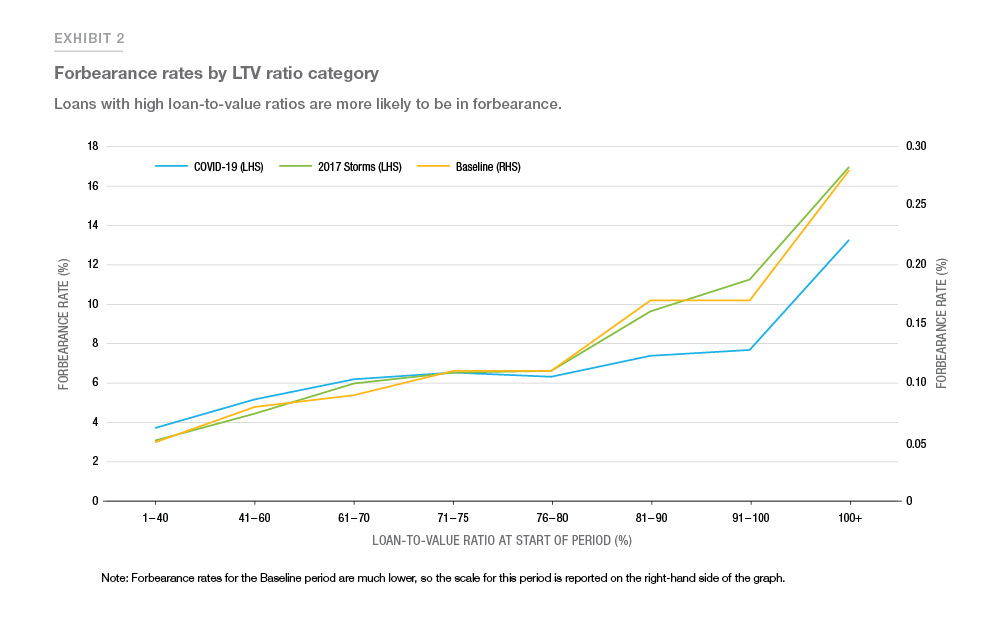

With respect to loan characteristics, Exhibit 2 shows how forbearance rates increase with increasing LTV ratios in all three samples, but less steeply in the COVID-19 period. In the COVID-19 period, the rate more than triples, going from 3.1% for loans with LTVs in the lowest category (1 to 40 LTV) to 13.3% for the highest category (101+). This rate increases by more than a factor of 5 in the 2017 Storms period (from 3.1% to 17.0%) and Baseline period (from 0.05% to 0.28%).

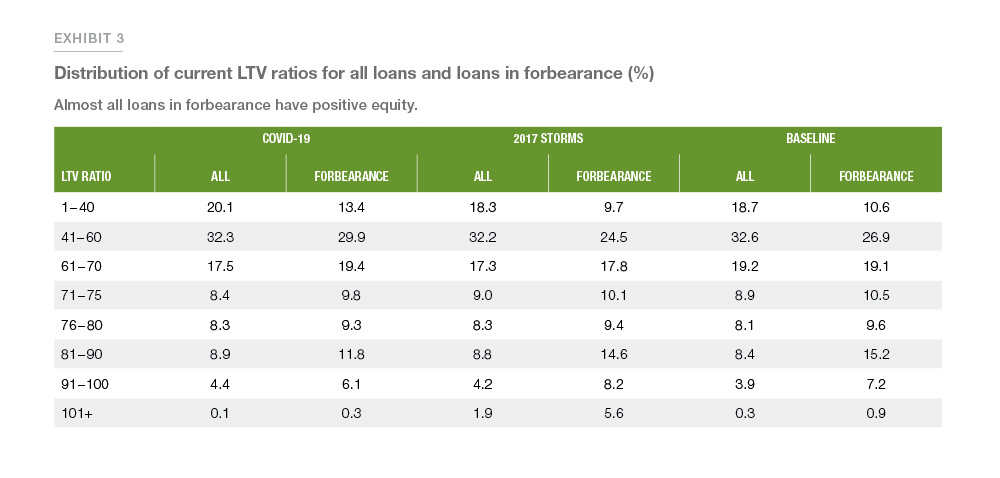

It is also interesting to note how the LTV ratios of loans in forbearance differ from loans in default. Exhibit 3 shows that the distribution of LTV ratios for COVID-19 forbearances are similar to loans in the entire sample. The mortgage default literature describes the impetus for default as a combination of negative equity and an inability to repay (see, for example, Elul et al. 2010). Few borrowers default if their loans have positive equity because they have the option of selling the house and using the proceeds to pay off the loan. In contrast, forbearance largely occurs for households with positive equity that are experiencing a short-term liquidity problem. Among those who enter forbearance during the COVID-19 period, 0.3% of loans have negative equity. This is higher than for the entire sample, where only 0.1% of loans have negative equity, but is still much lower than among seriously delinquent loans.

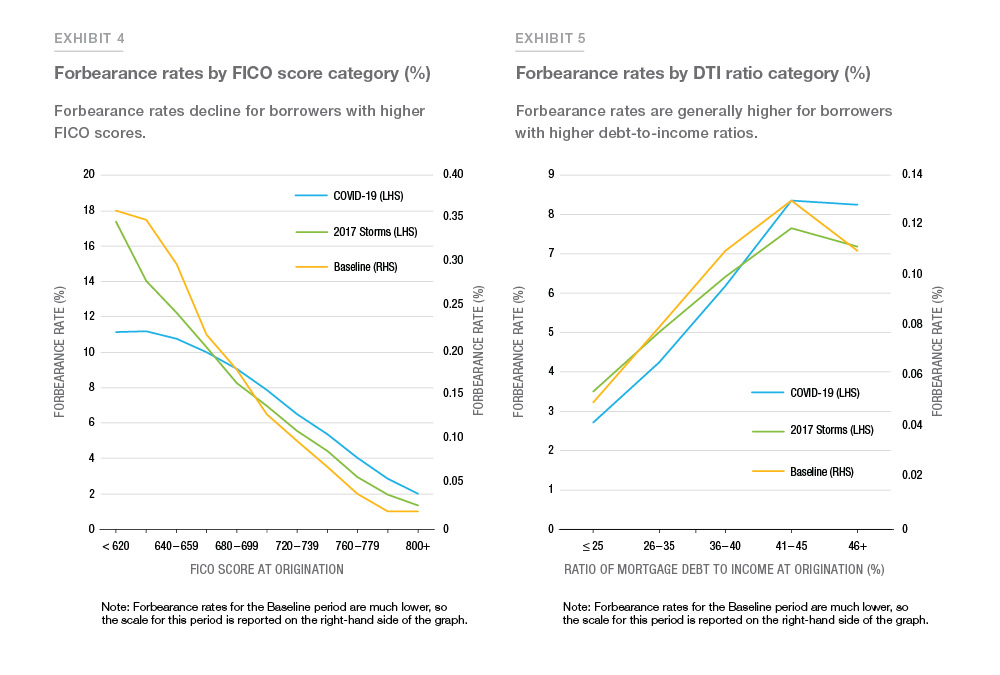

The other main characteristics that have similar relationships to default risk and forbearance risk are borrowers’ FICO scores and DTI ratios. Exhibit 4 shows how forbearance rates decline as borrower’s FICO scores increase across all three periods, but less steeply in the COVID-19 period. In the COVID-19 period, the rate increases by a factor of about 5.6, going from borrowers with FICO scores in the highest category (800+) at 2.0% to the lowest category (<620) at 11.1%.

This rate increases by a factor of 13 in the 2017 Storms period (from 1.3% to 17.4%) and by a factor of 18 in the Baseline period (from 0.02% to 0.36%). For borrowers’ DTI ratios, Exhibit 5 shows how forbearance rates increase as DTI ratios increase in all three periods, but level off above 40%. In the COVID-19 period, the rate increases by a factor of about 3, going from loans with DTI ratios in the lowest category (≤ 25%) at 2.7% to the highest category (46%+) at 8.3%. This rate increases by a factor of 2 in the 2017 Storms period (from 3.5% to 7.2%) and by a factor of 2.2 in the Baseline period (from 0.05% to 0.11%).

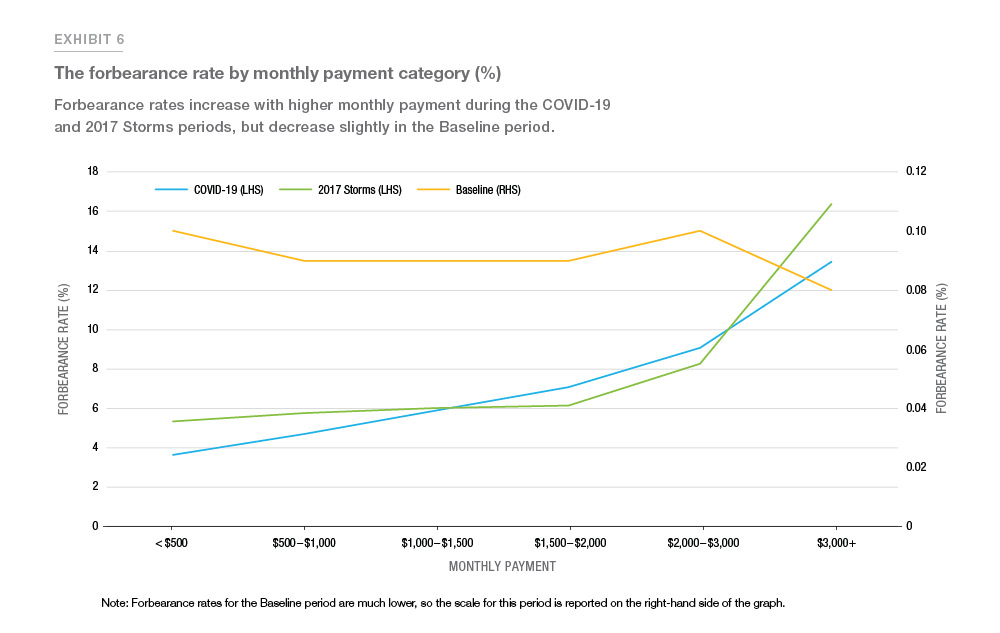

The amount of short-term liquidity that forbearance provides to borrowers is proportionate to their monthly mortgage payment. Exhibit 6 shows the relationship between forbearance rates and monthly payment. In both the COVID-19 and 2017 Storms periods, the rate of forbearance increases with the amount of the monthly mortgage payment, especially for payments exceeding $3,000 per month. In crisis times when liquidity becomes an issue, it makes sense that those with the greatest liquidity gains from forbearance enter it at a higher rate.10

Conclusion

Mortgage forbearance has played an important role in protecting borrowers affected by the COVID-19 pandemic by providing them with liquidity when they need it most. Millions of families have been able to stay in their homes with the financial relief provided through mortgage forbearance. Without forbearance, many of these households would have been forced to sell their homes or would have defaulted on their mortgages, which, in turn, could have depressed the housing market, leading to further defaults in a vicious cycle.

We have examined the variation in forbearance rates in mortgages funded by Freddie Mac across three periods and by several key variables. We have shown that the rate of mortgage forbearance during the COVID-19 crisis is similar to the rate seen in the 2017 Storms period, but much higher than the Baseline sample for the 14 months preceding the COVID-19 crisis. During the COVID-19 crisis and the 2017 Storms, many households likely viewed their situation as a temporary liquidity shortfall and so chose forbearance as their best financial strategy. We have also illustrated the relationship between forbearance rates and important borrower and loan characteristics: FICO score, DTI ratio, LTV ratio and monthly payment.

Forbearance has been an understudied area of research in mortgage finance. The scale and importance of this assistance program in the COVID-19 crisis highlight important new directions for this area of research. For example, what explains the behavior of borrowers who have entered forbearance but have continued to make their mortgage payments? Why do some borrowers who qualify for forbearance choose to default instead? How long will the duration of forbearance be for borrowers in the COVID-19 crisis? Finally, what are the final outcomes from mortgage forbearance? Which loans are most likely to enter into a successful repayment plan, to enter into a loan modification, or to default, and at what levels?

References Agarwal, S., B. W. Ambrose, A. P. Bandyopadhyay, and Y. Yildirim. 2020. “Communications between Borrowers and Servicers: Evidence from the COVID-19 Mortgage Forbearance Program.” Working paper. https://ssrn.com/abstract=3676546or http://dx.doi.org/10.2139/ssrn.3676546 Elul, R., N. S. Souleles, S. Chomsisengphet, D. Glennon, and R. Hunt. 2010. "What 'Triggers' Mortgage Default?" American Economic Review, 100 (2): 490–94. Foote, C. L., K. Gerardi, and P. S. Willen. 2008. “Negative Equity and Foreclosure: Theory and Evidence.” Journal of Urban Economics 64 (2): 234–45. Lin, C., T. Chu, and L. J. Prather. 2006. “Valuation of Mortgage Servicing Rights with Foreclosure Delay and Forbearance Allowed.” Review of Quantitative Finance and Accounting 26 (1): 41–54. McManus, D., and E. Yannopoulos. 2020. “Drivers of Mortgage Forbearance Rates during the COVID-19 Crisis.” Freddie Mac working paper. 1 This differs from mortgage principal forbearance as a component of loan modifications, whereby borrowers do not have to pay interest on a portion of the unpaid balance. 2 The source is the 2019 Survey of Consumer Finances and the measure of financial assets consists of liquid assets, certificates of deposit, directly held pooled investment funds, stocks, bonds, quasi-liquid assets, savings bonds, whole life insurance, other managed assets, and other financial assets. 3 There is extensive research focused on mortgage default, prepayment, and severity, but very limited research on mortgage forbearance. Foote, Gerardi, and Willen (2008) show that forbearance can be a highly effective tool for loss mitigation in the context of a simple theoretical model, particularly as it limits moral hazard relative to loan modification because borrowers who do not need help are unlikely to find forbearance attractive. Other research includes Agarwal et al. (2020) and Lin, Chu, and Prather (2006). 4 See https://freddiemac.gcs-web.com/news-releases/news-release-details/freddie-mac-announces-enhanced- relief-borrowers-impacted-covid, https://www.fanniemae.com/portal/media/corporate-news/2020/covid- homeowner-assistance-options-7000.html, and https://www.whitehouse.gov/briefings-statements/remarks- president-trump-signing-h-r-748-cares-act/ 5 The Mortgage Bankers Association estimates that 4.2 million U.S. mortgages (8.36%) were in forbearance in May 2020, while Black Knight Inc. estimates that 4.76 million U.S. mortgages (8.36%), representing $1.044 trillion, were in forbearance as of May 19, 2020. See https://www.blackknightinc.com/blog-posts/mortgage-forbearance-volumes-flatten-total-roughly-steady-at-4-76-million/ and https://newslink.mba.org/mba-newslinks/2020/may/mba-newslink-thursday-may-28-2020/mba-share-of-mortgage-loans-in-forbearance-increases-to-8-36/ 6 For details on forbearance impacts on Freddie Mac mortgage related securities, see https://crt.freddiemac.com/_ assets/docs/covid-19-crt-faqs.pdf and http://capitalmarkets.freddiemac.com/mbs/docs/covid_19_investor_faqs.pdf 7 In our data, forbearance and delinquency are measured independently. It is interesting that many households that enter into a forbearance agreement during the COVID-19 crisis continue to make mortgage payments. 8 Analysis by the Federal Reserve Bank of New York and the Urban Institute observes similarities between the economic fallout of the COVID-19 crisis and the experience of areas affected by hurricanes. See https://libertystreeteconomics. newyorkfed.org/2020/04/the-coronavirus-shock-looks-more-like-a-natural-disaster-than-a-cyclical-downturn.html and https://www.urban.org/sites/default/files/publication/102891/during-the-pandemic-policymakers-should- maintain-forbearance-but-fix-its-costs_0.pdf 9 Disaster related forbearance plans can be initiated by the servicer when a borrower becomes delinquent without contacting the borrower suggesting a higher incidence from a higher take-up. However, the take-up rates of forbearance in our data by borrowers that become 60 days or more delinquent is lower in the 2017 Storms period (86%) than in the COVID-19 period (95%). 10 McManus and Yannopoulos (2020) shows that forbearance rates increase with monthly payment even after controlling for the LTV ratio, the FICO score, the DTI ratio, geography, and other variables commonly used in mortgage analytics. PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP Sam Khater, Chief Economist Doug McManus, Director of Financial Research Elias Yannopoulos, Senior Macro Housing Economist