The "B" Word: Can We Spot the Next House Price Bubble?

“Are we in a house price bubble?”

That’s generally the first question I get after every presentation I make these days. The short answer is “Not yet.” But the concern is understandable. The scars are still fresh from the collapse of last decade’s house price bubble. And warning signs of a possible new bubble are accumulating.

While the evidence indicates there currently is no house price bubble in the U.S.—despite the rapid increase of house prices over the last five years—consider the following:

- House prices have been on a tear for the last five years, growing about twice as fast as the long-run average;

- House price growth has outpaced income growth by a cumulative 42 percent over the last 17 years;

- The number of large metropolitan statistical areas (MSAs) with unusually-high house-price-to-income ratios has grown from five in 2011 to 17 today. At the height of last decade’s bubble, 27 MSAs exhibited unusually-high price-to-income ratios;

- An increasing share of MSAs with relatively stable construction costs nonetheless have suspiciously high house prices per square foot.

Can we spot the next house price bubble? The experience of the mid-2000s is not encouraging. Even the experts at the Federal Reserve failed to recognize that bubble in time.

With every additional quarter of high house price appreciation, the need to understand where house prices are headed becomes more urgent. In this Insight, we assess the risk of another house price bubble. We explain why it’s difficult to spot a bubble before it bursts. We describe the approach we take to monitoring house price risk, both nationally and regionally. We also compare house price metrics today to the experience of last decade to see if any of the last bubble’s symptoms are recurring. Finally, we speculate about how today’s house prices might return to normal. Will we have a soft landing, or will we suffer through another house price collapse? Or is there a third possibility?

Three defining characteristics of a bubble

Bubbles are fueled by self-fulfilling predictions. In a bubble, prices rise simply because people expect them to keep rising. And these price increases confirm investors’ beliefs in yet more price increases. In the words of Nobel Laureate Robert Shiller,

a bubble is a kind of social epidemic—a period of feedback, where price increases generate enthusiasm among investors, who then bid up prices more, and then it feeds back again and again until prices get too high. During that period, people are motivated by envy of others who made money doing it, regret in not having participated and the gambler’s excitement. Stories develop that justify the bubble, they become current and then people think they’re right because everyone’s confirming the stories. So, that happens. Eventually prices get too high and the bubble bursts.

In retrospect, a bubble seems obvious. “We all knew” that prices had become disconnected from economic fundamentals and had reached unsustainable levels. But prior to the collapse, we all talked ourselves into thinking prices could rise even further. This psychological aspect is the reason that bubbles often are described as manias.

An anecdote—possibly true—from early California history highlights this self-delusional aspect of bubbles. In the late 1800s, a group of speculators in the Sacramento area formed a cabal with the purpose of fomenting a real estate bubble. They bought and sold parcels from each other at ever higher prices, convincing other investors that they had to purchase quickly before prices grew out of reach. One by one, members of the cabal sold out to the suckers. However, the bubble took on a life of its own, and prices continued to skyrocket. The temptation to ride the bubble higher became overwhelming. All the members of the cabal eventually reinvested, only to be wiped out when the bubble finally burst.

Which brings us to the second defining feature of bubbles—they burst. Prices frequently deviate temporarily from economic fundamentals. Stock market analysts predict the likelihood of market corrections, that is, sell-offs that bring prices back into alignment with fundamentals. And, while the distinction may be fuzzy, analysts distinguish between these corrections—a normal part of the ups and downs of asset prices—and crashes—sudden, unexpected, and significant price adjustments. Crashes reflect a sudden loss of investor confidence, a sudden realization that prices have become unsupportable.

In our view, if it doesn’t burst, it wasn’t a bubble. If the market corrects through normal mechanisms, if there’s a soft landing, then the deviation of prices from economic fundamentals, no matter how large, wasn’t a bubble. Of course, the larger the deviation from fundamentals, the harder it is for markets to stage an orderly correction and the greater the likelihood of a crash when investors finally question the inflated asset values.

The third defining feature of bubbles is the central role of easy credit in enabling the bubble to grow. Credit availability is the oxygen that keeps a bubble alive. If that oxygen is cut off, the bubble expires.

The housing bubble of the previous decade provides a good example of this aspect of bubbles. As market participants began to believe that house prices could grow indefinitely at three times their normal pace, some mortgage lenders grew less concerned with the ability of the borrower to repay the loan. After all, the expected increase in the value of the collateral would protect the lender in the event of a default. Investors in mortgage-backed securities—especially private label securities, that is, securities backed by mortgages without a guarantee against default from Freddie Mac, Fannie Mae, FHA or VA—were equally sanguine. As a result, borrowers with low credit scores found it easier to obtain mortgages, sometimes without providing any documentation of their employment, income, or assets. Demand from these borrowers stoked the rapid increases in house prices and played a part in fueling the growth of the housing bubble. The bubble collapsed when lenders finally became worried enough to restrict riskier types of credit, for instance, by freezing home equity lines of credit (HELOCs). Paradoxically, by restricting credit availability, lenders pricked the housing bubble and triggered the burst they were trying to avoid.

How we hunt for bubbles

As we noted above, bubbles are extremely difficult to identify as they are forming. There is always the possibility prices will adjust gradually to economic fundamentals rather than collapse suddenly. Moreover, it’s possible that claiming to identify a bubble will, by itself, spook lenders and investors and trigger a crash that didn’t need to happen. It’s always tempting to monitor conditions a little bit longer rather than take action, especially since it may be difficult to know what sort of action might prevent the bubble from bursting. Unfortunately, at Freddie Mac we’re stuck. A potentially-destructive house price bubble is one of the key risks we have to manage as best we can.

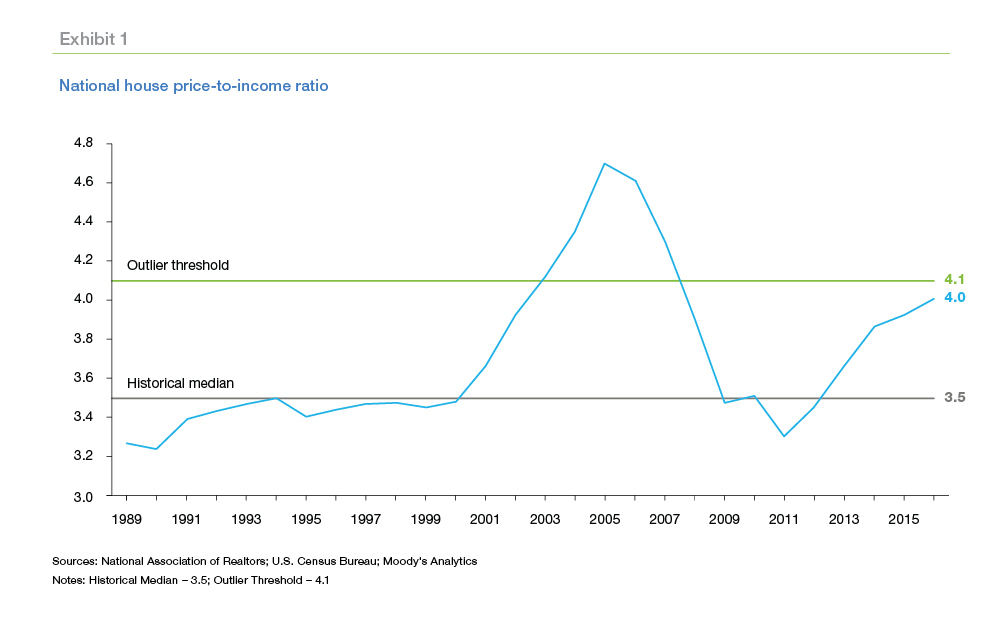

In last year’s Insight, “How to Worry About House Prices,” we described the two-part approach we have adopted to identifying areas with unusually-high house prices. The first part of the approach compares the current ratio of the median house price to the median household income (PTI ratio) to a historical norm. Exhibit 1 displays the national PTI ratio along with two reference lines.

The lower line is drawn at a ratio of 3.5, which is the historical median. The upper line is drawn at a ratio of 4.1. A statistical rule for identifying outliers suggests that a national PTI above 4.1 is an unusual occurrence, unusual enough to merit further analysis.

The time path of the housing bubble, crash, and recovery are plain to see in this exhibit. The national PTI ratio increased sharply in the early 2000s and broke through the 4.1 outlier threshold by 2004. The ratio started to collapse in 2006 and bottomed out at 3.3 in 2011. The ratio has risen since then and currently is approaching, but still is under, the outlier threshold.

Housing bubbles can occur at a local or regional level without triggering a national bubble. Accordingly, we also track the PTI ratios for the 50 largest metro areas. House prices evolve very differently in each metro, so we calculate the median PTI ratio and outlier threshold separately for each metro. As an example, housing costs claim a larger portion of household income in San Francisco, where the median PTI is 9.0, than in Dallas, where the median PTI is 3.9. In addition, the volatility of the PTI ratio is higher in San Francisco than in Dallas. As a result, it takes a very high PTI in San Francisco to attract our attention, while a PTI ratio barely above the national median is cause for concern in Dallas. Exhibit 2 displays the metros with unusually high PTI ratios, relative to their historical experience, as of the second quarter of 2017. Currently this metric highlights 17 of the 50 largest metros.

An unusually-high PTI ratio, by itself, is not persuasive evidence of a house price bubble. To refine the analysis, we look for three other types of evidence. First, we look for signs that the currently-high prices can be attributed to economic fundamentals. Remember that bubbles are a type of mass delusion that prices can continue to rise independent of any fundamental factor.

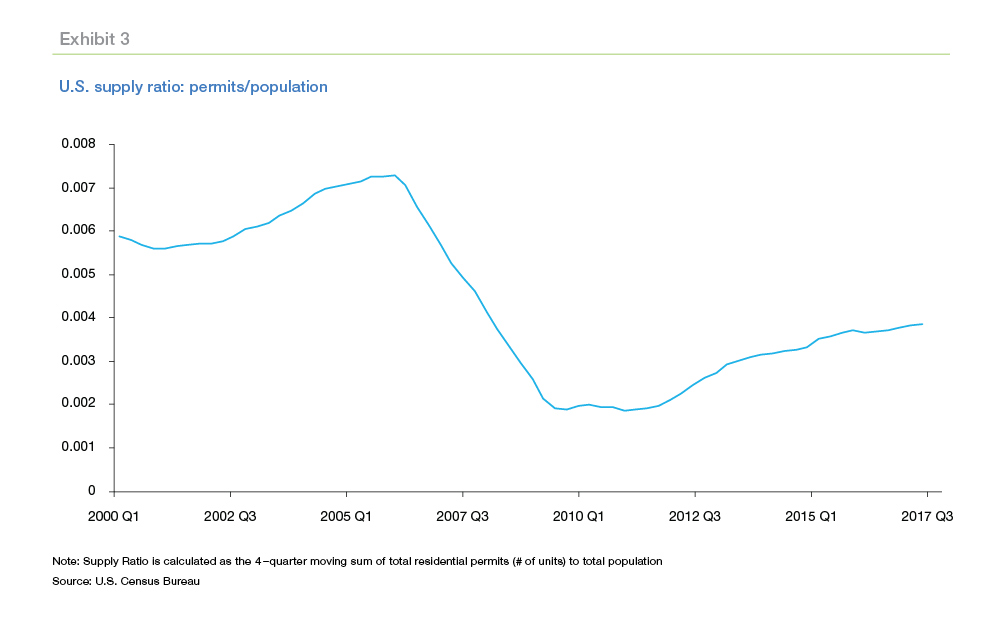

The most important fundamental in today’s housing market is the lack of houses for sale that affects virtually all of the largest metros in the U.S. As a rule of thumb, an inventory sufficient to cover six months of sales indicates a rough balance between the supply of and demand for houses. Based on Redfin data, there were 3.3 month's supply of housing inventory in September of this year. Among metro areas, inventories range from less than a month's supply in San Jose, CA to over 5 month's supply in New Orleans, LA.

Houses are not being built fast enough to close this gap. Exhibit 3 displays the ratio of housing permits to the population in the U.S. Following last decade’s house price collapse, this ratio fell to a third of the level in 2000. While it has been rising slowly since the end of 2011, it still stands at less than two-thirds of the 2000 level.

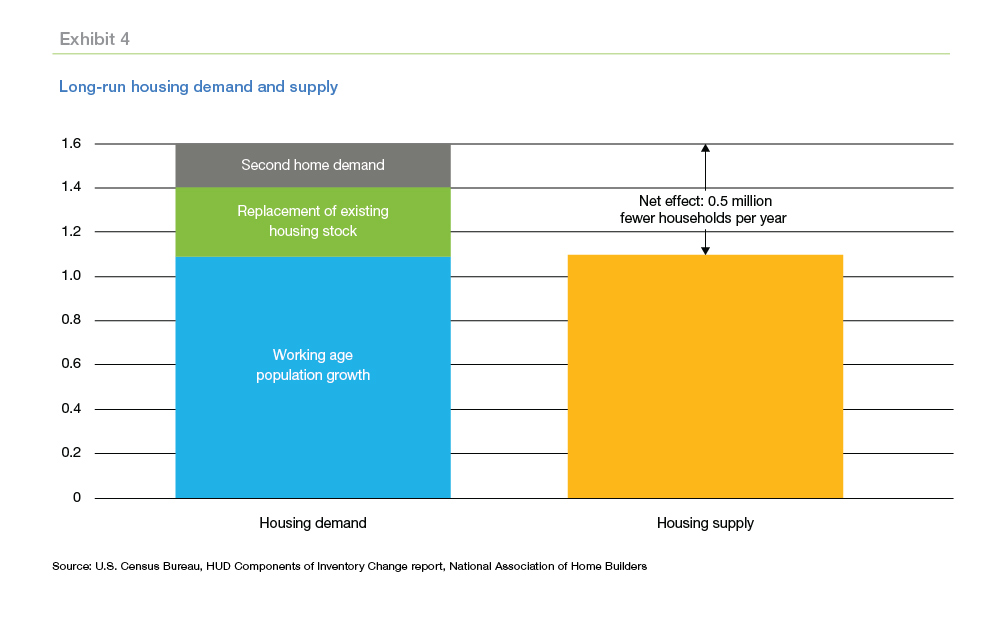

The evidence suggests construction is unlikely to increase fast enough to relieve the shortfall of houses for at least several more years. We estimate that the rate of new home construction falls approximately 500,000 houses short of the amount required to meet the growth in demand (Exhibit 4).

The shortage of houses for sale is strong evidence against a house price bubble. And the difficulty of increasing residential construction quickly suggests that any price adjustment will be gradual. As a result, we don’t expect to see a rapid collapse of the currently-high prices.

Despite this compelling evidence against a bubble, for completeness, we look at two additional types of evidence. Remember that a bubble requires easy credit availability. To see if credit is too loose, we look for signs of credit deterioration—increasing delinquencies and defaults. As it happens, this type of evidence is likelier to occur very late in the life of a bubble, just before it bursts. So it is not surprising that we don’t find evidence of credit deterioration. On the contrary, the current book of business has exhibited stellar credit performance to date.

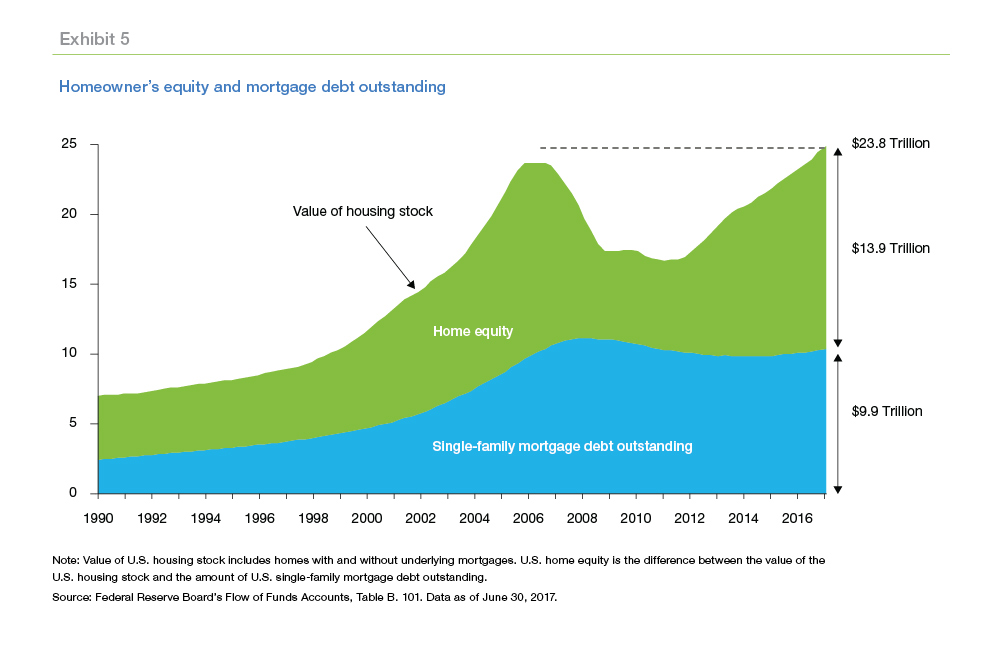

Another sign of easy credit is an increase in leverage, that is, borrowers tapping the equity in their homes to fund more consumption. A significant increase in leverage is likely to be the first warning sign of too-easy credit. However, the evidence to date is just the reverse. Exhibit 5 displays the value of the U.S. housing stock from 1990 to the present. The blue region at the bottom represents the amount of mortgage debt outstanding. The green region above it represents homeowners’ equity, that is, the difference between the value of the homes and the amount of mortgage debt outstanding. The increase in leverage in the housing bubble years stands out clearly. However, while house prices have risen rapidly since 2011, mortgage debt outstanding has barely budged. Homeowners, at least in aggregate, are not funding a spending spree with the equity in their homes.

Based on this analysis, there is no sign of an imminent bubble. However, house prices have been rising at twice the long-run equilibrium rate for over five years now. It’s possible that we’re looking in the wrong places for evidence. Perhaps we need to cast our nets a little wider.

What were the warning signs of the last bubble?

As Exhibit 1 shows, the national house price to household income ratio (PTI ratio) provided one warning of last decade’s house price bubble. Moreover, it provided a warning in plenty of time to take corrective action before the bubble burst. But given the difficulty of identifying a bubble, one possible warning sign isn’t enough. We need confirming evidence.

Perhaps there were other metrics, other warning signs, that preceded last decade’s house price collapse. By comparing the behavior of those metrics last decade to their current behavior, we may be able to accumulate a body of evidence that either warns us of an incipient bubble or, alternatively, convinces us that no new bubble is imminent.

Flipping

Robert Shiller has speculated that a sharp increase in flipping—buying a house and fixing it up for quick resale—may have contributed to last decade’s house price bubble. An increase in flipping indicates speculators project house price increases in the near future.

Exhibit 6 displays the number of homes flipped in a year as a percentage of home sales in that year. Sharply higher shares are apparent in 2004 through 2006. Home prices peaked in 2006, suggesting that flipping may provide an early warning that a growing bubble may burst soon. We drew two horizontal lines to serve as provisional thresholds. When flipping crosses the lower line, it may be time to look more carefully for other signs of overvaluation. When flipping crosses the upper line, it seems likely that the bubble has already grown to dangerous levels.

The share of flipping exceeded the lower threshold, but not the upper one, from 2010 through 2014, a period of strong house price growth. House prices were still falling in 2010 and parts of 2011 and 2012. The high share of flipping in those years most likely reflected investor purchases of foreclosed properties and short sales. However, 2013 and 2014 enjoyed high home price appreciation. The high share of flipping in those years may reflect both a continuation of purchases of distressed properties and a growing belief among investors that the crisis was over.

The modest decrease in the share of flipping after 2014 leaves this metric below the lower threshold. Today’s volume of flipping doesn’t appear to be pointing to a house price bubble.

Price per square foot

The price of a house per square foot depends on construction costs (including costs added by regulation) and the cost of land. While construction costs have increased over time, the rate of increase is moderate and fairly stable. As a result, in areas where buildable land is plentiful and land use restrictions are modest, the price per square foot of a house should remain stable as well. The ability of builders to supply additional houses at a roughly constant construction cost per square foot normally prevents the price per square foot of existing houses to rise too much.

It is important to note that this relationship won’t hold in cities like San Francisco or Seattle where geographic constraints on buildable land limit increases in the supply of new homes. In these cities, increases in the demand for houses produce sharp increases in the house prices, but very few new houses. As a result, swings in demand for houses in these cities can generate big swings in the price per square foot of new houses.

But, in cities like Dallas and Kansas City—where there are few restrictions on increasing the supply of houses—the price per square foot of a new house should track construction costs fairly closely and should therefore remain reasonably stable in the face of big swings in demand. In these cities, sharp increases in price per square foot are likely to indicate a house price increase that cannot be sustained.2

Exhibit 7 (following page) displays the average, inflation-adjusted price per square foot of houses (both existing and new) excluding cities like San Franciso or Seattle. This average increased steadily prior to the house price collapse, plunged during the collapse and recession, and resumed increasing after 2011. Today the average remains below the level in 2004.

Exhibit 8 provides another view of these data. This exhibit displays the share of MSAs with real price per square foot above $150. This metric crossed the 10 percent share mark in 2004, then plunged in 2007. Recently the share has increased and is approaching 10 percent again.

Price-to-Income contagion

While the national PTI ratio remains below its outlier threshold, the share of large metros with unusually high PTI ratios has been growing since 2011. Exhibit 9 displays this share from 1993 through the present. The share peaked at 54 percent in 2006, then fell to 10 percent in 2011. Recently, as of the second quarter of 2017, the share had risen to 34 percent, however it appears to have plateaued at a level below its previous peak.

Exhibit 10 is a “measles” chart—the red dots on the maps highlight the high-PTI metros in each displayed year. In the upper row of maps, the PTI contagion from 2001 to 2004 to 2007 is striking. The three maps in the lower row display a similar trend of contagion from 2010 to 2013 to 2016, although the 2010 map shows more initial contagion than the 2001 map above it.

As with the other warning signs, this indicator suggests a trend of price increases similar to, but not quite as extreme, as the trend during the build-up of last decade’s house price bubble.

Exhibit 10 looks worrisome, but, as we mentioned above, high PTI ratios are not definitive evidence of bubble conditions. One important reason is the correlation between mortgage rates and PTI ratios. When mortgage rates drop, monthly principal and interest payments decrease on new mortgages. As a result, a potential borrower can qualify for a larger mortgage—and, thus, a more expensive house—than previously. And the data indicate that is precisely what borrowers do. It’s not clear whether lower mortgage rates incent borrowers to buy different houses than they would have otherwise or whether the prices of the homes they were considering are simply bid up. Either way, the end result is higher PTI ratios.

Exhibit 11 displays the yearly average of the 30-year mortgage rate for the six years covered by Exhibit 10. During the pre-crisis years, the number of MSAs with high PTI ratios grew despite mortgage rates between six and seven percent. During that period, the increase in high-PTI MSAs tracked the growth of the house price bubble. In contrast, the increase in the number of high-PTI MSAs in the post-crisis years tracks the decline in mortgage rates from roughly 4-3/4 percent in 2010 to 3-3/4 percent in 2016. As a result, the increase in high-PTI MSAs since 2010 appears unlikely to signal another bubble.

To B or not to B

That is the question. Given the evidence above, what are the odds we are in—or are approaching—another house price bubble?

Despite the substantial house price increases in recent years and the evidence that house prices are unusually high in a growing number of metro areas, we do not believe there is a house price bubble at present. Here’s why:

- First, the primary reason for the high and rising house prices is the shortage of houses for sale. As we showed in Exhibit 4, residential construction is falling roughly 500,000 homes short of demand every year. And that annual shortfall ignores the pent-up demand that accumulated during the previous decade.

- Second, easy credit is not fueling housing demand. Qualifying for a mortgage is more difficult today than it was at the beginning of this century, a period that some analysts use as a reference for a “normal” mortgage market. Exhibit 12 displays the Housing Credit Availability Index (HCAI) published by the Urban Institute. This index measures an estimate of the default risk lenders are willing to accept on purchase loans for owner-occupied houses. This chart displays the Urban Institute’s estimate of the probability of default for the entire mortgage market. The probability of risk for loans guaranteed by the GSEs is much lower, as confirmed by the Urban Institute’s GSEonly HCAI charts. Currently lenders have reduced their default risk by more than half relative to the 2001-2003 reference period.

- Third, as shown in Exhibit 5, homeowners are not increasing their mortgage leverage. The sharp growth in house prices is generating an almost dollar-for-dollar growth in homeowners’ equity with only negligible changes in mortgage debt outstanding.

Where do we go from here?

We’re not in a bubble today, but what about tomorrow? How long can house prices appreciate at twice their historical average?

Historically, house prices have deviated from economic fundamentals for long periods of time. Exhibit 13 displays the 10-year growth rates of house prices and GDP per capita, a measure of income. Over the last 75 years, house price growth and income growth clearly have differed significantly for long periods of time.

Nonetheless, isn’t there a limit to the price-to-income ratio? Median household income currently stands at roughly $60,000. Can a household with the median income really buy a $600,000 house? A $1,000,000 house? A $2,000,000 house?

How can borrowers continue to qualify for the mortgages needed to purchase ever-more expensive houses? Underwriting standards place limits on the ratio of a borrower’s debt to his or her income. A high debt-to-income (DTI) ratio increases the probability a borrower may be unable to meet all their obligations at some point in the future. A high DTI ratio is the most common reason for rejecting a mortgage application.

A higher house price increases a borrower’s DTI ratio.3 In some cases, borrowers may qualify for a mortgage with a total DTI ratio (mortgage debt plus non-mortgage debt) as high as 50 percent. Exhibit 14 displays the percentage of recent borrowers whose DTI ratio would exceed 50 percent at various hypothetical increases in house prices.4 This calculation indicates that house prices would have to rise more than 90 percent before half these borrowers would breach the 50 DTI ratio limit. As a comparison, house prices have increased by a cumulative 43 percent since the national house price trough in 2011. It appears that house prices can increase a lot more before a significant share of borrowers are priced out of the market.

While house prices can deviate from fundamentals for many, many years, the long-run relationship between house prices and incomes is always restored eventually. At present, the gap between the demand for houses and the limited supply of houses for sale is bridged by high and ever-rising house prices. This equilibrating mechanism is responsible for the high PTI ratios that are spreading across the U.S. But eventually—perhaps several years from now—the economy will adjust so demand and supply are balanced at a level of house prices more in line with household income.

How will that adjustment take place this time? Will there be a sudden disruptive correction to house prices that roils the economy again? Or is a soft landing likely? Here are a few possibilities.

Scenario 1: Soft landing

Increases in residential construction may eventually slow the rate of house price appreciation. Although residential construction currently falls short of the growth in housing demand, construction is trending up, albeit slowly. That slow pace of improvement is not all bad; it prevents a sharp drop in house prices that could impose losses on recent homebuyers.

The shortage of available houses and the ultra-high prices in areas like San Francisco have created momentum for revisions to some of the regulations that limit development and drive up its costs. Revision of these regulations might accelerate the upward trend in construction somewhat, closing the gap between supply and demand more quickly.

Finally, Baby Boomers are living longer, healthier lives and are determined to age in place. They have been slower than previous generations to sell the family home, thus exacerbating the shortage of houses for sale. Eventually, however, the increasing frailty and mortality of the Boomers will release more and more of these houses to the market. As with the increase in residential construction, this trend will be gradual, thus cushioning the market against sudden decreases in house prices.

On the demand side, Millennials have been slower to purchase their first homes than previous generations. Economists debate the reasons for this pattern—some point to the burden of high student debt, others highlight the low marriage rate of the Millennials, and others focus on the decreases in labor force participation and mobility. In any event, a continuation of this low homeownership rate can serve to take some of the heat out of the demand for houses.

Scenario 2: Homeownership down, rentership up

Residential construction may remain perennially stuck at a level too low to meet the growth in demand. In addition, Federal Reserve actions to boost interest rates and unwind their portfolio of mortgage-backed securities may increase mortgage rates significantly. In this scenario, house price appreciation will accelerate and housing will become even less affordable than it is today. Regulatory constraints on residential development are likely to become more restrictive as existing homeowners lobby to protect the value of their housing investments.

In this scenario, equilibrium is restored by creating a permanent division between the housing “Haves” and “Have Nots.” First-time homebuyers and moderate-income households are likely to face particularly severe challenges to homeownership. Housing will become increasingly bifurcated between the affluent and everyone else. In addition, wealth inequality is likely to increase as fewer households are able to take advantage of the wealth-building associated with homeownership. Single family rental will increase, particularly if regulatory constraints limit higher-density, multifamily development.

Scenario 3: Demand/supply imbalance triggers a bubble

A worsening of the imbalance between the demand for and supply of housing could eventually create a bubble where none currently exists. After another few years of rapid house price increases, memories of last decade’s crash could fade and expectations of future house prices could reset higher. Some of the bad practices of the previous decade could return. For instance, if wage growth remains tepid and mortgage rates remain low, borrowers may once again start borrowing against the equity in their homes to finance higher consumption. The cycle of house price increases followed by additional borrowing eventually becomes unsustainable, and the bubble bursts.

Conclusion

The evidence indicates there currently is no house price bubble in the U.S., despite the rapid increase of house prices over the last five years. However, the housing sector is significantly out of balance. The incomplete recovery in residential construction following the crisis of the last decade has created several years of pent-up demand for household formation. What we can’t predict is how this imbalance will eventually be resolved. Will there be a gradual restoration of a normal balance between supply and demand? Alternatively, will the rate of home building remain stubbornly low, exacerbating the income and wealth inequality that followed the Great Recession? Another bubble appears to be a less probable scenario, but not an impossible one.

1 See “How to Worry About House Prices” for details about this calculation.

2 See “Is Geography Destiny” for a fuller discussion of the difference in house price dynamics in these different types of cities.

3 Assuming a constant percentage down payment

4 Based on Freddie Mac fundings of single-family, fixed-rate, purchase-money mortgages from April through July 2017. Assumes income, non-housing debt payments, LTV, term and interest rates are unchanged.

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP

Sean Becketti, Chief Economist

Len Kiefer, Deputy Chief Economist

Ajita Atreya, Quantitative Analytics Senior

Penka Trentcheva, Quantitative Analytics Senior

Venkataramana Yanamandra, Quantitative Analytics Senior