Quarterly Forecast: Rapidly Rising Rates & Declining Demand Driving a Housing Market Slowdown

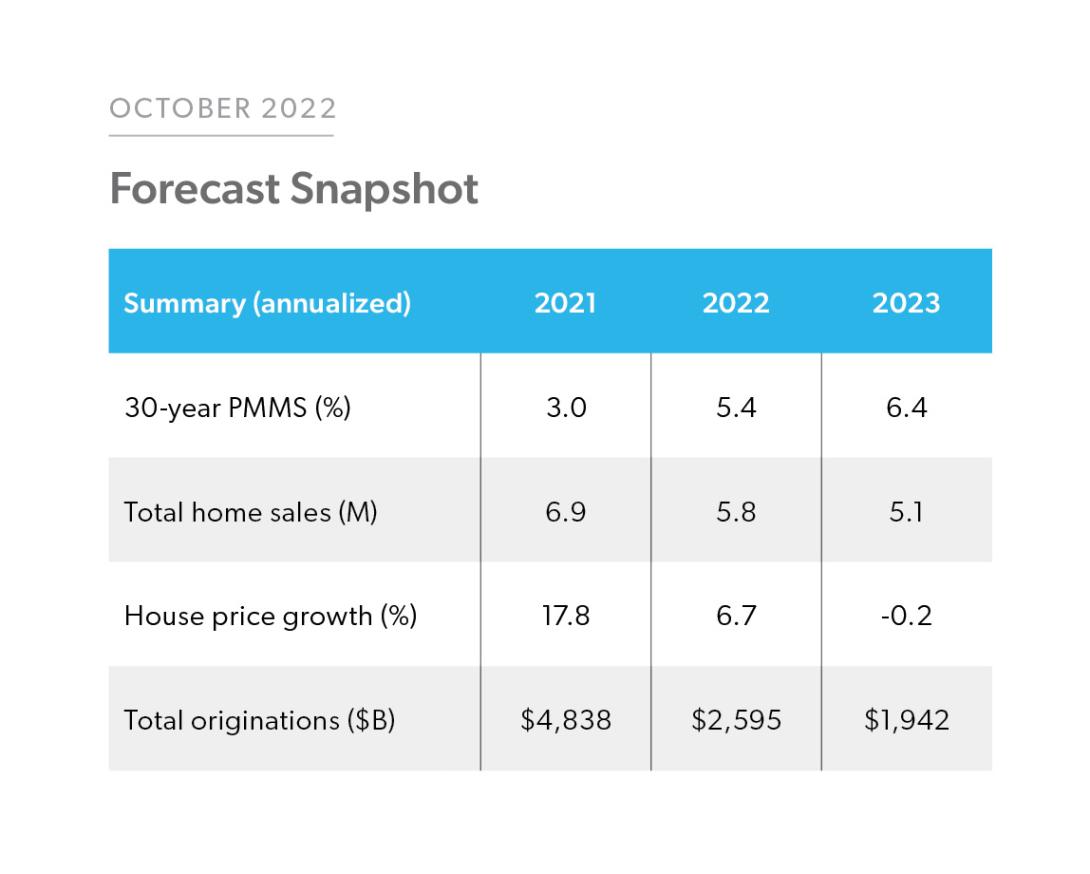

Mortgage interest rates have increased at the fastest rate since the early 1980s. The U.S. weekly average 30-year fixed-rate mortgage was 6.94% in the week of October 20, 2022, up 3.85 percentage points from a year ago according to Freddie Mac’s Primary Mortgage Market Survey. In the history of the Primary Mortgage Market Survey, which stretches back to April 1971, mortgage rates have only increased faster in 1980 and 1981. However, in 1980 and 1981, rates averaged 16% and 18%, respectively. Just one year ago, rates were under 3%. This means that while mortgage rates are not as high as they were in the 80’s, they have more than doubled in the past year. Mortgage rates have never doubled in a year before.

The increase in mortgage interest rates has been driven by a general increase in interest rates throughout the economy, which in turn have been primarily driven by inflation. Inflation rates have remained stubbornly high, and the Federal Reserve’s Federal Open Market Committee (FOMC) has responded by increasing their policy rate by 3 percentage points thus far in 2022. Market participants are broadly expecting the FOMC to continue increasing their policy rate this year.

The September 2022 employment report released by the U.S. Bureau of Labor Statistics indicated that the U.S. economy added 263,000 nonfarm payroll jobs in September, and the unemployment rate ticked down to 3.5%. The U.S. economy has now added back all the jobs lost during the pandemic recession and more. Total nonfarm employment as of September 2022 was half a million higher than the pre-pandemic level in February 2020. Nonfarm payroll growth has averaged 420,000 per month in 2022, which is well above 177,000 job gains which was the average from January 2017 through December 2019.

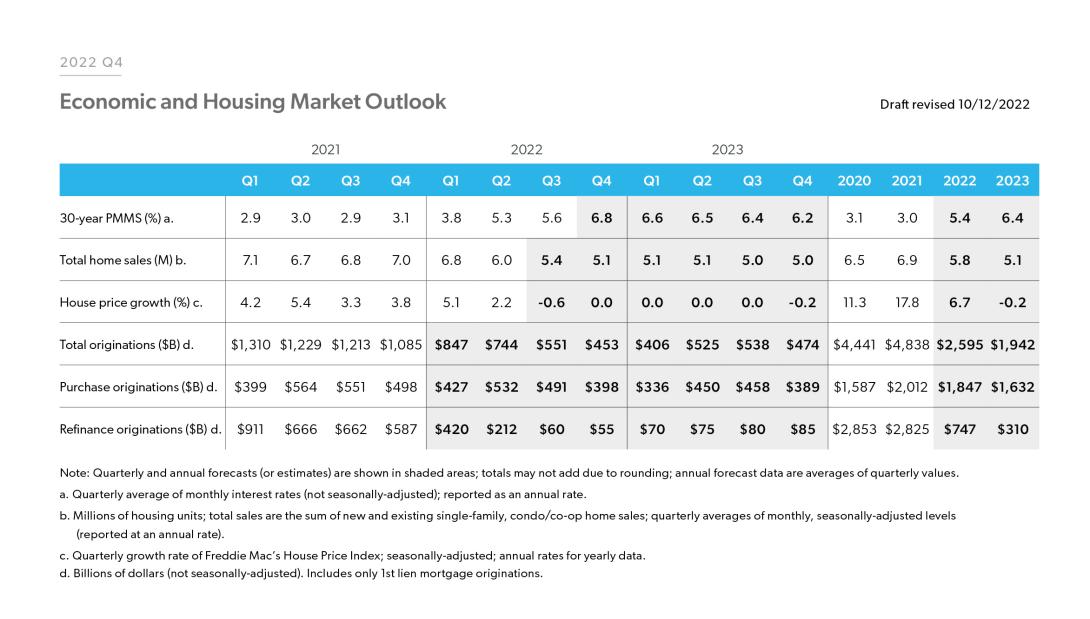

While the labor market remains strong, the impact of the FOMC’s rate increases earlier this year will only be felt with a lag and, while job growth is above its pre-pandemic average, it has shown signs of gradually decelerating. This is reflected in implied forward yields for the U.S. 10-year Treasury, which are flat over the next five quarters. Mortgage rates generally follow 10-year Treasury yields, which would indicate that rates should be flat given the path of Treasuries. However, in recent months the spread between the primary mortgage rate and 10-year Treasuries has widened as the mortgage industry adjusted to dramatically lower transaction activity and recent interest rate volatility. If spreads gradually return closer to historical averages, then mortgage rates will decline modestly over the next year. This is reflected in our forecast which has rates dropping from an average of 6.8% in the fourth quarter of 2022 to 6.2% in the fourth quarter of 2023.

The housing market rapidly decelerated as markets absorbed the impact of higher mortgage rates. Home sales have fallen to a forecasted 5.4 million units at a seasonally adjusted annual rate in the third quarter of 2022 from 7 million earlier this year. Home purchase mortgage applications point to continued contraction in home sales activity. We forecast that home sales activity will bottom at around 5 million units at the end of next year. Falling from 7 million to 5 million would be a decline of about 30% and put the contraction in home sales in line with other historical periods when interest rates increased.

As housing market activity continues to contract, we expect that it will lead to a continued increase in the months’ supply of homes available for-sale from historically low levels last year. The loosening of the once incredibly tight for-sale inventory removes the intense upward pressure on home prices of the past two years. While fewer sales are increasing the months’ supply, that is partially offset by fewer new listings as high mortgage rates disincentivize existing homeowners from moving up or downsizing.

House prices increased by about 40% since 2020 (vs. cumulative inflation of 15%) but the spike in mortgage rates has caused a correction in house prices. We expect house prices to decline modestly, but the downside risks are elevated. As the labor market cools off, housing demand will remain weak in 2023, potentially resulting in declines in prices next year. However, home price forecast uncertainty is wide due to interest rate volatility and the potential of a recession on the horizon.

Given the house price and home sales forecast, we estimate home purchase mortgage originations to be $1.9 trillion in 2022, slowing to $1.6 trillion in 2023. With mortgage rates expected to remain elevated, we forecast refinance activity to slow with refinance originations declining from $2.8 trillion in 2021 to $747 billion in 2022 and $310 billion in 2023. Overall, we forecast total originations to decline from the high of $4.8 trillion in 2021 to $2.6 trillion in 2022 and $1.9 trillion in 2023.

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP