Economic, Housing and Mortgage Market Outlook – November 2024

In this Issue

- The U.S. economy remains resilient with strong Q3 growth even as the labor market moderates.

- Recent volatility in mortgage rates has weighed on housing and mortgage activity.

Recent developments

U.S. economy: The U.S. economy continues to grow at a robust pace, as evidenced by the advance estimate of Q3 2024 seasonally adjusted annual rate of growth of Real Gross Domestic Product (GDP).1 Growth for Q3 was 2.8%, a slight decrease from the rate of 3.0% in the second quarter, but well above the long-run potential growth of 1.8% estimated by the Congressional Budget Office (CBO). As with the previous quarters, in Q3 2024, consumption spending led the growth and at 3.7%, grew at the fastest pace since Q1 2023. Consumption spending has remained resilient even in the face of high inflation and a still-high interest rate environment. The contribution of this component to overall growth was around 2.5 percentage points. Compared to Q2 2024, the decrease in Q3 GDP growth was primarily due to a downturn in private inventory investment and a significant deceleration in residential fixed investment. This was partially offset by increases in exports, consumer spending, and federal government spending.

The labor market continued to moderate. Per the latest employment report from the Bureau of Labor Statistics (BLS), payroll growth for October witnessed a sharp decline, with the economy adding only 12,000 jobs. However, this slowdown was mainly attributed to Hurricanes Helene and Milton, which hit the Southeastern part of the country, and a strike at Boeing that subtracted around 44,000 jobs from the manufacturing sector. Despite facing temporary disruptions in job growth, the unemployment rate stayed consistent at 4.1% for the second month. Average hourly wage growth also remained at 4% on a year-over-year basis. While the payroll gains for October came in at the lowest level since December 2020, these declines led by temporary events are not a major cause for concern.

As measured by the Employment Cost Index, compensation costs for civilian workers, increased 3.9% in Q3 2024. This is a decrease from the second quarters’ increase of 4.1% and is the lowest since late 2021. This decrease further shows wage growth moderating amid a softening labor market.

Inflationary pressures have been receding over the past few months, but remain above the Federal Reserve’s target of 2%. Core Personal Consumption Expenditure (PCE) Price Index, the Federal Reserve’s preferred inflation gauge, rose 0.2% over the month in August and 2.7% from a year ago. Prices for goods have been leading the slowdown in overall inflation with a 0.1% monthly decline and a 1.2% yearly decline in September. Conversely, prices for services continue to rise and were up 0.3% month-over-month and rose 3.7% from a year ago.

Economic growth for Q3 2024 remained strong and above the long run trend growth estimate. With the labor market continuing to moderate and inflation cooling towards the Fed target of 2%, and the Federal Reserve might continue on its implied rate cut path.

U.S. housing and mortgage market: Home sales remained subdued despite mortgage rates declining and hitting 2-year lows in September. Total (new + existing) home sales fell 0.2% in September as homebuyers wait for rates to decrease. Existing home sales continued their downward trend with sales in September at the lowest level since October 2010 at 3.84 million. Existing sales continue to reel under the pressure of high mortgage rates and the rate lock-in effect. New home sales rose slightly to 738,000 in September, with the pace of new home sales continuing to run above the pre-pandemic average. In the face of increasing mortgage rates, more builders are using sales incentives and therefore making new homes more attractive for potential buyers. Slower sales have led to a slight pick-up in inventory, with the supply of existing homes at 4.3 months in September, the highest since October 2020. However, despite the recent increase, months’ supply remains low by historical standards and is below the 5 to 6 months’ supply that is typically considered consistent with a balanced housing market.

Housing construction also decelerated in September. Total housing starts declined 0.5% from August and 0.7% from last September. This decrease was primarily due to a slowdown in multifamily construction, which decreased over 15% from last September. Homebuilder confidence inched up for the second consecutive month to 43, according to the National Association of Home Builders’ Housing Market Index. Though increasing for the second time in six months, the index has remained below 50 since August 2023, indicating that building conditions are expected to remain poor in the near term.2

House price appreciation continued to slow from the highs witnessed in 2022. As measured by the FHFA House Price Index, U.S. house prices in August 2024 rose 0.3% month over month and 4.2% from last year. All nine census divisions showed annual increases, ranging from 2.4% in the West South Central division to 6.3% in the East North Central division.

Higher mortgage rates and low affordability impacted the homeownership rate in Q3 2024. The homeownership rate was slightly lower at 65.6% in Q3 2024 compared to 66% in Q3 2023, per the Residential Vacancies and Homeownership Report by the U.S. Census Bureau. Between Q3 2023 and Q3 2024, the total number of housing units rose from 145.4 million to 147.0 million, an increase of around 1.5 million units. Occupied units increased by 1.7 million, while vacant units fell by 0.2 million. Most notably, the increase in occupied housing units was primarily driven by renter-occupied units which increased by 1.1 million units from 44.3 million in Q3 2023 to 45.5 million in Q3 2024. However, owner-occupied units increased only 0.6 million units from 86.0 million to 86.6 million. The homeowner vacancy rate ticked slightly up from 0.9% in Q2 2024 to 1.0% in Q3 2024 and was up from 0.8% in Q3 2023. The renter vacancy rate at 6.9% in Q3 2024 increased from 6.6% in Q2 2024 and from the 6.6% a year ago. The increase in rental vacancy reflects a large backlog of recently completed multifamily construction projects, boosting the number of units available.

Mortgage rates rose from their two-year low, seen in September at 6.08% and reached 6.72% as of the last week of October. The 30-year fixed-rate mortgage as measured by Freddie Mac’s Primary Mortgage Market Survey® averaged 6.43% in October. While homebuyers are waiting on the sidelines for mortgage rates to go down, especially after the 50-basis point rate cut by the Federal Reserve, most of the declines in rates were already baked in by the first Fed rate cut.

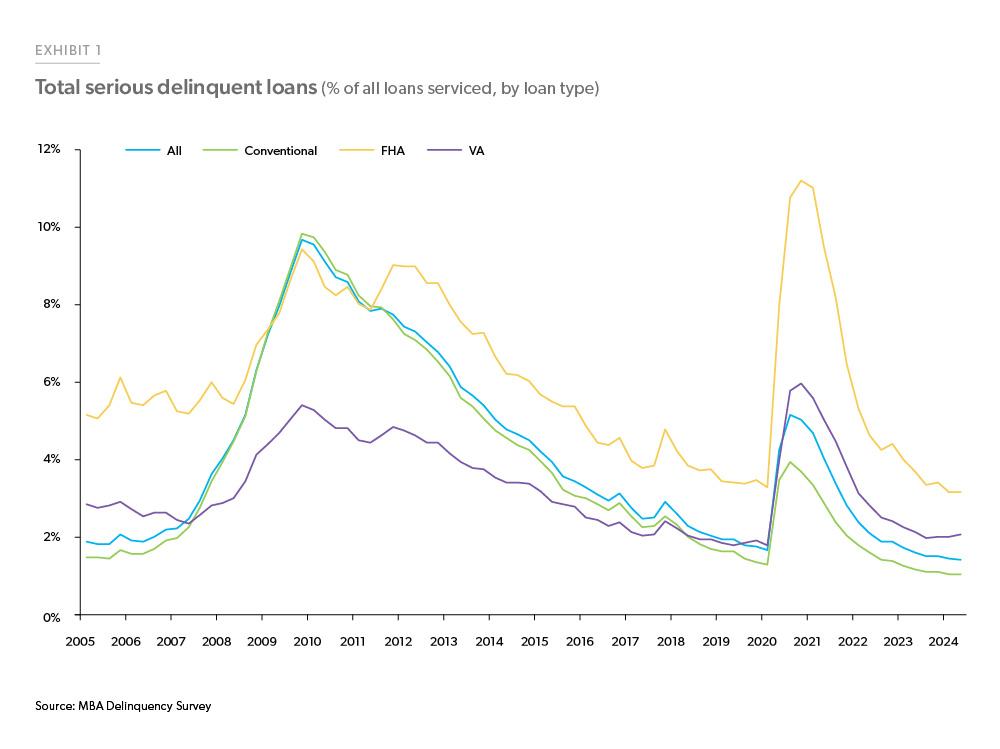

Exhibit 1 outlines the change in mortgage rates in the 12 weeks prior and the 12 weeks after the first Fed rate cut in seven episodes since the 1990s. As can be seen from the chart, rates begin declining in anticipation of the Fed rate cut but after the cut, rates remain stable and decline only very gradually. While the Fed usually cuts rates during times of economic distress, this time is different. The U.S. economy remains in a position of strength. Since the first Fed rate cut in September, mortgage interest rates are up nearly ¾ of a percentage point, which is more than average and speaks to the unique circumstances in the economy today.

Rising rates are unwelcome news to potential homebuyers who might have been hoping that Fed rate cuts would result in lower mortgage rates. However, if we look back historically at past rate cutting cycles, we see that interest rates typically do not fall much following a rate cut. If we look at the previous 6 rate cutting cycles, 6 weeks after the initial Fed rate cut mortgage rates increased on average 0.1 percentage points. This is because mortgage rates are influenced by the long-term rates, which already priced in the Fed rate cut. With economic growth surprising on the upside, bond market participants are starting to consider a slower pace of future rate cuts and factor in the potential for higher-than-expected inflation in the near-term. This has resulted in upward pressure on long-term rates, including mortgage rates.

Recent volatility in rates has weighed on housing and mortgage activity. Existing home sales have fallen to 14-year lows. Refinance activity, which witnessed a boomlet in September, is also receding as rates are on the rise again.

Outlook

Our outlook has not been adjusted to reflect any impact of the U.S. election. As such, we have not factored in any potential changes to the U.S. fiscal outlook or other policy.

While the U.S. economy continues to surprise on the upside, we expect a moderation in economic growth in 2025. This is due to a further cooling of the labor market and a potential decrease in consumer spending. Under our baseline scenario, we expect inflation to continue to move towards the Federal Reserve’s target rate of 2%. As a result, we expect the Federal Reserve to implement further rate cuts in the upcoming meetings.

Mortgage rates rebounded rapidly from the 2-year lows in October and are back up above 6.7%. In the near- term, rates may continue to be volatile and higher rates will keep home sales muted for the remainder of this year. But as we get into 2025, we anticipate that rates will gradually decline throughout the year. The expected decline in mortgage rates in 2025 should loosen some of the rate lock-in effect for existing homeowners, offering more inventory in the market. The rate lock-in effect for October increased again as mortgage rates increased — up from $38,000 in September to $42,000 as of October 2024. Lower rates and the boost to inventory should lead to slightly higher home sales in 2025. We expect house prices to continue to grow, although at a slower pace.

In the mortgage market, as of Q2 2024, total purchase volumes were $336 billion while refinance volumes were $93 billion for a total volume of $429 billion. For 2025, we expect the decline in rates to boost refinance origination volumes. This, coupled with expected increase in purchase originations due to a modest growth in home sales and home prices, should improve the mortgage market in 2025. We forecast total origination volumes to increase modestly in 2025.

See the November 2024 spotlight on “housing supply.”

Footnotes

- Bureau of Economic Analysis (BEA)

- The NAHB Housing Market Index is a diffusion indexed constructed so that a value of 50 indicates sentiment is on balance neutral, while values above (below) 50 indicates that sentiment is on balance positive (negative).

Prepared by the Economic & Housing Research group

Sam Khater, Chief Economist

Len Kiefer, Deputy Chief Economist

Ajita Atreya, Macro & Housing Economics Manager

Rama Yanamandra, Macro & Housing Economics Manager

Penka Trentcheva, Macro & Housing Economics Senior

Genaro Villa, Macro & Housing Economics Senior

Caroline Cheatham, Finance Analyst