What Do Borrowers Do When a Mortgage Application Is Denied?

Approximately 13% of all purchase mortgage applications — a total of nearly 650,000 — were denied in 2020, according to Housing Mortgage Disclosure Act data. Although the housing finance industry may understand the basic denial causes, discovering how applicants respond after a denial can inspire potential solutions to increase the pool of approved applications going forward.

To that end, in April, Freddie Mac’s Market Insights team conducted a quantitative and retrospective study among consumers whose mortgage application had been denied in the past four years. The study seeks to understand why a borrower’s loan was denied and the actions the borrower took before and after denial.

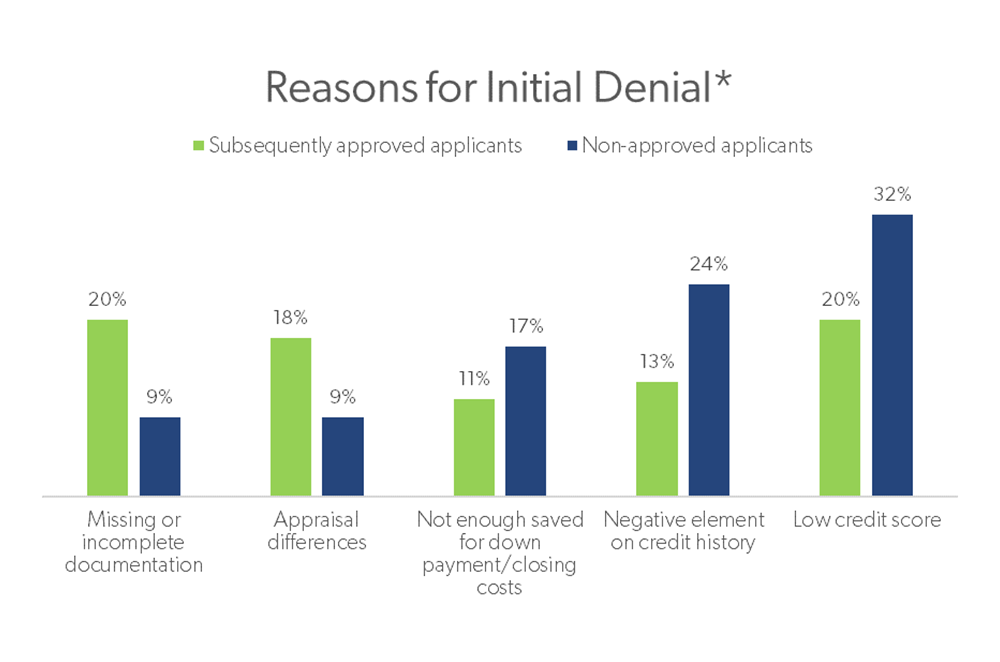

Reasons for Denial

Reasons for mortgage application denials do vary, however, three in five survey respondents cited debt or credit issues as reasons given for their initial denial. Notably, our research found that one in five Black applicants were denied due to a negative element on their credit history, which is a significantly higher number than White (16%) or Hispanic (12%) applicants.

Overall, our survey showed that the category of issue that resulted in a denial was a key factor in whether an applicant was subsequently approved or not.

Applicants who were subsequently approved for a mortgage were more likely to report they were initially denied for reasons considered to be “quick fixes,” such as:

- Missing or incomplete documentation. (See chart below for a full breakdown.)

- Appraisal differences.

Non-approved applicants, in contrast, were more likely to report they were initially denied for reasons that require a longer period to resolve, such as:

- Down payment costs.

- Low credit scores.

- Adverse credit histories.

*Denial reason categories are not mutually exclusive.

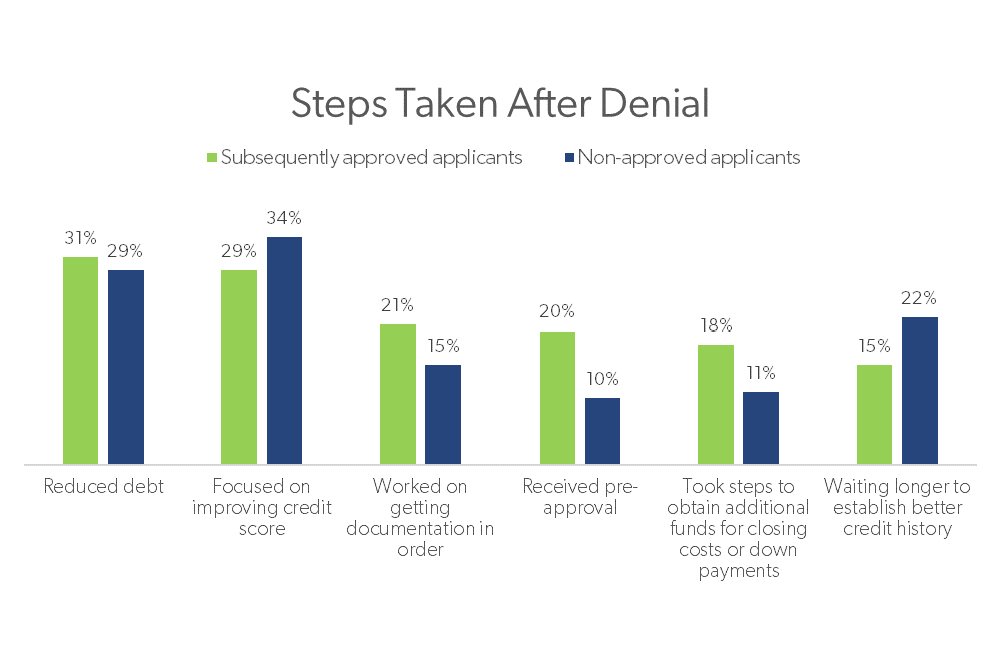

Actions Taken After Denial

Subsequently approved applicants were more likely to report they took certain quick-fix steps after their initial mortgage application denial, compared to non-approved applicants.

For both populations, respondents were most likely to indicate the actions they took were to improve their credit score and reduce debt. Beyond that, however, actions taken by each population diverged based on the reason for their denial.

*Steps taken after denial are not mutually exclusive.

For example, subsequently approved applicants were more likely to report they were denied for missing or incomplete information or appraisal differences, and therefore spent more time gathering the necessary funds or documents needed before receiving approval. Non-approved applicants were more likely to state they were focusing on working to improve their credit.

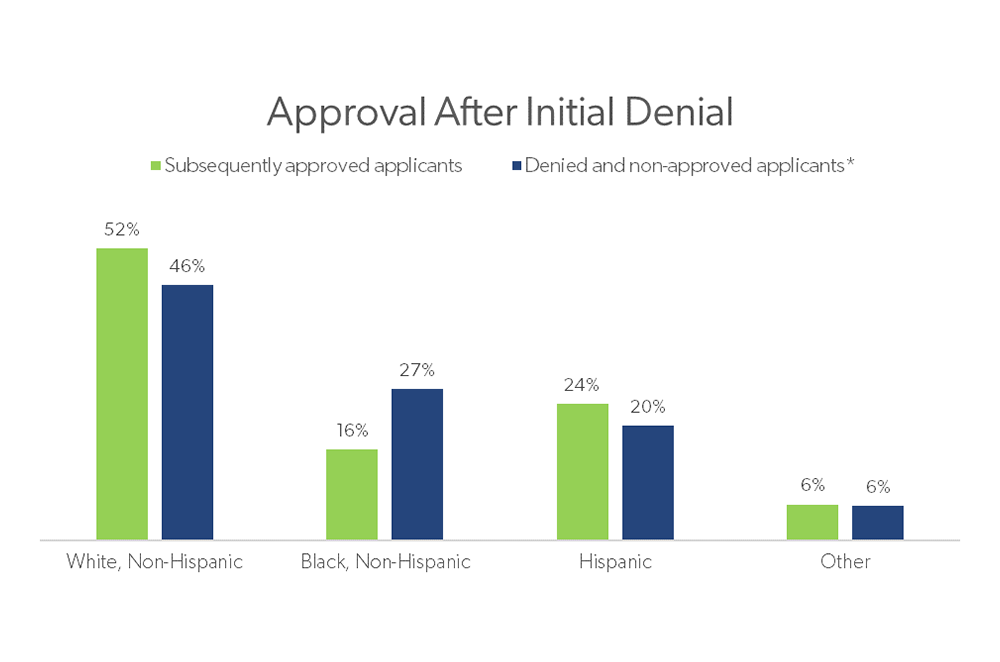

*May not have reapplied, reapplied and still in the process, denied again or denied and planning to reapply at some point.

Interestingly, whereas 78% of subsequently approved applicants said they reapplied with the same lender, only 17% of non-approved applicants said they expected to reapply with the same lender. This difference suggests that lenders have an opportunity to provide more educational and consultative resources to help turn more mortgage denials into approvals.

Freddie Mac’s Market Insights team fielded its quantitative study April 8-24, 2022, and it includes responses from 1,531 consumers who had been denied a mortgage application in the past four years. The survey oversampled for Black and Hispanic consumers.

Interested in more consumer research? Gain insights into the housing market from surveys of homebuyers, homeowners and renters in Freddie Mac Consumer Research.