Economic, Housing and Mortgage Market Outlook – June 2024

In this Issue

- Even though economic growth tempered in the first quarter of the year, it remains in line with historical averages.

- Mortgage rates receded from the highs seen in April and early May; moderating rates along with modest improvements in housing inventory should provide some respite to potential homebuyers.

Recent developments

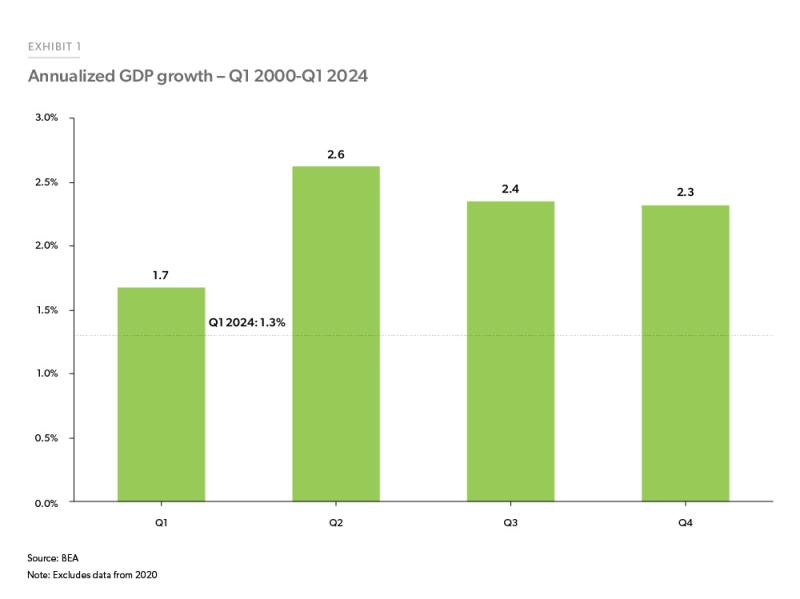

U.S. economy: The second estimate of U.S. economic growth released by the Bureau of Economic Analysis (BEA) in May 2024 showed further moderation of GDP growth to a 1.3% annualized rate in Q1 2024 as compared to the first estimate of 1.6%. Downward revisions to consumer spending were the largest contributor to the change along with private inventory investment and federal government spending. Consumption spending slowed to 2% annualized growth in Q1 as compared to 3.3% in Q4 2023. Consumption spending contributed 1.3% to the increase in GDP, implying that the other components offset each other – the increases in investment and government spending were offset by a decrease in net exports. While the downward revision of GDP for Q1 raises concerns of future growth, Q1 growth since 2000 has typically been slower than the other quarters despite being seasonally adjusted. Exhibit 1 shows the quarterly averages of growth rates from Q1 2000 to Q1 2024.

Per the Bureau of Labor Statistics (BLS), the labor market report showed job gains of 272,000 for the month of May, more than consensus expectation of 185,000.1 More than half of the total job gains for May came from healthcare, leisure and hospitality and government. Year-to-date job growth for 2024 is 1.2 million with an average of 247,000 jobs added each month. However, the unemployment rate ticked up to 4% for the first time since January 2022. Even with this uptick, the unemployment rate remained at or below the 4% mark for the twenty-eighth consecutive month and maintained the longest streak of at or below 4% unemployment since the 1960s.

Contrary to the employment report for May, which was strong, the Job Openings and Labor Turnover Survey (JOLTS) report released by BLS showed moderation in the labor market with job openings decreasing to 8.1 million in April. The job openings to unemployed ratio for April at 1.24 also moderated towards the pre-pandemic average.2 The quits rate remained at 2.2% for the sixth month in a row. While overall job growth remained strong, there is also some cooling reflected in the steadily rising unemployment rate and declining job openings.

The core Personal Consumption Expenditures (PCE) price index, the Federal Reserve’s preferred inflation gauge that strips out volatile food and energy prices, rose 0.3% month-over-month for the second consecutive month in April.3 Prices for goods increased 0.2% and prices for services were up 0.3% month-over-month in April. Core services excluding housing, so-called “super core” inflation, a measure of inflation that the Federal Reserve has been tracking, came in at 0.3% month-over-month in April, slightly lower than the 0.4% increase in March. While April’s core PCE movement was in the right direction, consistent moderation is imperative in the coming months for rates to come down since the index increased 2.7% from a year ago, above the Federal Reserve’s target of 2.0%.

The Consumer Price Index (CPI) increased by 0.3% in April, aligning with consensus expectations. The CPI release for April showed some softening from the previous high monthly readings. CPI for shelter also came in lower than anticipated marking the slowest increase since October 2023. We expect shelter to subtract from the CPI in the coming months as the decline in rents gets incorporated into the shelter component with a lag. On the other hand, insurance costs along with medical and financial services inflation have been rising at a more rapid pace, and thus remain concerning in the long run.

Overall, while growth moderated to start the year, it is still consistent with an economy that is growing, albeit at a slower pace. The labor market remained strong with respect to job growth, but the unemployment rate ticked up to the highest since January 2022 and we expect inflation to continue to moderate through the rest of the year.

U.S. housing and mortgage market: After benefitting from stable mortgage rates in the first couple of months of the year, the housing market experienced a slowdown in April due to a rebound in rates. Total (existing + new) home sales for April fell 2.3% from March and were down 2.7% from a year ago. Existing homes sold at an annual rate of 4.14 million in April, down 1.9% month-over-month and year-over-year.4 New home sales for April fell 4.7% from March to an annualized rate of 634,000, accounting for about 13% of total home sales.5 While housing inventory remains low as fewer people are switching homes due to the mortgage rate lock-in effect, there has been some uptick in both existing and new home inventory. Existing home inventory picked up 16% year-over-year to 1.21 million units, while new home inventory is at the highest level it’s been since January 2008.

Homebuilder confidence reversed course in May, declining 6 points to 45, according to the National Association of Home Builders’ Housing Market Index. The decline is below the threshold of 50, indicating poor building conditions over the next six months. The primary driver of the decline was attributed to higher mortgage rates.6 However, the housing construction sector experienced some growth in April. According to the U.S. Census Bureau, new residential construction picked back up in April with total housing starts increasing 5.7% month-over-month. While single-family starts retreated 0.4% month-over-month, multifamily starts surged by 31%.

The March FHFA Purchase-Only Home Price Index increased by 0.1% month-over-month compared to an increase of 1.2% in February. Year-over-year house price growth remained strong at 6.7% for March. The states with the highest annual house price appreciation were Vermont at 12.8% and New Jersey at 11.6% followed by New York at 10.9%.7 The house price growth is primarily influenced by the depleted inventory of homes available for sale, coupled with resilient demand which continues to exert upward pressure on home prices.

The 30-year fixed-rate mortgage averaged 7.06% in May, as measured by Freddie Mac’s Primary Mortgage Market Survey® and ended the month at 7.03%. According to the Mortgage Bankers Association (MBA) Weekly Application Survey, mortgage activity declined over the month as rates hovered around 7%. Overall mortgage activity was down 8.5% month-over-month and down 7.3% year-over-year at the end of May. Refinance activity for May was down 9.5% compared to April, and purchase applications were down 8.3% month-over-month at the end of May.

Higher interest rates continue to impact consumer credit performance. Overall, 3.2% of the outstanding debt was in some stage of delinquency, up 0.1 percentage point from Q4 2023.8 While overall delinquency rates increased in Q1 2024, they remain 1.5 percentage points below the pre-pandemic level of Q4 2019. While serious delinquency rates for credit cards, autos and mortgages increased over the quarter, mortgage performance has remained better than the other sectors. Credit card serious delinquencies increased from 6.4% in Q4 2023 to 6.9% in Q1 2024 and auto delinquencies increased from 2.7% to 2.8% during the same period. Mortgage delinquencies rose from 0.8% to 0.9% in Q1 2024.

Overall, while housing inventory improved modestly in April, it remains below the level necessary for a balanced housing market. This imbalance is impacting housing affordability, which continues to remain a challenge.

Outlook

We expect the U.S. economy to continue to moderate as consumers adjust their spending in response to higher interest rates. In our baseline scenario, we expect a slowdown in employment, accompanied by a modest uptick in the unemployment rate.

As inflation remains above the Federal Reserve’s target rate of 2%, an immediate cut in the federal fund rates is not on the horizon. However, in a scenario where the job market cools sufficiently to keep inflation in check, we anticipate one rate cut in the latter half of the year. This potential scenario could lead to a gradual easing of mortgage rates. We expect mortgage rates to remain above 6.5% through the end of the year, which compared to the rates as high as 7.8% witnessed last year is a positive development and could offer some respite for potential homebuyers.

Mortgage rates have been volatile over the past month, hovering between 6.9% and 7.2%; and they are still relatively high, deterring home sales. Despite robust housing demand driven by first-time homebuyers, we expect home sales to remain muted. The current housing demand is highly concentrated in the entry-level segment of the housing market, where the supply is short due to limited construction. Additionally, trade-up buyers are almost nonexistent as there is a financial disincentive to give up low rates on their current home in exchange for a higher rate on the trade-up home. However, unwavering demand and tight supply are expected to push home prices up, potentially leading to further increased home prices in both 2024 and 2025.

Our projection of mortgage origination is contingent on several factors, including home prices, home sales, and the cash share of purchases. As we anticipate a moderation in home sales, high prices, and a flat cash share of purchases, we expect purchase origination to be slightly higher in 2024 than in 2023. With mortgage rates above 7%, refinance activity is expected to be minimal. However, if interest rates drop below 6.5%, refinance activity could see some uptick, as millions of borrowers still have rates above 6.5%. Nevertheless, given persistent inflation, achieving rates below 6.5% is challenging. Our forecast suggests a modest increase in total origination volumes this year and next, primarily driven by home prices.

See the June 2024 spotlight on the “Asian American, Native Hawaiian, and Pacific Islander homeownership gap.”

Footnotes

- Moody’s Analytics consensus expectation.

- Pre-pandemic average for 2019 was 1.19.

- BEA

- National Association of Realtors

- U.S. Census Bureau

- National Association of Home Builders (https://www.nahb.org)

- The state house price indices are based on Q1 2024 data.

- New York Federal Reserve Consumer Credit Panel

Prepared by the Economic & Housing Research group

Sam Khater, Chief Economist

Len Kiefer, Deputy Chief Economist

Ajita Atreya, Macro & Housing Economics Manager

Rama Yanamandra, Macro & Housing Economics Manager

Penka Trentcheva, Macro & Housing Economics Senior

Genaro Villa, Macro & Housing Economics Senior

Jessica Donadio, Finance Analyst