Quarterly Forecast: Market Slowdown will Continue as High Rates and Prices Exacerbate Affordability Challenges

U.S. economic growth fell at a 1.6% annual rate in Q1 2022 primarily due to a decrease in exports and government spending and an increase in imports. Consumption has been supported by a strong labor market. The unemployment rate remained steady at 3.6% as of June. The U.S. economy added 372,000 nonfarm payroll jobs in June averaging 456,000 jobs gained per month in 2022.

Enlarge Image

Despite the strength in the labor market, economic uncertainty is on the rise and the economy is slowing due to inflation and ongoing geopolitical tensions. Inflationary pressures remain high with the all-item consumer price index (CPI) increasing 8.5% year-over-year in May 2022. Inflation has eaten into consumers’ pandemic savings as the costs of essentials such as food, energy, and rent have outpaced wage and income growth. Inflationary pressures will likely remain high throughout the year due to the impact of the geopolitical conflict on food and energy prices.

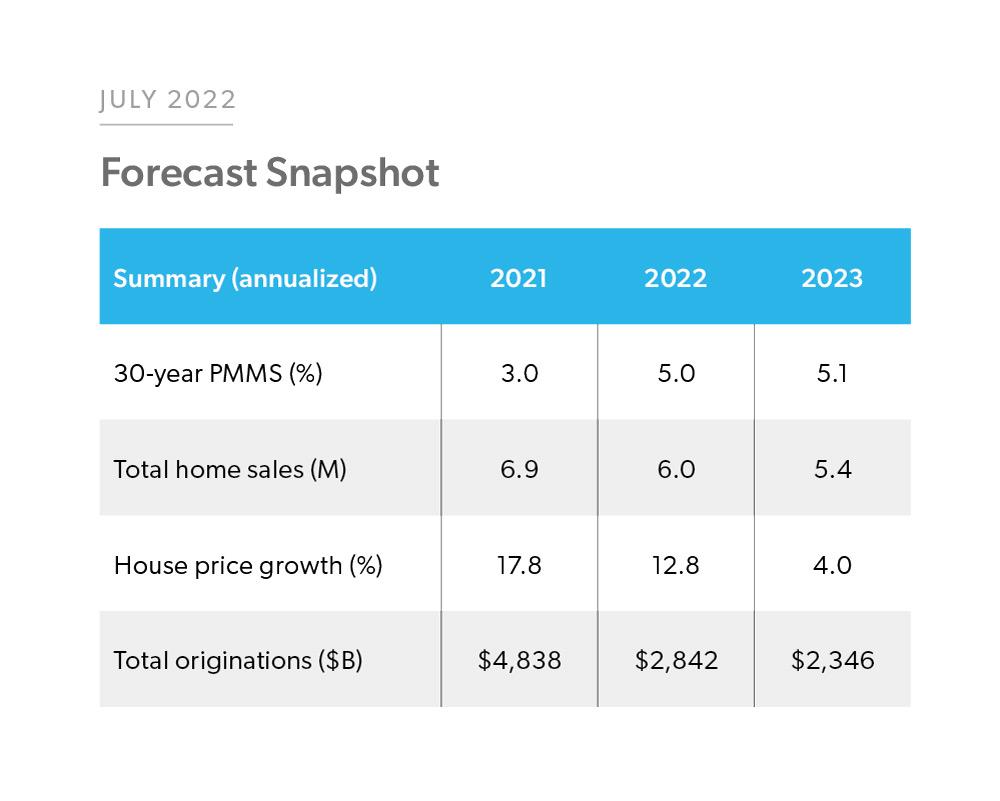

The Federal Reserve has increased the target fed funds rate by 1.5 percentage points through the first half of 2022 and the markets have been pricing in more aggressive rate increases. As a result, mortgage rates have been volatile over the past few weeks but have increased from 3.8% in the first quarter to 5.3% in the second quarter of 2022. We forecast 30-year fixed-rates to average 5% in 2022 and rise to 5.1% in 2023. House price appreciation is slowing to a more moderate growth rate and we expect price growth to be 12.8% and 4.0% in 2022 and 2023 respectively.

The rise in mortgage rates along with house price appreciation is leading to affordability challenges and causing a slowdown in the housing market. Both existing and new home sales have slowed in the latest surveys. Total home sales are down 17% since the beginning of the year. We expect housing demand to moderate and forecast home sales to slow to 6 million in 2022 and 5.4 million in 2023.

Given the house price growth and home sales expectation, we expect home purchase mortgage originations to be $2.0 trillion in 2022, slowing to $1.9 trillion in 2023. With mortgage rates expected to continue to rise, we forecast refinance activity to slow with refinance originations declining from $2.8 trillion in 2021 to $885 billion in 2022 and $463 billion in 2023. Overall, we forecast total originations to decline from the high of $4.8 trillion in 2021 to $2.8 trillion in 2022 and $2.3 trillion in 2023.

Enlarge Image

PREPARED BY THE ECONOMIC & HOUSING RESEARCH GROUP