Housing will have its best year in a decade

This year is shaping up to be the best year for housing in a decade. Home sales, construction housing starts and house prices are set to reach decade-level highs. Here are several reasons why we think this will happen.

Low mortgage rates

At the end of 2015, interest rates on 30-year fixed rate mortgages averaged over 4 percent, but declined at the start of 2016 and have remained below 4 percent so far this year. Low mortgage interest rates help support homebuyer affordability in the face of rising house prices and stagnant income.

If interest rates rise rapidly, like they did in the spring of 2013, housing market activity is likely to cool significantly. Our forecast is for mortgage interest rates to gradually rise, remaining below 4 percent for the first half of 2016, before inching higher and closing the year around 4.4 percent. On balance, the downside risks to this forecast are greater than the upside—there's a substantial likelihood that rates could remain below 4 percent throughout 2016. The path of rates depends on global economic conditions.

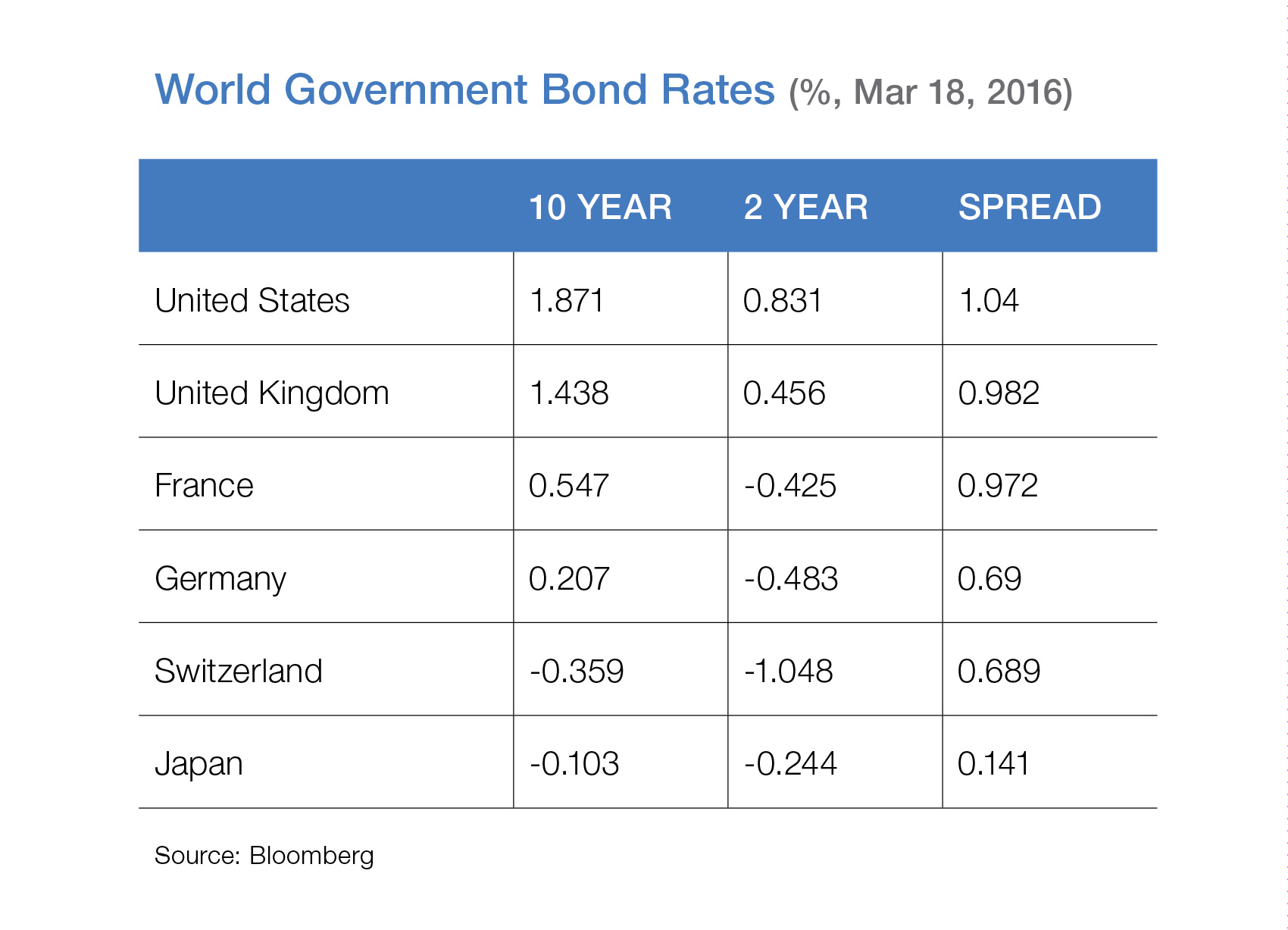

Many countries have negative interest rates. In Japan the 10-year government bond reached a record low of negative 0.1 percent in March. Across Europe many countries' sovereign bond yields also have negative interest rates, some on maturities out to 10 years. Exhibit 1 compares sovereign bond yields for 2-year and 10-year maturities across several advanced economies. While we think there's little chance the U.S. will have negative rates any time soon, negative rates abroad keep the lid on long-term rates in the U.S.

We think the outlook for global growth will improve—or at least stabilize—throughout the balance of this year and the downward pressure on U.S. rates will abate. More good news on the domestic U.S. economy, and a return to tightening by the Federal Reserve, will push rates higher later this year. The Fed is likely to only raise rates twice this year, which will slow the pace of interest rate increases.

Resilient labor market

The U.S. labor market has been remarkably resilient, producing an average of 205,000 net job gains per month since 2011. The steady flow of jobs has helped to bring the unemployment rate down below 5 percent. On the downside, labor force participation has fallen substantially with no sign of recovery and wage growth remains anemic.

Recent analysis from Goldman Sachs suggests that the labor force participation rate is unlikely to increase much from today's level. According to their analysis, which accounted for demographic and other socioeconomic factors, only about 0.1 to 0.2 percentage points of the more than 3 percentage point decline in the labor force participation rate since 2007 is due to cyclical factors and can be expected to reverse itself. The rest of the decline is driven by long-term factors like the aging of the population. Under this analysis, the prospects for increased labor force participation are dim.

If the labor force participation rate doesn't increase and job gains maintain their recent pace, then pressures are going to build and wages will rise. So far wage growth has been anemic, barely keeping pace with inflation. But if you look closely at the latest data on average hourly earnings you might convince yourself that we're at the nascent stages of a gradual increase in wages.

Wage growth ultimately will be a key factor for housing markets. If wages and incomes do not start rising, then rising interest rates, home prices and rents will squeeze households and ultimately slow housing markets.

Household formations on the rise

Given the steady job growth, household formations should start picking up. During the Great Recession household formation rates dropped and still have not picked up to match underlying population growth. Throughout the first half of 2015 the pace of formations seemed to be accelerating, reaching 2.2 million on a year-over-year basis in the second quarter of 2015. In the latter half of 2015, the pace of net household formations dropped by over 50 percent to 800,000 per year.

The drop-off in household formations could be an anomaly due to noisy data, or it could be a symptom of the lack of supply of housing. Total annual housing completions have been running below 1 million for several years, and the vacancy rates are dropping. With low levels of supply there is nowhere for households to be formed. So despite robust job gains household formations haven't followed yet.

Housing supply increases

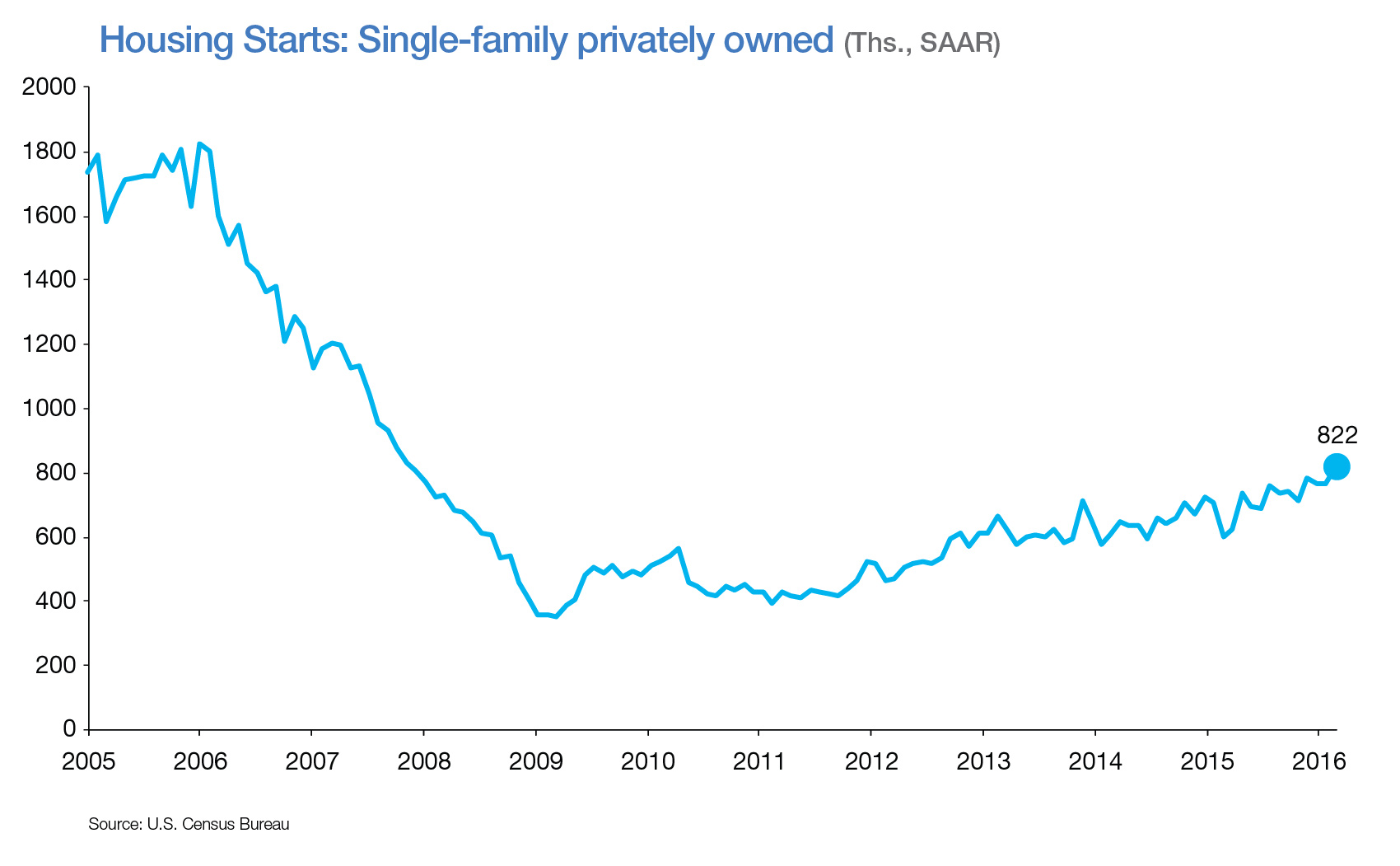

But there's good news in the housing construction data. Multifamily housing starts have been solid, running above 300,000 for the past three years. But without single-family construction increasing it's going to be hard to meet housing demand. In February 2016 single-family housing starts were at a seasonally-adjusted annual rate of 822,000 (Exhibit 2), a substantial year-over-over percent increase, but still well below what we'll need to meet long-run housing demand.

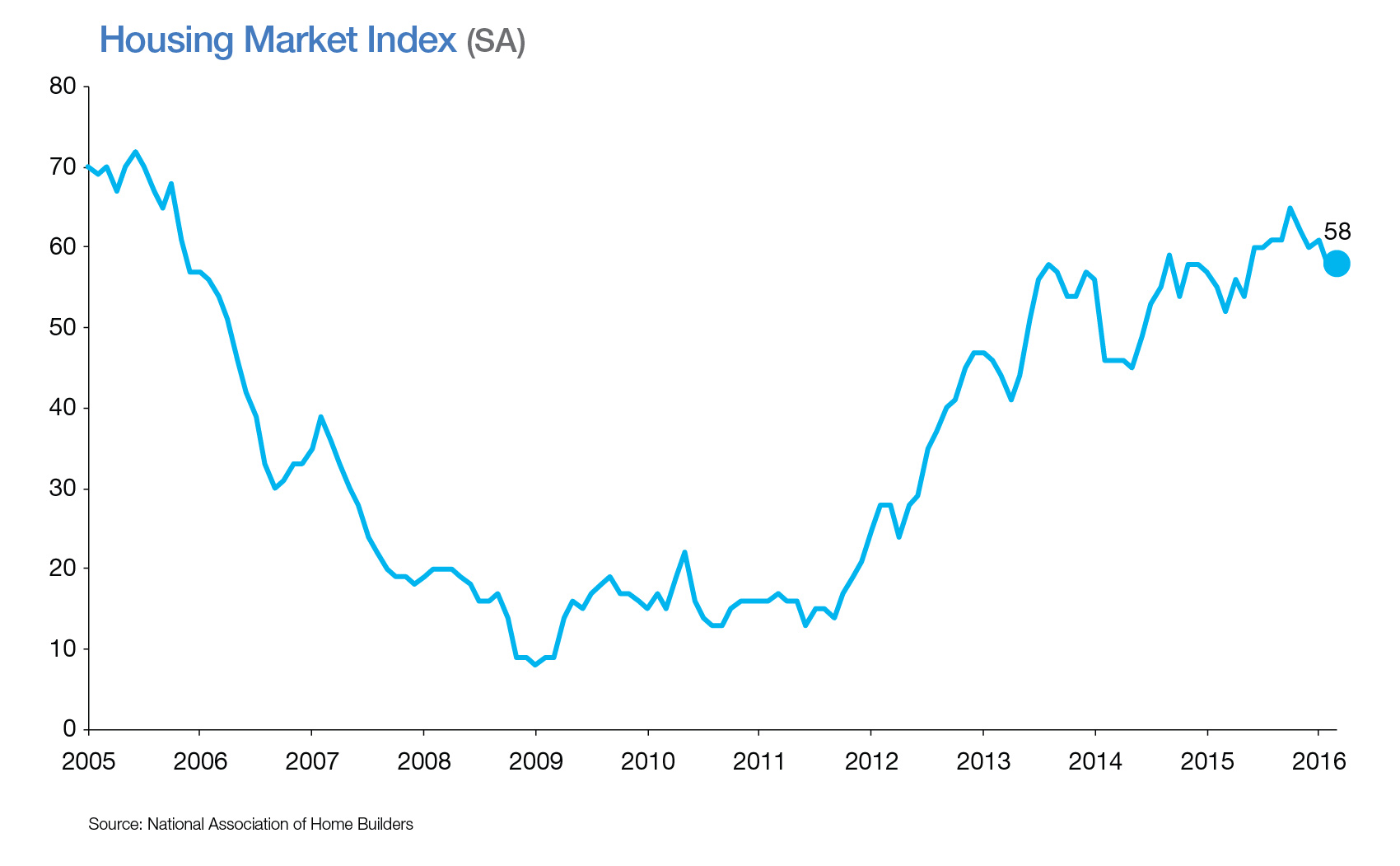

The recovery in single-family housing starts has been long (and tortured) despite optimism by homebuilders about the direction of the new home market. The NAHB/Wells Fargo Housing Market Index (HMI) tracks homebuilder sentiment. A reading above 50 indicates that on net respondents maintain a positive outlook about the new home market. The HMI for March 2016 was 58, marking the 21st consecutive month above 50. However, despite the optimistic sentiment, homebuilding activity has not followed suit. Historically the HMI and 1-unit housing starts have tracked each other closely. They still do, but the relationship has changed. If the historic relationship between sentiment and starts from 1985 to 2009 held, then single-family starts would be nearly 50 percent higher than where they are today.

One reason homebuilders have not ramped up home construction to match sentiment is a dearth of available labor. Recent analysis by the NAHB of the Bureau of Labor Statistics Job Openings and Labor Turnover Survey (JOLTS) pointed out that unfilled job openings for construction workers in January 2016 were the highest since July of 2007. The lack of skilled labor is one key factor holding back housing starts.

Nevertheless, housing starts are trending higher, which will bring more badly-needed new supply onto the market. We're forecasting that combined multifamily and single-family housing starts will increase 200,000 units to 1.3 million in 2016.

House prices moving higher

With demand picking up and supply lagging, house prices are moving higher.

In 2015, house prices increased about 6 percent on a year-over-year basis. We're forecasting house prices to continue to rise, but at a moderating pace, with annual house price appreciation slowing to 4.8 percent in 2016 and 3.5 percent in 2017. We think that long-term house prices should grow around 3 percent so this forecast is consistent with a market where supply issues slowly abate.

Higher house prices will help drive up homeowners' equity. According to a recent report by CoreLogic , 8.53 percent of borrowers are underwater (i.e., the mortgage exceeds the value of the property used to secure the loan. This is down from a high of 26 percent in 2009 and reflects the solid house price gains of recent years.

Higher house prices are driving down affordability. According to analysis by the National Association of Realtors (NAR), the qualifying income—the minimum gross income necessary to afford the median priced home in the U.S. with a down payment of 20 percent and the requirement that gross housing expenses not exceed 25 percent of gross income—has increased $3,400 from January 2015 to January 2016. With house prices forecasted to rise further, more and more households will face an affordability pinch.

Best year in a decade

Despite the challenges facing the housing market, we expect this to be the best year for housing in a decade. Home sales, housing starts, and house prices will reach their highest level since 2006 according to our latest forecast. Low mortgage rates and an improving labor market—including modest income gains—will help drive housing markets higher. Challenges remain, with low housing supply and declining affordability being a key concern in many markets, but on balance, the housing markets in the U.S. are poised for the best year since 2006.